Issue Summary

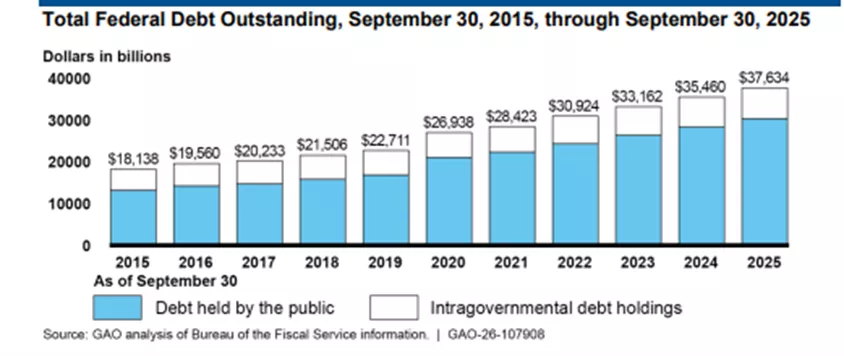

At the end of FY 2025, total federal debt was $37.6 trillion. Of this, 80% was debt owed to investors (debt held by the public) and 20% was debt the government owed itself (what Treasury owes to other parts of the government).

Image

To meet government borrowing needs, Treasury borrows money from the public by issuing Treasury securities (e.g., bills, notes, bonds, etc.) to investors on a regular and predictable schedule. The interest rates at which investors purchase Treasury securities at auction determine the government’s borrowing costs. Strong demand for Treasury securities from a variety of investors helps maintain low government borrowing costs. Treasury must continue to promote strong demand for its securities while making debt issuance decisions—such as what type of Treasury security to issue and in what quantity—that navigate financial and economic conditions.

Some of Treasury’s considerations include:

- Uncertain borrowing needs. Policy changes and economic conditions can affect federal cash flow. For example, the federal response to the COVID-19 pandemic led to unprecedented spending. Treasury sold securities to quickly raise trillions of dollars. Other external events like recessions, military conflicts, and emergencies (e.g., natural disasters such as hurricanes) can also affect borrowing needs.

- Uncertainty about future interest rates. Treasury’s debt management goal is to borrow at the lowest cost over time. In addition to financing government operations each year, Treasury must also refinance maturing debt. For example, in FY 2026, Treasury will need to refinance $9.7 trillion in maturing securities at market interest rates. Treasury must manage its debt portfolio to balance low financing costs with rollover risk (the risk that it may have to refinance its debt at higher interest rates). To do this, Treasury considers the mix of long-term and short-term securities that it offers. Long-term securities typically have higher interest rates but reduce rollover risk because they do not mature as frequently. Short-term securities usually have lower interest rates but must be refinanced more frequently, potentially at higher interest rates.

- Debt limit stalemates. The debt limit is a legal limit on the total amount of federal debt that can be outstanding at one time. Delays in suspending or raising the debt limit create debt and cash management challenges for Treasury. Delays in raising the debt limit have occurred in 13 of the 15 years between 2011 and 2025. As a result, Treasury has often used extraordinary actions to remain under the limit, such as suspending investments or temporarily disinvesting securities held in federal employee retirement funds. Once it has exhausted all extraordinary actions, Treasury may not issue debt without further action from Congress and the President. If Treasury exhausts borrowing authority and runs out of cash to continue paying government obligations, a default will occur—which could be devastating for individuals, financial institutions, and the economy. Even without a default, the current debt limit process imposes avoidable costs on taxpayers, disrupts financial markets, and reduces investor confidence in Treasury securities. There are alternative approaches to the debt limit that would mitigate these risks.

- Treasury market disruptions. Disruptions in the Treasury market could reduce investor demand for Treasury securities and raise borrowing costs. For example, the COVID-19 pandemic shocked financial markets and caused many investors to sell their Treasury securities for cash at the same time, which strained market trading and sent interest rates higher on some securities. Other market disruptions also occurred in 2019 and 2014, which led to periods of stress. Such disruptions pose risks to the liquidity and efficiency of the Treasury market, at a time when debt issuance and debt held by the public continue to grow.

Image