Is it Harder for Women to Save for Retirement?

In a word: yes.

On Thursday, the Comptroller General of the United States Gene Dodaro, head of GAO, testified about the unique challenges women face saving for retirement. Among those challenges, he noted that women have longer life spans, lower lifetime earnings, and that they are more likely to be primary caregivers, which can limit them from maintaining paid employment. To watch the testimony, click here.

Today’s WatchBlog explores our portfolio of work on women’s retirement issues, including our findings from recent interviews with groups of older women.

Also, check out our new video where you can hear from women, in their own words, discuss their concerns about saving for retirement.

Gender wage gap contributes to disparities

In 2012, we found that women reported annual contributions to retirement accounts that were around 30% lower than men’s contributions. Despite their economic gains, women continue to have lower annual earnings than men, on average, and much lower lifetime earnings.

Older women told us that they feared they would be unable to pay their future expenses. Some expected their financial situations to deteriorate during retirement. Many said they worry about having to turn to others, including their children, for financial assistance. Some of the women reported being in debt already, not having savings, and needing to continue working to make ends meet.

One woman told us, “…[M]ost of my jobs in my life were very low-paying jobs, and there was no retirement benefits. There was nothing like that.”

Women’s career trajectories can lead to less savings and lower Social Security payments

In 2019, we found that women were more likely than men to take on caregiving responsibilities, which may interrupt saving for retirement. Taking time out of the workforce to raise children or grandchildren or care for elders can also take a big bite out of a woman’s future Social Security payments.

One woman told us, “I have always said since I started collecting Social Security that I really have empathy for women who’ve stayed at home with their kids, who’ve done something else, and their Social Security is not being funded, and then they end up having to live on it.”

In 2020, we found that grandparents who were financially responsible for their grandchildren were mostly female and more likely than the general population to be poor.

Older women regret not being better informed about financial planning

Older women expressed concern about losing their Social Security or Medicare benefits and described Social Security as a financial resource that is critical to their retirement security.Some said their sense of financial security was also tied to having income from multiple sources, including from retirement savings and other investments.

But many of the women we spoke to said they didn’t always know how to create more retirement income for themselves. They reported being unfamiliar with how investments worked or how important employer matching policies and compound interest were to building wealth. One woman said, “…I should have been paying more attention. Instead of putting 50 cents, I should have been putting a dollar, you know, in that matching.”

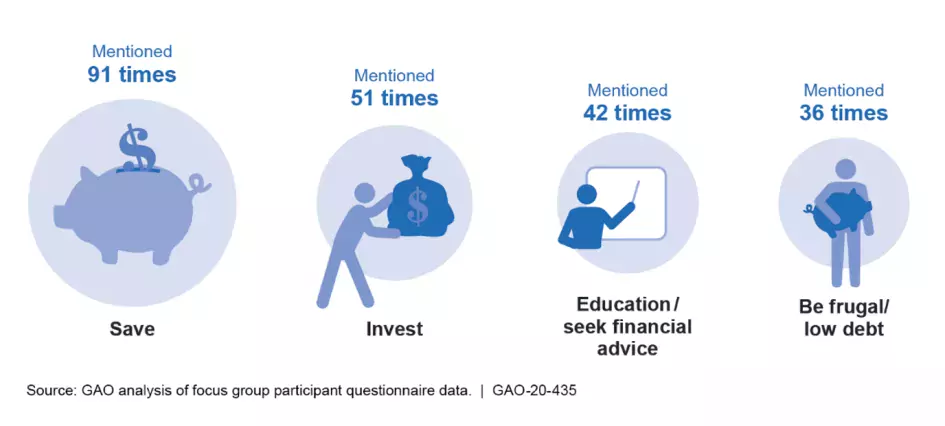

Older women said they would tell younger women to seek advice and prepare early for retirement. The below graphic illustrates the top 4 pieces of advice older women had for younger women.

Image

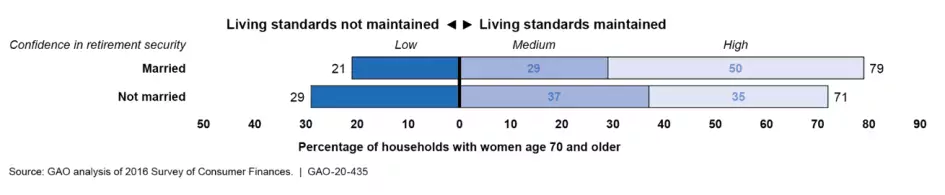

Marital status affects women’s retirement income more than men’s

In 2019, we found that unmarried women had lower retirement income than their married counterparts. Our 2012 study also found that women’s household income and assets fell on average by 41% after divorce, almost twice the size of the decline that men experienced.

Retirement Confidence among Households with Women 70 and Older, by Marital Status

Image

In a divorce, a spouse often doesn’t have a legal claim to the other spouse’s retirement accounts—and establishing such a claim can be complex.

We reported that about one-third of women who experienced a divorce and said their former spouse had a retirement plan also reported losing a claim to that spouse’s benefits. We recommended the Department of Labor make better information available to help divorcing spouses navigate the process of establishing these claims.

What can be done?

Previously, we suggested that Congress explore ways to help people boost retirement income, which may include increasing access to retirement savings plans, improving tax incentives to save for retirement, and expanding Social Security benefits. All of these ideas and more could help women—and everyone else—become more financially secure in retirement.

- Comments on GAO’s WatchBlog? Contact blog@gao.gov