Homeowners Insurance: Premiums Generally Tracked Inflation but Rose More in Disaster-Prone Areas

Fast Facts

Homeowners insurance helps people recover when disasters strike their homes. But it's becoming less affordable and available in certain areas.

Nationally, average premiums rose 3% during 2019–2024 but rose 25% or more in southern coastal areas. Risk from different natural disasters also affected premiums differently. For example, wind risk affected premiums more than wildfire risk.

We asked insurers, state regulators, and consumer advocates about options for making homeowners insurance more available or affordable. They supported options like tax deductions or credits for home upgrades to withstand disasters.

A Home Destroyed by the 2025 Eaton Fire in California

Partial burnt remains of a house’s walls and frames in the aftermath of a fire. Large piles of rubble are in the background.

Highlights

What GAO Found

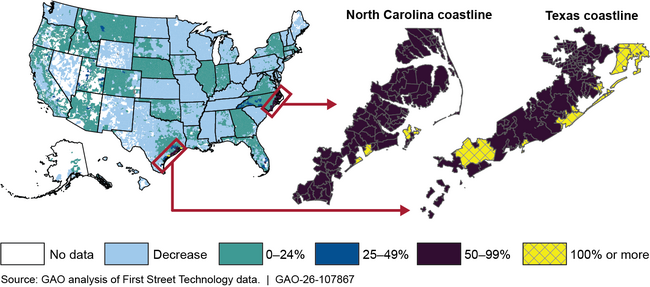

In recent years, while homeowners insurance premiums increased slightly nationwide, premiums grew more rapidly in certain areas of the country. Premiums as a percentage of 2023 median household income were highest in Florida, Louisiana, and Oklahoma. The average U.S. homeowners insurance premium rose 3 percent in 2019–2024, after adjusting for inflation. But rates in parts of certain states, particularly southern coastal areas at high risk of wind damage, increased 25 percent or more.

Estimated Total Change in Homeowners Insurance Premiums After Inflation, 2019–2024

The risk of different types of natural disasters can affect premiums to varying degrees. For example, GAO found that homes in areas with a high risk of wind damage had premiums about 58 percent higher than similar homes in areas with a medium level of wind risk. Moving from a medium to high level of wildfire risk was associated with an 8 percent increase in premiums. Increased risk of natural disasters also can reduce the availability of homeowners insurance.

Insurance is state-regulated. The time state regulators take to review requests to raise premiums varies, reflecting differences in regulations and regulator priorities. In 2020–2024, the longest median approval times were in Colorado (331 days) and California (305 days). Some homeowners in states in which regulators take longer to approve premium changes tend to have more difficulty obtaining insurance than in other states.

Some states have undertaken efforts to improve the availability and affordability of homeowners insurance, and legislation was introduced in Congress to support these efforts. GAO identified federal policy options that could improve the availability or affordability of the insurance. Stakeholders GAO surveyed expressed the strongest support for options that encourage mitigation, such as tax deductions or credits for building or upgrading homes to better withstand natural disasters. Stakeholders expressed mixed views on direct federal insurance or reinsurance programs and had concerns about federal costs and private market effects.

Why GAO Did This Study

Homeowners insurance plays a critical role in helping Americans recover from natural disasters, such as hurricanes and wildfires. But insurers have experienced rising losses from such disasters and homeowners in some areas experienced reduced affordability and availability of insurance. That is, insurance prices were greater than some homeowners could afford, and some were not able to obtain insurance.

GAO was asked to review issues related to homeowners insurance. This report examines trends in insurance availability and affordability, how insurance is priced and regulated, and views on federal policy options to increase availability and affordability.

GAO analyzed 2019–2024 data on private homeowners insurance and 2014–2023 information on insurers of last resort. GAO reviewed reports from government agencies, insurance industry groups, and consumer advocacy organizations. GAO interviewed representatives of the Federal Insurance Office, four insurance industry groups, three consumer advocacy organizations, and four state insurance regulators. GAO also sent a structured questionnaire on proposed policy options to 15 organizations, selected to obtain a range of views. GAO received responses from four industry associations, three consumer organizations, and three state regulators, for a 67 percent response rate. GAO also visited four states to speak with regulators and other stakeholders.

For more information, contact Alicia Puente Cackley at CackleyA@gao.gov.