Federal Reserve Lending Programs: Credit Markets Served by the Programs Have Stabilized, but Vulnerabilities Remain

Fast Facts

The last of the Federal Reserve's emergency lending programs supported through CARES Act funding ended in early 2021. As of September 1, 2021, the programs had about $19 billion in assets. Economic indicators we examined suggest that these programs helped improve liquidity and access to credit in markets they targeted. Entities that used the programs, such as state and local governments and small businesses, generally said they were beneficial.

However, vulnerabilities remain. For example, high debt levels leave businesses financially vulnerable, and the pandemic's duration may affect state and local governments' ability to repay their debt.

Highlights

What GAO Found

The Board of Governors of the Federal Reserve System (Federal Reserve) authorized 13 lending programs—known as facilities—to ensure the flow of credit to various parts of the economy affected by the COVID-19 pandemic. The last of the nine facilities supported through CARES Act funding ceased purchasing assets, such as corporate bonds, or extending credit by January 8, 2021. As of September 1, 2021, the CARES Act facilities held about $19 billion in assets. The Federal Reserve oversight reviews completed in December 2020 identified opportunities to enhance certain areas, including internal process and controls. These reviews also identified areas for continued monitoring, such as cybersecurity and conflicts of interest. GAO found that Federal Reserve's plans for ongoing monitoring of the facilities align with federal internal control standards for ongoing monitoring of an entity's internal control system.

Available indicators suggest the facilities helped improve access to credit and liquidity in the corporate and municipal credit markets. For example, corporate bond spreads (which reflect borrowing costs) have remained low, and municipal spreads have decreased to prepandemic levels. Also, officials from state and local entities that participated in the Municipal Liquidity Facility (which targeted the municipal bond market) generally said the facility was beneficial and helped restore investor confidence in the municipal bond market. However, corporate and municipal credit markets remain vulnerable. For corporate credit markets, corporate bonds outstanding remain elevated and the high level of debt leaves businesses vulnerable to distress. Municipal credit markets also remain vulnerable because of the pandemic's extended duration, which may adversely affect local economies. According to surveys of small and independent businesses and lenders, access to credit has improved, but recovery remains slow, including for businesses in the services sector.

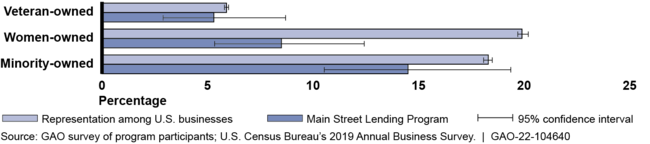

Loans made under the Main Street facilities (which targeted small and mid-sized businesses and nonprofits) were concentrated among small for-profit businesses in certain economic sectors, such as restaurants. According to GAO's generalizable survey of Main Street borrowers, an estimated 88 percent said that the program was “very important” in helping them maintain operations. Women-owned businesses participated at lower rates compared to their representation among U.S. businesses. Although estimates of veteran- and minority-owned business participation were somewhat lower compared to their representation among U.S. businesses, the differences were not statistically significant (see figure).

Estimated Participation of Business Types in the Main Street Lending Program

Why GAO Did This Study

On July 30, 2021, the last of the 13 Federal Reserve lending facilities stopped purchasing assets or extending credit. However, some of these facilities, including facilities that were supported through Department of the Treasury funding appropriated under section 4003(b)(4) of the CARES Act, continue to hold outstanding assets and loans. The Federal Reserve will continue to monitor and manage the facilities until these assets and loans are no longer outstanding.

The CARES Act included a provision for GAO to periodically report on section 4003 loans, loan guarantees, and investments. This report examines the Federal Reserve's continued oversight and monitoring of the CARES Act facilities; what available evidence suggests about the facilities' effects on corporate credit markets, states and municipalities, and small businesses; and the characteristics of Main Street Lending Program participants, among other things.

GAO reviewed applicable laws and agency and Federal Reserve Bank documentation; analyzed agency and other data on the facilities and credit markets; interviewed Federal Reserve and Treasury officials and representatives of state and local governments; and conducted a generalizable survey of for-profit Main Street borrowers.

For more information, contact Michael E. Clements at (202) 512-8678 or clementsm@gao.gov.