Issue Summary

The United States has had long-standing affordable housing issues, which include shortages of affordable rental housing that is safe and accessible and challenges with building enough affordable housing.

To support affordable rental housing, federal agencies administer more than a dozen different programs that provide rental assistance payments, grants, loan guarantees, and tax incentives—such as the Department of Housing and Urban Development’s (HUD) Housing Choice Voucher program. Additionally, HUD is responsible for ensuring that housing units subsidized through its rental assistance programs are safe and sanitary and that housing providers make reasonable accommodations for individuals with disabilities. HUD and the Department of the Treasury also support the construction of affordable ownership and rental housing through programs like the Self-Help Homeownership Opportunity Program, the Housing Trust Fund, and the Low-Income Housing Tax Credit.

However, agencies could improve how they administer such programs.

For instance:

- Affordable rental housing. Many low-income renters face a shortage of affordable housing. The Housing Trust Fund program, which began in 2016, is designed to preserve and increase the supply of affordable housing units. HUD allocates program funds to states for affordable housing projects. However, it could improve its oversight of such projects by more comprehensively assessing fraud risks. Additionally, HUD provides rental assistance to low-income households through programs administered by state and local public housing agencies. These agencies are required to provide utility allowances to assisted households that pay utilities separately from rent. However, HUD's allowance-related tools and guidance may not be very useful for these agencies. Additionally, the Department of Defense could develop a comprehensive list of critical housing areas and take other steps to help ensure that service members and their families have access to affordable, quality housing.

- Reasonable accommodations. HUD enforces federal civil rights laws that require housing providers to make reasonable accommodations—such as providing entryway ramps—for households with disabilities. These requirements also apply to the housing providers that administer HUD's own rental assistance programs. However, although HUD collects information on a household's disability status, it does not systematically collect data on requests for reasonable accommodations for its 3 largest rental assistance programs. HUD could also take steps to help address the challenges older adults experiencing homelessness face in finding affordable housing—such as finding housing with accessibility features like grab bars.

- Assistance for domestic violence or sexual assault survivors. HUD requires that its housing providers have emergency transfer plans to move survivors of domestic violence or sexual assault from their current subsidized housing unit to one in a new location. However, providers often didn't specify how transfers would take place.

- Lead paint. HUD is responsible for ensuring that housing units provided under its rental assistance programs are safe and sanitary. For its Project-Based Rental Assistance Program, HUD monitors lead paint risks through management reviews and periodic physical inspections. But HUD has not conducted a comprehensive risk assessment to identify properties posing the greatest risk to children under the age of 6.

Image

- Flexible housing funds. An experimental HUD program, the Moving to Work demonstration, gave 39 participating public housing agencies the flexibility to use HUD funding for purposes other than housing assistance—such as developing affordable housing, and imposing work requirements and time limits on tenants. However, HUD could take steps to more comprehensively capture and track data on households served by this program.

- Tax credits. Developers can apply for federal Low-Income Housing Tax Credits to help them build affordable housing projects. The amount of credit depends largely on project costs. However, project costs vary widely, and federal oversight of costs is limited. Currently, no federal agency has the authority to collect and report on project costs for the tax credit. The Internal Revenue Service and the Treasury should use data on variables that affect cost—such as square footage and building type—to better monitor this tax credit.

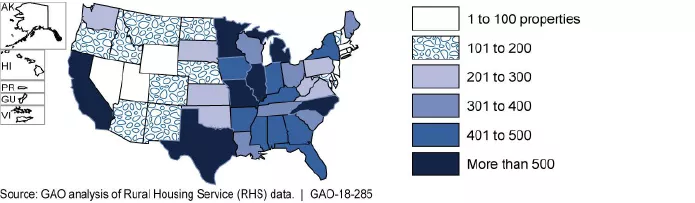

- Rural rental housing. USDA’s Rural Housing Service (RHS) provides mortgages to support affordable rental units for low-income tenants through its Rural Rental Housing Program. When these mortgages reach the end of their terms (mature), property owners may exit the program—and current law does not allow RHS to continue providing rental assistance when this occurs. As a result, tenants in properties with mortgages that are maturing may face rent increases or lose their housing altogether. Congress should consider granting RHS the authority to continue providing rental assistance to tenants in properties with maturing mortgages.

Image

- Manufactured housing. Manufactured housing—prefabricated, factory-built homes—can be an affordable option for lower-income homebuyers. But some borrowers may not qualify for mortgages and might have to turn to other kinds of financing with less favorable rates and terms. Several federal agencies, including HUD, have created new or modified existing loan programs to help manufactured home borrowers. HUD has also taken some steps to improve the financing of manufactured housing but has not fully implemented several proposed changes.

- “Sweat equity” program. HUD administers the Self-Help Homeownership Opportunity Program (SHOP), which is a competitive federal grant program that awards funds to eligible nonprofit organizations to help develop affordable housing units for purchase by low-income families. Buyers are expected to contribute "sweat equity" to the project by helping to build their own homes. However, HUD could make better-informed program decisions for this program. For example, market data shows that costs for some activities the grant can pay for have risen over time. But HUD has only changed the grant's per-unit spending limit twice. Using relevant data could help HUD determine if spending limits are keeping pace with costs.