The Big Shift in Mortgage Lending That Poses Risks to the Housing Market

Homebuyers are increasingly relying on “nonbank” mortgage companies to finance their properties. In fact, these nonbanks now make and service most mortgage loans.

Unlike traditional banks, nonbanks don’t take deposits to fund loans or help withstand financial stress. Instead, they rely on short-term funding to finance their operations.

What’s driving this trend and what are its potential risks? Today’s WatchBlog post looks at our new report on the rise and monitoring of nonbanks in the mortgage market.

Image

The Great Recession’s role in the rise of nonbank mortgages

The Great Recession occurred nearly 20 years ago. But we’re still feeling its impacts. In the midst of that crisis, the federal government’s backing of the mortgage market grew sharply, including through guarantees of mortgage-backed securities. And in the wake of the crisis, banks retreated from the mortgage market. This was partly due to changes in capital requirements that made it more expensive for banks to hold mortgages.

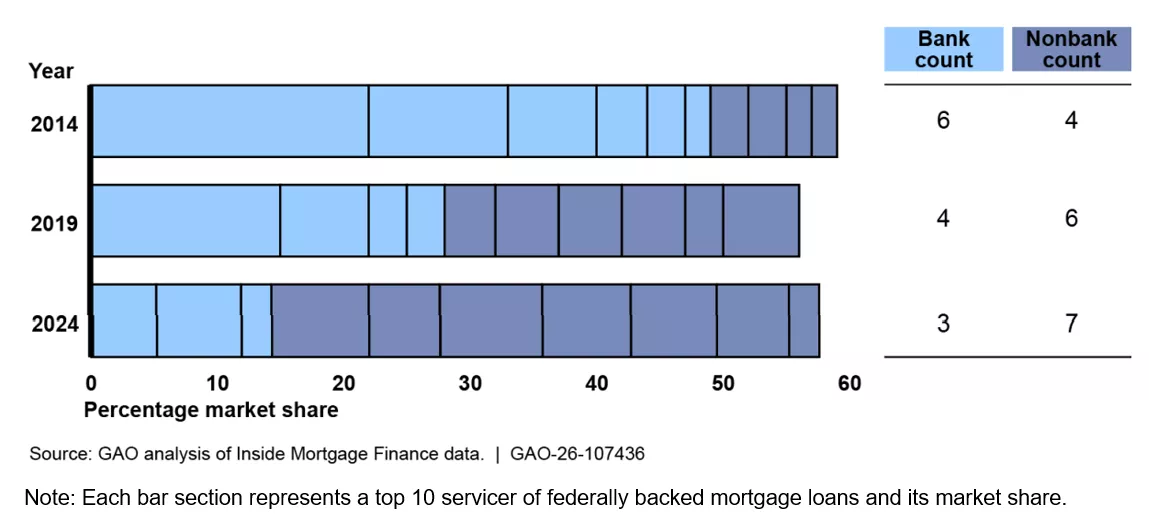

But people still needed mortgages to purchase homes. So nonbank mortgage companies (such as Rocket Mortgage) took on a bigger role. From 2014 through 2024, nonbanks largely replaced banks as the top lenders and servicers of federally backed mortgages. For example, during that time, the share of these mortgages serviced by nonbanks rose from 27% to 66%.

Market Share of the Top 10 Servicers of Federally Backed Mortgages

Image

What are the benefits of nonbank mortgages? As nonbanks filled the void left by traditional banks, they also benefited the mortgage market in other ways.

Nonbanks were quick to adopt technology that has made it easier and faster to get a mortgage. As result, many consumers can complete a mortgage application entirely online. Nonbanks also play a major role in lending to lower-income households and other groups that historically have had less access to credit.

What are the risks? Nonbanks are vulnerable to economic downturns, due partly to their reliance on short-term credit lines. In times of economic stress, restrictions on those credit lines could prevent nonbanks from meeting their financial obligations or from making new mortgages.

The failure of a large nonbank—or even multiple smaller ones—could disrupt mortgage markets. And because the federal government supports the market through insurance and guarantees, American taxpayers could be on the hook to cover losses.

What’s the federal government’s role in monitoring nonbank risks?

Nonbank mortgage companies generally do not have a federal regulator overseeing their safety and soundness. But two federal agencies that support the stability of mortgage securities markets—Ginnie Mae and the Federal Housing Finance Agency (FHFA)—are among the federal entities that play a role in monitoring nonbanks.

- Ginnie Mae guarantees almost $3 trillion in mortgage-backed securities.

- FHFA oversees Fannie Mae and Freddie Mac—corporations under federal conservatorship that issue and guarantee trillions of dollars in mortgage-backed securities.

Both agencies have processes to monitor the financial condition of nonbanks. But we identified areas for improvement:

- Financial data. Both agencies analyze nonbanks’ self-reported financial data as part of their monitoring efforts. But we found that FHFA is not taking all the steps needed to ensure the data is reliable. This could reduce the dependability of FHFA’s financial analyses of nonbanks.

- Watch lists. Both Ginnie Mae and FHFA produce watch lists of nonbanks that pose relatively higher risks, based partly on financial data. But we found that neither agency fully assesses key risks of short-term credit lines. As a result, the agencies may not be fully considering information material to their watch lists.

- Scenario analyses. Both agencies analyze the effect of changing economic conditions on nonbanks’ financial health. But Ginnie Mae focuses on a single economic stress scenario that does not capture the range of possible outcomes. By not considering multiple stress scenarios, Ginnie Mae’s is less prepared for risks that could affect its financial exposure and the stability of the mortgage market.

We made recommendations to Ginnie Mae and FHFA on how they could address these issues. To learn more about nonbank mortgages and our recommendations, check out our full report.

- GAO’s fact-based, nonpartisan information helps Congress and federal agencies improve government. The WatchBlog lets us contextualize GAO’s work a little more for the public. Check out more of our posts at GAO.gov/blog.

- Got a question or comment? Email us at blog@gao.gov.

GAO Contacts

Related Products

GAO's mission is to provide Congress with fact-based, nonpartisan information that can help improve federal government performance and ensure accountability for the benefit of the American people. GAO launched its WatchBlog in January, 2014, as part of its continuing effort to reach its audiences—Congress and the American people—where they are currently looking for information.

The blog format allows GAO to provide a little more context about its work than it can offer on its other social media platforms. Posts will tie GAO work to current events and the news; show how GAO’s work is affecting agencies or legislation; highlight reports, testimonies, and issue areas where GAO does work; and provide information about GAO itself, among other things.

Please send any feedback on GAO's WatchBlog to blog@gao.gov.