Paycheck Protection Program: Program Changes Increased Lending to the Smallest Businesses and in Underserved Locations

Fast Facts

In response to COVID-19, Congress created the Paycheck Protection Program to help small businesses get low-interest loans.

But self-employed people and businesses owned by minorities, women, and veterans faced challenges getting loans, prompting the Small Business Administration to:

approve 600 new lenders-including nonbanks, who largely didn't participate in the first round of the program

develop guidance to encourage more self-employed people to apply

Also, Congress targeted funding to the smallest and minority-owned businesses.

We found that by June 2021, the changes helped increase loan access for the intended businesses.

Highlights

What GAO Found

The Paycheck Protection Program (PPP) supports small businesses through forgivable loans for payroll and other eligible costs. Early lending favored larger and rural businesses, according to GAO's analysis of Small Business Administration (SBA) data. Specifically, 42 percent of Phase 1 loans (approved from April 3–16, 2020) went to larger businesses (10 to 499 employees), although these businesses accounted for only 4 percent of all U.S. small businesses. Similarly, businesses in rural areas received 19 percent of Phase 1 loans but represented 13 percent of all small businesses. Banks made a vast majority of Phase 1 loans.

In response to concerns that some underserved businesses—in particular, businesses owned by self-employed individuals, minorities, women, and veterans—faced challenges obtaining loans, Congress and SBA made a series of changes that increased lending to these businesses. For example,

- SBA admitted about 600 new lenders to start lending in Phase 2 (which ran from April 27–August 8, 2020), including nonbanks (generally, lending institutions that do not accept deposits).

- SBA developed guidance after Phase 1 helping self-employed individuals participate in the program.

- SBA targeted funding to minority-owned businesses in part through Community Development Financial Institutions in Phases 2–3. (Phase 3 ran from January 12–June 30, 2021.)

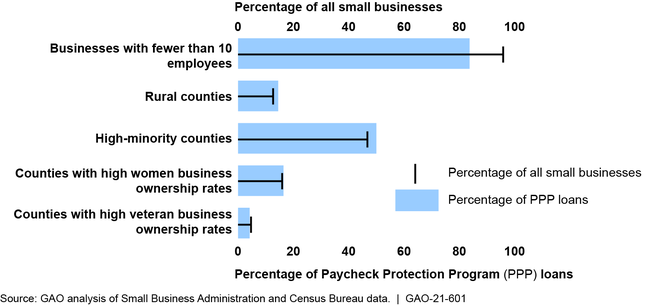

By the time PPP closed in June 2021, lending in traditionally underserved counties was proportional to their representation in the overall small business community (see figure). While lending to businesses with fewer than 10 employees remained disproportionately low, it increased significantly over the course of the program.

Paycheck Protection Program Loans, by Type of Business or County

Why GAO Did This Study

The COVID-19 pandemic resulted in significant turmoil in the U.S. economy, leading to temporary and permanent business closures and high unemployment. In response, in March 2020, Congress established PPP under the CARES Act and ultimately provided commitment authority of approximately $814 billion for the program over three phases. When initial program funding ran out in 14 days, concerns quickly surfaced that certain businesses were unable to access the program, prompting a series of changes by Congress and SBA.

The CARES Act includes a provision for GAO to monitor the federal government's efforts to respond to the COVID-19 pandemic. GAO has issued a series of reports on this program, and has made a number of recommendations to improve program performance and integrity. This report describes trends in small business and lender participation in PPP.

GAO analyzed loan-level PPP data from SBA and county-level data from four U.S. Census Bureau products and surveyed a generalizable sample of PPP lenders, stratified by lender type and size. GAO also reviewed legislation, interim final rules, agency guidance, and relevant literature, as well as interviewed SBA officials.

For more information, contact John Pendleton at (202) 512-8678 or pendletonj@gao.gov.