Retirement Accounts: Federal Action Needed to Clarify Tax Treatment of Unclaimed 401(k) Plan Savings Transferred to States

Fast Facts

What happens if you lose track of some of your retirement funds—such as a 401(k) from a prior employer? The companies holding those unclaimed accounts can take the money out and transfer it to states. States hold the money as lost property until the owners claim it.

But whenever money comes out of a tax-deferred account, there are taxes to consider. We looked at how IRS treats these transfers for tax purposes.

While there is some guidance from IRS and the Department of Labor on these transfers, IRS hasn't clarified tax reporting and withholding requirements for employers transferring unclaimed retirement funds. We recommended IRS do so.

Five $100 bills are on a table beside a broken piggy bank.

Highlights

What GAO Found

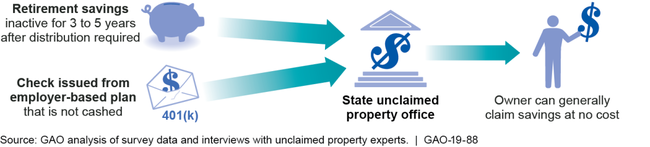

Millions of dollars in retirement savings are transferred to states as unclaimed property, only some of which is later claimed by owners. Of the 22 states responding to GAO's survey, 17 states provided data indicating that $35 million in unclaimed retirement savings was transferred to them from employer plans and individual retirement accounts (IRAs) in 2016. When account owners do not claim money from retirement savings accounts or cash checks from their plans, the funds may be transferred to state unclaimed property offices (see fig.). Assets and uncashed checks from employer plans (such as 401(k) plans), were the most common form of retirement savings transferred to states. After funds are transferred, owners can claim their savings from the state. According to the 15 states providing data on this, owners claimed about $25 million in retirement savings in 2016: $601, on average, from 401(k) plan checks, and $5,817, on average, from traditional lRAs. States reported using a range of strategies to maintain the value of retirement savings while holding these funds, such as applying interest. States also reported various efforts to locate owners. However, not all savings will be claimed because, among other reasons, owner information is not always associated with transferred savings when the amount is small, which complicates state efforts to locate some owners.

Stakeholders Described How Retirement Savings Are Transferred to and Claimed from States

The Internal Revenue Service (IRS) and the Department of Labor (DOL) have issued guidance on transferring retirement savings to states; however, IRS has not clarified certain responsibilities or ensured that the retirement savings that owners claim from states can be rolled over into other tax-deferred retirement accounts. IRS is responsible for communicating and enforcing tax responsibilities, but has not specified whether 401(k) plan providers should report state transfers to IRS as distributions and withhold federal income taxes. IRS officials said the agency has not issued guidance to clarify this issue because of competing priorities. As a result, 401(k) plan provider practices vary—some providers withhold taxes when transferring savings to states while others do not. This makes the IRS less likely to collect federal income taxes that may be due if transfers are taxable events. IRS also has not taken action to ensure that individuals who claim 401(k) savings from a state can roll over these savings to other tax-deferred retirement accounts after IRS's 60-day deadline. IRS allows individuals to roll over savings after 60 days for several reasons, none of which include claiming 401(k) savings from a state. Federal law seeks to protect the interests of participants in retirement plans. Account owners who are unable to roll over their reclaimed savings forgo the opportunity to continue investing the funds on a tax-deferred basis.

Why GAO Did This Study

Over the course of individuals' careers, their retirement savings can be spread across multiple retirement accounts and they can change jobs, both of which can cause their savings to become unclaimed and even lost. Prior GAO work has found that unclaimed retirement savings are sometimes transferred to the states. GAO was asked to review such transfers.

This report examines (1) how much in retirement savings is transferred to states as unclaimed property and what happens to those savings once transferred and (2) the steps IRS and DOL have taken to oversee these transfers and what improvements are needed. GAO interviewed federal and state officials, industry representatives, and other stakeholders, and surveyed all 50 states and the District of Columbia (and received 22 responses). GAO also surveyed 401(k) plan service providers and IRA trustees regarding the volume of retirement savings transferred to states and their federal tax reporting and withholding practices for those transfers.

Recommendations

GAO is making three recommendations, including that IRS should consider clarifying whether transfers from employer-based plans (such as 401(k) plans) to states constitute reportable and taxable distributions and consider modifying its list of permitted reasons for rolling over savings after the 60-day rollover deadline. IRS agreed with our recommendations and noted that it will work with the Department of the Treasury to address them.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Internal Revenue Service | The IRS Commissioner should work with the Department of the Treasury to consider clarifying if transfers of unclaimed savings from employer-based plans (such as 401(k) plans) to states are distributions, what, if any, tax reporting and withholding requirements apply, and when they apply. (Recommendation 1) |

In November 2020, IRS published guidance that clarifies that distributions from qualified plans to state unclaimed property funds are subject to federal income tax withholding and that qualified plans are generally required to report these transfers to IRS as designated distributions on IRS Form 1099-R for the year in which the distribution occurs.

|

| Internal Revenue Service | The IRS Commissioner should work with the Department of the Treasury to consider adding retirement savings transferred to states from terminating DC plans to the list of permitted reasons for rolling over savings after the 60-day rollover period, in a form consistent with the rules adopted on the taxation of transfers of unclaimed retirement savings. (Recommendation 2) |

In November 2020, IRS published guidance that clarifies that a distribution made from an eligible retirement plan (such as a qualified retirement plan or an IRA) to a state unclaimed property fund is a basis for a taxpayer to self-certify eligibility for a waiver of the 60-day rollover requirement.

|

| Department of Labor | The Secretary of Labor should specify the circumstances, if any, under which uncashed distribution checks from active plans can be transferred to the states. (Recommendation 3) |

On January 14, 2025, EBSA published Field Assistance Bulletin No. 2025-01, which addresses this recommendation. This guidance specifies the circumstances under which active retirement plans can transfer unclaimed savings, including uncashed checks, to states. Prior to that, the ERISA Advisory Council (EAC) explored whether there are circumstances under which a defined benefit or defined contribution pension plan might consider voluntary transfers of uncashed distribution checks to a state unclaimed property program to advance the goal of reuniting participants and beneficiaries who cannot be found or who are nonresponsive (missing participants) with their retirement savings. The EAC submitted and posted its report and recommendations in November 2019. In addition, the SECURE 2.0 Act passed in FY23 included a requirement for DOL to establish an online searchable database, known as the Retirement Savings Lost and Found, to help individuals find retirement plans in which they may have lost track of savings. DOL is coordinating with the Treasury Department/IRS and SSA to get access to data needed for the searchable database, and working on other activities related to developing this database. DOL will include this recommendation in its consideration of the Lost and Found, including the extent to which information would need to be collected from plans and/or state unclaimed property funds about amounts transferred to specific state unclaimed property funds.

|