Low-Income Housing Tax Credit: Opportunities to Improve Oversight

Fast Facts

In this Snapshot we review our prior work on the Low-Income Housing Tax Credit—the largest source of federal assistance for developing affordable rental housing.

We've found that the cost of projects using the tax credit varies widely and that there's minimal federal oversight. We discuss ways to address these issues—for example, by collecting better data on project costs. Currently no federal agency has the authority to collect and report on this data for the tax credit. We've previously recommended that Congress consider designating an agency to do so.

Highlights

The Big Picture

The U.S. has a widespread shortage of affordable housing. The Low-Income Housing Tax Credit (LIHTC) is the largest source of federal assistance for developing affordable rental housing. It provides tax credits typically through state and local housing finance agencies to developers and private investors to develop affordable housing.

Overview of Low-Income Housing Tax Credit Process

The Internal Revenue Service (IRS) administers the tax credit at the federal level and housing finance agencies administer and oversee the program in states and localities. These agencies develop Qualified Allocation Plans, which identify priority housing needs and contain selection criteria for awarding the tax credits. The agencies evaluate proposed projects against their plans and award tax credits to developers. Agencies can use the plan's selection criteria to influence the types of projects developers propose and build.

Projects awarded tax credits must remain affordable to qualifying low-income households for at least 30 years. Developers often try to attract investors willing to contribute financing in return for an ownership interest in a project (a process known as buying tax credits). A syndicator can be used to facilitate this process. Projects often require additional financing to cover development costs. Gaps in funding may be filled by private sources or federal, state, or local affordable housing programs such as the Housing Trust Fund .

What GAO’s Work Shows

Our 2018 report identified areas for improving the oversight of the tax credit, including development costs. We also issued reports in 2015 and 2016 on the tax credit's administration and oversight.

Despite LIHTC's size and complexity, federal oversight of the tax credit has been minimal. This is in part because IRS is the only federal agency that administers the program. According to IRS, the agency does not have the authority or resources to collect and report detailed information on the tax credit. The Department of Housing and Urban Development (HUD) collects some data on the program, but it does not have the authority to collect cost data.

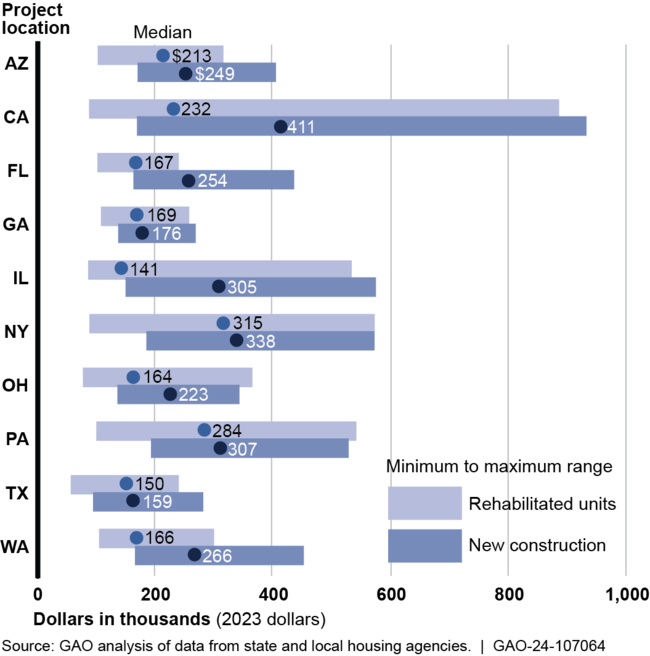

In 2018, we determined the per-unit cost of 1,849 LIHTC projects in selected locations. Project characteristics such as construction type (new construction or rehabilitation), number of units, target income level (low-income or mixed), location (urban, suburban, or rural), and local housing market conditions explained some cost differences across projects. Due to differences in these characteristics, we found that costs varied widely among the 12 housing finance agencies in our study.

Adjusted Development Costs for Rental Housing That Received Low-Income Housing Tax Credits, Selected States, 2011–2015

Note: We adjusted project costs to 2023 dollars using the Calendar Year Chain-Weighted Gross Domestic Product Price Index.

Our analysis was limited to selected variables we were able to consistently collect and that were similarly defined across the selected housing finance agencies. Housing finance agencies have flexibility in what cost-related data to collect, how to maintain these data, and how to define variables for evaluating the program. Inconsistency in how agencies collect cost-related data results in data limitations and constrains oversight and analysis of the program's efficiency and effectiveness.

➢ We recommended that Congress consider designating an agency to regularly collect and maintain specified cost-related data from housing finance agencies and periodically assess and report on the tax credit's development costs.

➢ We also recommended that IRS encourage housing finance agencies and other tax credit stakeholders to collaborate on developing standardized cost data.

Our work also analyzed how housing finance agencies use their Qualified Allocation Plans to select projects to develop. Section 42 of the Internal Revenue Code requires that plans give preference to certain projects, including those that serve the lowest income tenants. It also specifies some selection criteria, such as project location and tenant populations with special housing needs. Housing finance agencies have flexibility to create their own methods for scoring developers' applications and can include selection criteria appropriate to local conditions. For example, agencies commonly included proximity to transit and energy efficiency as criteria. Other criteria included qualifications of the project development team, cost-effectiveness, and leveraging other federal or state programs.

Challenges and Opportunities

LIHTC is a key federal program for addressing the shortage of affordable housing, but it is difficult to compare cost drivers and trends across locations because federal oversight of cost data is limited and data collection is inconsistent. Designating an agency to collect and report on project development costs could more efficiently address existing oversight challenges. Further, greater standardization of cost data would allow better analysis of cost drivers and cost-management practices, which could help increase the program's efficiency.

More from GAO's Portfolio

Low-Income Housing Tax Credit: GAO-18-637 , GAO-16-360 , GAO-15-330 , GAO-17-285r , GAO-13-66

Affordable Housing: GAO-23-105647 , GAO-23-106628 , GAO-23-105370

Manufactured Housing: GAO-23-105615

HUD Rental Assistance: GAO-23-106339 , GAO-23-105083

For more information, contact Jill Naamane at (202) 512-8678 or NaamaneJ@gao.gov.