Tax Filing: Actions Needed to Address Processing Delays and Risks to the 2021 Filing Season

Fast Facts

The IRS faced numerous challenges during the 2020 filing season due to the COVID-19 pandemic. For example, it closed all processing facilities for several weeks for health and safety reasons. This, in turn, led to millions of pieces of unopened mail—including paper tax returns.

We reviewed IRS's efforts to process tax returns, serve taxpayers, and prepare for the 2021 filing season. We made 7 recommendations, including that IRS:

revise its estimates for addressing its 2020 backlog of work

identify alternate work assignments for staff on paid leave due to the pandemic

identify, assess, and address risks to the 2021 filing season

Highlights

What GAO Found

The 2020 filing season occurred during the global COVID-19 pandemic, introducing challenges that the Internal Revenue Service (IRS) had to respond to quickly to fulfill its mission-essential functions. IRS took steps to protect the integrity of its operations, help ensure the health and safety of its employees, and provide relief to taxpayers. For example, IRS closed all its processing and service facilities for several weeks before re-opening with health and safety measures and extended the filing season deadline to July 15, 2020.

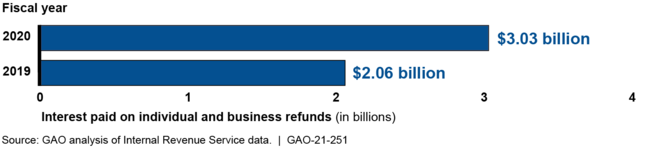

IRS's 2020 processing of e-filed returns was generally on par with prior years. However, IRS's overall 2020 performance was significantly impacted by its reliance on manual processes such as for paper returns, and its limited ability to process returns remotely while processing centers were closed. As a result, as of December 2020, IRS had a significant backlog of unprocessed returns and taxpayer correspondence. Additionally, costs increased including interest on delayed refunds which exceeded $3 billion in fiscal year 2020. IRS has not revised its estimates for addressing all of the backlog due to operational uncertainties created by the pandemic. Doing so would help IRS determine how best to address the backlog and perform 2021 filing season activities.

Refund Interest Paid to Taxpayers, Fiscal Years 2019 and 2020

GAO also found that about 23 percent of business tax returns were filed on paper even though an e-file option is available. IRS has not comprehensively identified barriers to business-related e-filing nor taken specific actions to increase e-filing. Doing so would help reduce the volume of costly paper-based work and improve services to business filers. Further, during the filing season, IRS transitioned nearly two-thirds of its phone customer service staff to telework, but was unable to do so for returns processing staff because most of its paper-based work is not set up to be performed remotely. As of late October 2020, about one-third of these staff remained on paid leave. Identifying and implementing alternative work assignments for staff that remain on paid leave would better support IRS operations and reduce costs.

IRS has not fully identified and assessed all risks to the 2021 filing season—including those exacerbated by the COVID-19 pandemic—consistent with enterprise risk management practices. IRS identified some risks in October 2020 after GAO raised concerns, but did not fully address all essential elements of enterprise risk management, such as identifying options for risk response. Doing so would better position IRS to respond to risks during the 2021 filing season. In early 2021, after receiving a draft of this report, IRS provided additional information on its risk management efforts. GAO will review this information to determine if these efforts are sufficient to address its recommendation.

Why GAO Did This Study

During the annual tax filing season, generally from January to mid-April, IRS processes more than 150 million individual and business tax returns and provides telephone, correspondence, online, and in-person services to tens of millions of taxpayers. Due to the COVID-19 pandemic and to provide relief to taxpayers, IRS extended the 2020 filing and payment deadline by 3 months to July 15, 2020.

GAO was asked to review IRS's performance during the 2020 filing season. This report (1) describes the changes IRS made to operations and services for the 2020 filing season due to the COVID-19 pandemic; (2) assesses IRS's performance on providing customer service and processing individual and business income tax returns during the 2020 filing season and compare to prior filing seasons, where appropriate; and (3) evaluates IRS's plans to prepare for the 2021 filing season.

GAO analyzed IRS documents, filing season performance data, and employee timecard data; assessed IRS's plans for the 2021 filing season; and interviewed cognizant officials.

Recommendations

GAO is making seven recommendations, including that IRS revise estimates for addressing its backlog; identify and address barriers to e-filing for business taxpayers; identify and consider implementing alternative work assignments for returns processing staff on paid leave; and identify and assess risks to the 2021 filing season. IRS agreed with four recommendations and disagreed with three. GAO believes that the recommendations remain warranted.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Internal Revenue Service |

Priority Rec.

The Commissioner of Internal Revenue should revise IRS's estimates for resolving its backlog of work from the 2020 filing season. (Recommendation 1) |

IRS disagreed with this recommendation and did not adjust its estimate for reducing this backlog of work. As a result, we are closing this recommendation as not implemented. In response to our March 2021 recommendation, IRS said it continued to monitor and assess the 2020 filing season carryover paper inventory daily. IRS also said that it adjusted processing priorities based on constantly changing variables that affect the paper inventory backlog, such as social distancing requirements and shutdowns in functional areas due to reported positive COVID-19 tests. In December 2021, IRS completed entering all remaining returns from 2020 into its systems for processing. As of April 2022, IRS officials said that, in general, these returns had been fully processed. However, they said IRS may be holding some returns from 2020 for review due to complex errors. In March 2023, IRS reported that it had processed all returns received in 2020, bringing this inventory to zero. We are tracking IRS's efforts to address its overall backlog of taxpayer correspondence in a separate priority recommendation.

|

| Internal Revenue Service | The Commissioner of Internal Revenue should track business refund processing, such as through IRS's weekly performance tracking. (Recommendation 2) |

IRS disagreed with this recommendation. In February 2021, IRS stated that it tracks, and management uses, information on the timeliness of business refund processing, and that a report to track business refunds will not be a useful mechanism for reducing interest on business refunds. However, during our review, IRS could not tell us the extent to which business tax refunds were delayed during the 2020 filing season because it does not monitor and report on this information. As a result, IRS does not know how well it is processing business returns with refunds, or the extent to which it will have to pay refund interest, which was $10.2 billion in fiscal year 2023 and $5.3 billion in fiscal year 2024. As of December 2025, IRS continued to disagree with this recommendation and planned no action. We continue to believe this recommendation is valid, given the large amounts of refund interest paid in recent years. We will continue to monitor this issue.

|

| Internal Revenue Service | The Commissioner of Internal Revenue should conduct an assessment to comprehensively identify barriers taxpayers face to e-filing business-related returns. (Recommendation 3) |

IRS agreed with GAO's March 2021 recommendation and has identified barriers that taxpayers face in e-filing business-related returns. In January 2021, IRS provided documentation on research it had conducted from 2015 to 2017 on the barriers associated with e-filing three business-related tax forms, including employment returns, which account for IRS's largest volume of business-related paper returns. In January 2022, IRS officials stated that the e-file barriers they identified several years ago are still relevant because IRS has taken limited action to address the barriers due to competing priorities. To supplement their initial research, IRS officials then provided results from follow-up efforts in September 2018 and November 2020 that align with the results of their initial work on why taxpayers continue to file employment returns on paper. Collectively, these efforts identify barriers to taxpayers e-filing business-related returns. The information from these efforts should help IRS better prioritize its next steps for addressing e-file barriers for business taxpayers.

|

| Internal Revenue Service | The Commissioner of Internal Revenue should, after completing the barrier assessment in recommendation 3, determine what actions IRS could take to address the barriers and implement those actions, as feasible. (Recommendation 4) |

IRS agreed with GAO's March 2021 recommendation and has taken some steps to address barriers taxpayers face to e-filing business-related returns. To address the greatest barrier it identified to increasing e-filing rates for employment returns, IRS officials told us they intend to develop an online signature personal identification number (PIN) for businesses. The online signature PIN would be a fully automated application and approval process that could issue the number in real time rather than using the current process, which takes at least 45 days to issue a PIN. As of August 2025, IRS officials said the barrier to this project is funding and that it is in a pending status. In addition, to make it easier for businesses to e-file returns, in 2024, IRS began making more tax forms used by businesses available to file electronically. Addressing barriers to e-filing business returns could help IRS reduce the volume of more costly paper-based work and improve services to business filers. We will continue to monitor IRS's progress on these efforts.

|

| Internal Revenue Service | The Commissioner of Internal Revenue should identify and consider implementing actions to transition staff currently on weather and safety leave to active work status, as appropriate. This could include reassigning staff to other tasks that can be performed remotely. (Recommendation 5) |

IRS disagreed with GAO's March 2021 recommendation and at that time, stated that it had taken all reasonable steps to identify work that can be performed remotely and assigned it to staff that had previously been on weather and safety leave. Prior to GAO's report being issued, IRS recalled mission-essential staff who performed in-person work and who were previously on weather and safety leave to report to the office to support 2021 filing season activities. As of January 31, 2021, mission-essential IRS staff were unable to use weather and safety leave due to concerns with reporting in-person due to the COVID-19 pandemic. As of February 2022, GAO is closing this recommendation as not implemented, since IRS recalled affected employees back to on-site work.

|

| Internal Revenue Service | The Commissioner of Internal Revenue should identify and document all risks to the 2021 filing season; conduct a comprehensive risk assessment, including determining the likelihood of these risks occurring and potential impact of these risks on IRS's ability to carry out its mission-essential functions; and identify options to respond to each identified risk. (Recommendation 6) |

IRS agreed with this recommendation and took steps to address it. Specifically, in February 2021, IRS said that it had implemented actions to document risks to the 2021 filing season and had completed a risk assessment. For example, IRS stated that the Filing Season Readiness Executive Steering Committee had developed a risk register statement and corresponding strategies to address items that could impact the integrity of the 2021 filing season. After receiving our draft report, in January 2021, IRS provided us with several monthly reports describing the impact of COVID-19 on its filing season operations and its recovery efforts. IRS's first report was in June 2020 and monthly updates were provided through March 2021. In the reports, IRS described the risks and potential impacts to the filing season such as in the areas of hiring, employee retention, and physical space issues due to social distancing. According to IRS officials, these documents indicate that IRS considered some COVID-19-related risks to the 2021 filing season prior to October 2020 that it did not document in the filing season planning documents that it had provided during out audit. Additionally, in October 2021, IRS provided updated information on its risk management efforts, including mitigation strategies. IRS's continued attention to this area will help promote transparency and public confidence that the agency is effectively managing filing season risks.

|

| Internal Revenue Service | The Commissioner of Internal Revenue should, after completing the comprehensive risk assessment in recommendation 6, monitor risks, and communicate IRS's plans to manage risks and provide status updates to stakeholders. (Recommendation 7) |

In February 2021, IRS agreed with this recommendation. After receiving our draft report, in January 2021, IRS provided us with several monthly reports describing the impact of COVID-19 on its filing season operations and its recovery efforts. IRS stated that its monthly reports provided opportunities for continued risk management of the 2021 filing season. However, IRS did not indicate how it would communicate its plans to manage risks and provide status updates to stakeholders. In December 2021, IRS provided documentation demonstrating how it informed stakeholders of its plans to address identified risks to the 2021 filing season. For example, IRS held regular meetings during the 2021 filing season with members of Congress as well as regular meetings with the tax preparer community. During these meetings, IRS shared information on filing season performance and actions it was taking to manage risks. IRS also provided examples of public messaging intended to help manage risks. For example, one risk IRS identified was delays in processing paper returns due to the pandemic and hiring challenges. To mitigate this risk, IRS relied on press releases to encourage taxpayers to file electronically and request direct deposit for their refunds. IRS also provided regular operating status updates and alerts on irs.gov. These actions helped IRS promote transparency and confidence that the agency was effectively managing risks.

|