Paid Tax Return Preparers: Opportunities Remain to Improve IRS Oversight

Fast Facts

This Q&A report looks at paid tax preparers, who file returns for more than half of all taxpayers. Some paid preparers, such as CPAs, have credentials from IRS or a state, but the majority aren't subject to testing or education requirements.

Unqualified preparers can make serious errors that can cause taxpayers to lose out on benefits or subject them to audits or penalties. These errors can also lead to billions of dollars in improper payments and reduce federal revenue. But IRS only has the legal authority to oversee the credentialed preparers.

We've made several recommendations to help Congress and IRS strengthen oversight of paid preparers.

Tax documents, pens, and an iPhone on the official IRS website on a background of the U.S. flag.

Highlights

What GAO Found

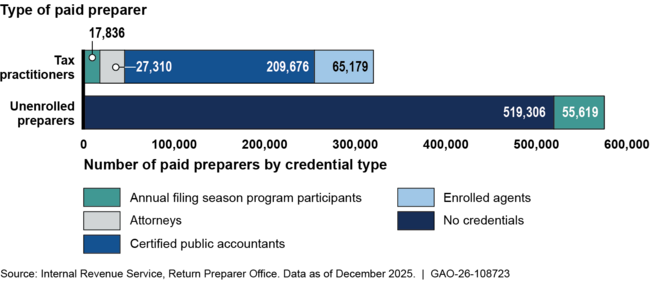

Paid preparers have differing levels of skills, education, and expertise. Tax practitioners include enrolled agents, certified public accountants, attorneys, and other individuals who possess some level of qualification or credentials issued by either Internal Revenue Service (IRS) or states. All other paid preparers without professional credentials are considered unenrolled preparers. While all paid preparers are required to have and use a Preparer Tax Identification Number (PTIN) and are subject to various requirements in the Internal Revenue Code, IRS only has the authority to regulate the practice of tax practitioners. Generally, unenrolled preparers are not subject to IRS regulation, including testing and education requirements.

Number and Type of Credentials Held by Paid Preparers for 2025

In prior work, GAO found that paid preparers can make serious errors on the tax returns they prepare. In addition, GAO’s prior work indicates that unenrolled preparers can make errors at a higher rate than taxpayers who prepare their own returns or who use other categories of paid preparers. When paid preparers make errors, taxpayers may overpay and lose out on tax benefits. Alternatively, when preparers understate tax liabilities, taxpayers may be subject to penalties and the government may collect less revenue.

GAO has previously reported that IRS uses various tools, including outreach and education, civil and criminal investigations, and penalties to oversee all paid preparers and bring them into compliance. For example,

- IRS’s Refundable Credits Return Preparer Strategy program identifies preparers who were potentially noncompliant with due diligence requirements and encourages them to comply. Actions IRS may take range from issuing warning letters and phone calls to preparers to more serious actions such as audits of preparers’ clients and IRS staff visits to preparers.

- IRS conducts civil and criminal investigations of abusive tax schemes, including those involving paid preparers.

- Paid preparers may be subject to penalties for noncompliance with certain requirements in the Internal Revenue Code.

Why GAO Did This Study

During fiscal year 2024, more than half of all individual taxpayers used a paid preparer, according to IRS data. Paid preparer errors can lead to billions of dollars in improper claims of refundable tax credits and can have negative consequences for individual taxpayers.

GAO was asked to examine IRS’s ability to oversee preparers. This report describes what GAO and other IRS oversight groups have previously reported on IRS’s oversight of paid preparers and recommended to improve its efforts.

GAO reviewed the Internal Revenue Code, relevant regulations and case law, information on paid preparer credentials, GAO’s previous issued work on paid preparer topics, and reports by other IRS oversight groups. Additionally, GAO analyzed data on numbers of preparers with a current PTIN and interviewed IRS officials.

Recommendations

GAO previously recommended that Congress take various actions to improve federal oversight of all paid preparers. These include the following:

- Granting IRS the authority to establish professional requirements for paid preparers.

- Providing IRS with explicit authority to establish security requirements for the information systems of paid preparers and authorized e-file providers.

GAO has also made numerous recommendations to IRS to improve its oversight of paid preparers that remain unimplemented and are described in the report.