Issue Summary

Tax expenditures are provisions of the tax code that can reduce how much a taxpayer owes—and therefore federal revenue. Examples include special tax credits, deductions, exclusions, exemptions, deferrals, and preferential tax rates. Tax expenditures have the same net effect on the federal budget as spending programs.

However, unlike federal discretionary spending, tax expenditures do not compete with other priorities in the annual appropriations process, and many are not subject to congressional reauthorization. Instead, many tax expenditures operate like mandatory spending programs (such as Medicare), with eligibility rules and formulas that provide benefits to those who wish to participate.

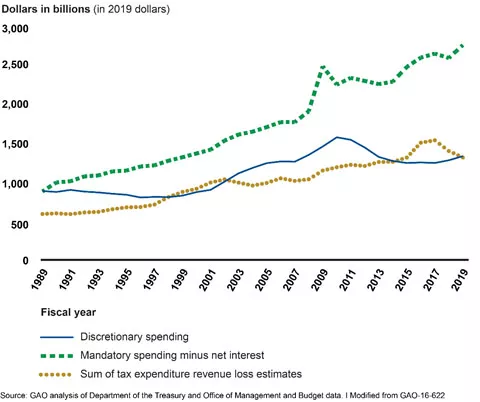

Tax Expenditures Are Comparable in Size to Federal Discretionary Spending

Image

Note: Summing tax expenditure estimates provides a sense of size but does not take into account possible interactions among individual tax expenditures or outlay effects from refundable credits. Total change in tax revenues from repealing tax expenditures could differ from the sum of the estimates. To view the data behind this graphic, download it in TXT or PDF format.

Paying attention to tax expenditures is an important step to addressing the nation’s fiscal health, and they should be part of broader tax reform discussions.

For example:

- Assessing tax expenditures. Periodic reviews and evaluations could help determine how well tax expenditures work to achieve their goals, and how their benefits and costs compare to other programs with similar goals. The Office of Management and Budget (OMB) and the Treasury could develop a framework for assessing tax expenditure performance. OMB could also help agencies identify which tax expenditures contribute to agency goals.

- Opportunity Zones. Congress created Opportunity Zones to spur investment in distressed communities. About 10% of Americans live in these nearly 9,000 zones. In these areas, certain business investments can bring significant tax benefits to the investor. Unlike other, similar tax incentives, there is no limit on the amount investors can claim for tax breaks. However, it’s unclear how these Opportunity Zone investments will actually affect these communities and whether investors will follow the tax rules.

- Low Income Housing Tax Credit. This tax credit is the largest source of federal assistance for developing affordable housing. The cost of projects using the tax credit varies widely, and federal oversight of the credit is limited. But no federal agency has the authority to collect and report better data on project costs.

- Renewable energy tax expenditures. The federal government aids the development of utility-scale electricity generation projects—particularly renewable ones. For example, federal tax expenditures aided the development of such projects, but there is limited data on the effectiveness of these tax expenditures.

- Tax credits for research. The tax credit for qualified research expenses provides significant subsidies to encourage business investment in research intended to foster innovation and promote long-term economic growth. Generally, the credit provides a subsidy for research spending in excess of a base amount, but concerns have been raised about its design and administrability.