Increased Federal Role in the Housing Finance System

Housing finance is a complex, multi-trillion-dollar industry that played a major role in the 2007-2009 financial crisis. Two of our recent reports analyzed changes in the market since the crisis and their effect on taxpayers. We discuss our findings in today’s WatchBlog.

The process of pooling mortgages

After lenders make mortgage loans to homebuyers, they often sell the loans to third parties who pool these loans into mortgage-backed securities. Investors can then buy and trade these securities, similar to stocks and corporate bonds.

This process is intended to provide lenders with funding to make more loans and offer lower interest rates to borrowers.

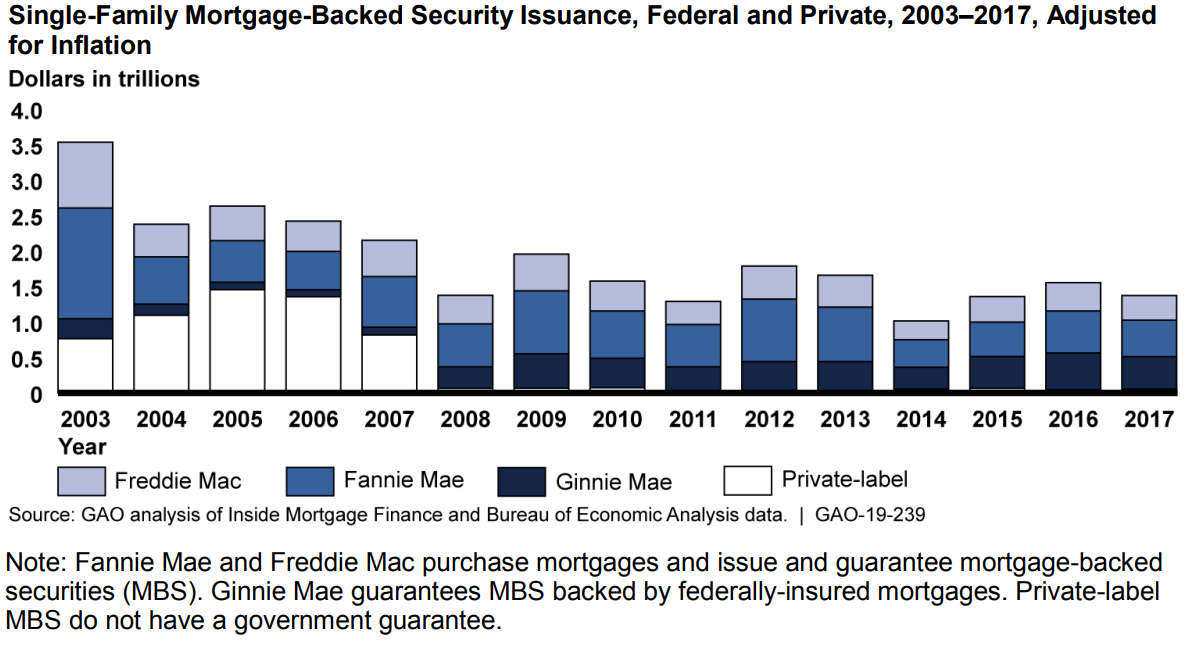

Government’s expanding role in housing finance

The main federal entities involved in housing finance include:

- Fannie Mae and Freddie Mac, which are government-sponsored enterprises (i.e., congressionally chartered private corporations that are publicly owned) that issue securities and guarantee the payment of principal and interest to investors in the event that borrowers default.

- Ginnie Mae, which is a federally owned corporation within the Department of Housing and Urban Development that guarantees securities that are composed entirely of federally insured mortgages. Unlike Fannie Mae and Freddie Mac, Ginnie Mae doesn’t issue securities.

Leading up to the 2007-09 financial crisis, some borrowers defaulted on their mortgages and Fannie Mae and Freddie Mac suffered losses because of their guarantee to pay securities investors. In 2008, the federal government took control of Fannie Mae and Freddie Mac out of concern their failure could upset U.S. financial stability.

Even though the market has largely recovered, the federal role in the housing market has increased. Fannie Mae, Freddie Mac, and Ginnie Mae issue or guarantee about 95% of new mortgage-backed securities, compared to about 50% in 2006.

Ginnie Mae’s risk to taxpayers

Notably, Ginnie Mae’s market share has grown dramatically. In 2007, it guaranteed $500 billion of mortgage-backed securities, and in 2018, it guaranteed $2 trillion—exposing it and taxpayers to a greater risk of loss. Our recent report found that Ginnie Mae faces resource and risk management challenges:

- Ginnie Mae operates with a limited staffing budget and relies heavily on contractors.

- Ginnie Mae has not assessed whether its mortgage-backed securities guaranty fee—which, among other things, helps ensure timely payment to investors—is set at an appropriate level in light of its growing risk exposure.

- HUD faces challenges in its oversight of Ginnie Mae.

To address these challenges, we recommended that Ginnie Mae review its staffing practices and conduct additional risk management analysis. We also suggested that Congress consider legislation to address these challenges and to reform Ginnie Mae’s oversight structure so it can better address its risks.

The need for housing finance reform

A decade after the crisis, Fannie Mae and Freddie Mac remain under government control—leaving taxpayers on the hook for any potential losses. Our recent report found that lack of action to resolve the long duration of the government’s takeover of Fannie Mae and Freddie Mac has led to uncertainty among market participants.

Congress and others have suggested different ways to reform the system to lessen the government’s role and address weaknesses. We reviewed 14 reform proposals and found that while they generally included certain key elements—such as addressing fiscal exposure—many proposals didn’t have clear goals or a system-wide focus. For instance, 7 proposals didn’t consider how reform might impact other federal entities, including Ginnie Mae.

We suggested that Congress consider legislation for the future federal role in housing finance that has clear goals and considers Ginnie Mae.

We also continue to include housing finance on our high-risk list.

Comments on GAO’s WatchBlog? Contact blog@gao.gov.

GAO Contacts

Image

Related Products

GAO's mission is to provide Congress with fact-based, nonpartisan information that can help improve federal government performance and ensure accountability for the benefit of the American people. GAO launched its WatchBlog in January, 2014, as part of its continuing effort to reach its audiences—Congress and the American people—where they are currently looking for information.

The blog format allows GAO to provide a little more context about its work than it can offer on its other social media platforms. Posts will tie GAO work to current events and the news; show how GAO’s work is affecting agencies or legislation; highlight reports, testimonies, and issue areas where GAO does work; and provide information about GAO itself, among other things.

Please send any feedback on GAO's WatchBlog to blog@gao.gov.