U.S. Postal Service: Additional Guidance Needed to Assess Effect of Changes to Employee Compensation

Fast Facts

In the past 11 years, USPS’s revenue hasn’t covered its costs. To help address this, USPS lowered its employee compensation costs—a significant part of its expenses—mostly by paying new employees less.

We found USPS overestimated its cost savings from these efforts. We substantiated $8 billion in savings and found USPS’s estimates ($9.7 billion in 2016-2018) may be overstated. Also, USPS’s estimates didn’t consider factors like training and other costs associated with increased turnover due to lower wages.

We recommended including turnover and other factors in savings estimates so USPS has information it needs to better assess its workforce.

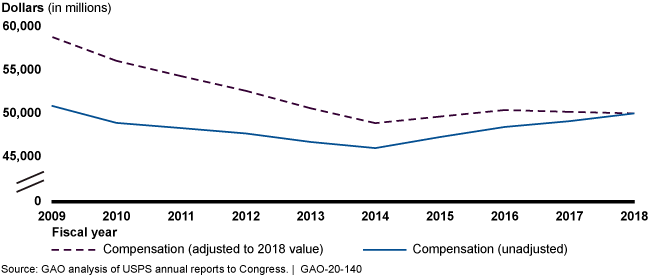

Compensation Costs for Current USPS Employees for Fiscal Years 2009 through 2018

Line graph showing declines in compensation costs adjusted to 2018 value and unadjusted

Highlights

What GAO Found

Compensation costs for current United States Postal Service (USPS) employees are $9 billion lower than 10 years ago, when adjusted for inflation (see fig). Most of the decline happened in fiscal years 2009 through 2014 as a result of reductions in the number of USPS employees and the hours they worked. While compensation costs have increased in recent years, USPS reports that more work hours were necessary to handle growth in delivery points and labor intensive packages. In recent years, USPS has also failed to make required payments for retiree health and pension benefits—a total unfunded liability of about $110 billion.

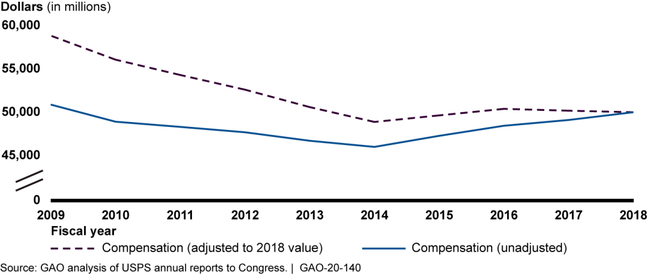

Compensation Costs for Current USPS Employees for Fiscal Years 2009 through 2018

USPS estimates a savings of about $9.7 billion from fiscal years 2016 through 2018 as a result of paying new employees less, among other efforts. GAO substantiated about $8 billion in savings, and found that USPS's cost savings estimates are likely overstated because they do not fully account for changes in work hours or tenure of employees. Also, USPS did not account for other costs such as increased turnover rates among lower-paid employees. USPS lacks guidance on what factors to consider in its cost savings estimates, and as a result may make future changes to employee compensation based on incomplete information.

Changes to employee compensation that would require legislative change could save USPS billions, but the amount saved is dependent on USPS overcoming implementation challenges. If USPS could reduce delivery frequency and associated work hours, GAO estimated USPS could save billions a year. However, other recent USPS reductions in service have not fully achieved planned work hour reductions due to, among other things, issues with management of work hours and lack of union agreement. Changing employee pay and benefit requirements could also achieve significant long-term savings, but saving depends on USPS overcoming challenges, such as potential increases in turnover and reduced productivity resulting from decreases in pay and benefits.

Why GAO Did This Study

USPS faces major financial challenges. In the last 11 years it has lost over $69 billion; an issue for an organization that is to be self-sufficient. Significant USPS expenses are concentrated in employee compensation—72 percent of its costs in fiscal year 2018—and USPS has taken actions to decrease these costs. GAO was asked to review issues related to USPS's employee compensation.

This report examines: (1) recent trends in postal employee compensation, (2) the results of recent USPS efforts to manage compensation and (3) potential effects of proposed changes to employee compensation that would require legislative change. GAO analyzed USPS employee payroll data from fiscal years 2009 through 2018 to determine compensation trends and impacts of management efforts to manage compensation. GAO reviewed relevant legal documents, USPS policy documents and collective bargaining agreements. GAO assessed four broad reviews of USPS including recommendations for legislative change related to pay, benefits and required workhours. GAO also interviewed USPS officials, officials representing USPS employee unions, and industry and mailer stakeholders.

Recommendations

GAO recommends that USPS develop guidance that specifies that cost estimates include important factors, such as turnover. USPS accepted this recommendation stating it would formally articulate internal guidance to ensure appropriate factors are taken into account when developing cost estimates and evaluating outcomes.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| United States Postal Service | The Postmaster General should direct executive leaders to develop guidance for cost savings estimates related to employee compensation specifying that analysis used to calculate estimates should, to the extent possible, include significant factors, such as work hours, tenure, and turnover. (Recommendation 1) |

USPS has significant financial challenges and is unable to cover its expenses with the revenue it generates from the sale of products and services. According to USPS, most of its annual costs are related to its employees. In response to this situation, USPS has taken actions in recent years to reduce employee compensation costs. According to USPS management officials, these actions were intended to decrease compensation costs and increase workforce flexibility. In 2020, we estimated that while these actions saved USPS billions of dollars, they likely did not save USPS as much as it estimated because USPS did not consider important factors such as work hours and tenure. There are a variety of acceptable methods for conducting cost savings estimates, but all estimates should include relevant factors driving costs and be clearly documented. At the time, USPS officials said they did not have guidance for how to develop cost savings estimates, including what significant factors should be considered. Given that USPS regularly evaluates and manages employee compensation in its labor negotiations, as well as overall budget planning, without guidance on what factors are necessary to consider when developing employee compensation cost estimates, USPS risks making ill-informed decisions about whether to maintain, or make additional, changes to compensation. Therefore, we recommended that the Postmaster General direct executive leaders to develop guidance for cost savings estimates related to employee compensation. Specifically, guidance should advise that cost savings estimates should, to the extent possible, include significant factors known to impact employee costs, such as work hours, tenure, and turnover. In late 2020, USPS management issued guidance about cost savings estimates, noting that significant factors such as work hours, tenure, and turnover be utilized, as appropriate. USPS also provided us with an example of how it now conducts cost-benefit analyses, using a variety of factors, when considering changes to employee compensation. Conducting analyses in this way will likely help USPS make better informed decisions about potential cost savings related to any future workforce changes.

|