Tax Debt Collection: IRS Needs to Define Field Program Objectives and Assess Risks in Case Selection

Highlights

What GAO Found

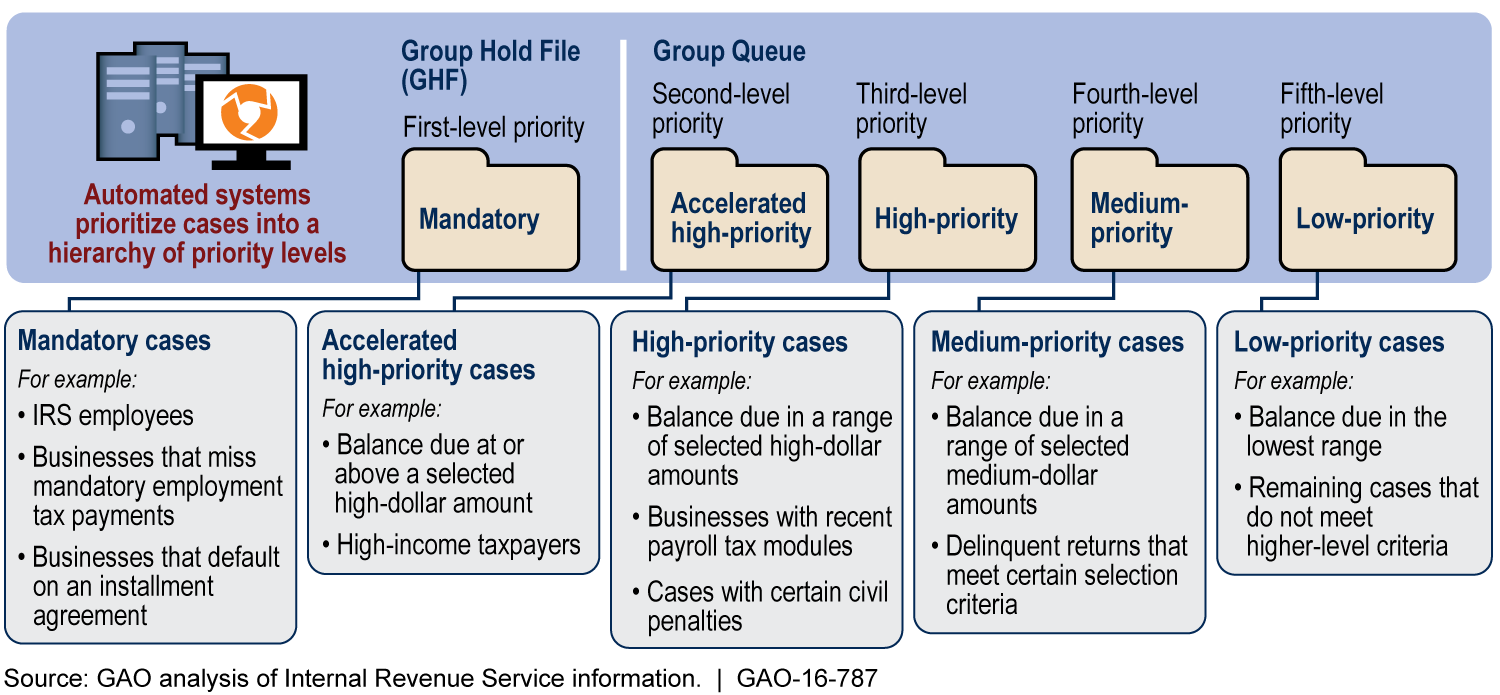

The Internal Revenue Service (IRS) uses automated processes to prioritize cases to be potentially selected for in-person contact to resolve a tax collection issue (see figure), but group managers in the Field Collection program manually select the cases to assign to revenue officers. For example, when reviewing cases, group managers consider characteristics of the revenue officer available—such as current workload—and case characteristics—such as potential collectability—when deciding whether to assign a case.

IRS Field Collection Case Prioritization

GAO found weaknesses in the Field Collection program's internal controls for case selection, including:

Program objectives are not clearly defined and communicated. IRS has not sufficiently developed and communicated specific and measurable program objectives, including fairness. GAO heard different interpretations of program objectives and the role of fairness from focus group participants. Without clearly defined and clearly understood objectives aligned to its mission, Field Collection management does not have reasonable assurance that case selection processes support achievement of that mission. Further, the lack of clearly articulated objectives undercuts the effectiveness of Field Collection management's efforts to measure performance and assess risks.

Documentation and assessment of case selection risks are inadequate. The Field Collection program's automated prioritization and decision support systems are control procedures that may guide staff to reduce risks. However, the Field Collection program does not have documented procedures for periodically reviewing automated aspects of case selection. Further, the Field Collection program lacks sufficient guidance for group managers to exercise judgment in case selection. These deficiencies limit the Field Collection management's ability to provide reasonable assurance that selection decisions effectively support achievement of IRS's mission.

Why GAO Did This Study

IRS's Field Collection program is where IRS revenue officers make in-person contact with noncompliant individuals and business officials to enforce tax return filing and payment requirements. Sound processes for selecting cases are critical to maintain taxpayer confidence in the tax system and use federal resources efficiently. GAO was asked to review the processes IRS uses to select collection cases for potential enforcement action.

This report (1) describes the Field Collection program's automated and manual processes for prioritizing and selecting cases and (2) assesses how well Field Collection case selection processes support the collection program's mission, including applying tax laws “with integrity and fairness to all.” To address these objectives, GAO reviewed IRS documents and conducted interviews with IRS officials knowledgeable about the case selection processes, including a series of focus groups with IRS Field Collection managers. GAO evaluated how well the processes adhere to relevant federal standards for internal control.

Recommendations

GAO is making five recommendations, including that IRS: develop and document objectives in clear and measurable terms, including fairness; provide guidance for group managers' use of judgment in selecting cases; and develop procedures to assess automated and manual processes. IRS agreed with the recommendations and outlined planned steps to address them.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Internal Revenue Service | To ensure that Field Collection program case selection processes support IRS's and the Collection program's mission, including applying tax laws with integrity and fairness to all, the Commissioner of Internal Revenue should develop, document, and communicate Field Collection program and case selection objectives, including the role of fairness, in clear and measurable terms sufficient for use in internal control. |

IRS agreed with the recommendation and described actions being taken to address it. After providing us proposed draft program and case selection objectives for review, in October 2022, IRS provided objectives that officials said were finalized. The objectives appeared to be clear and useful for internal control to manage the program, as IRS documents showed two objectives on fairness and case selection along with automated and manual controls in place to support achieving them. The objectives appeared measurable because IRS had clearly linked performance measures to them. However, it was not clear that IRS had formally adopted the objectives and communicated them. IRS officials said they planned to communicate the objectives by publishing them in the Internal Revenue Manual (IRM) by April 2023. IRS later extended that timeframe while GAO and IRS continued to communicate about planned IRM revisions through February 2024. In July 2024 IRS said it planned to communicate Field Collection program and case selection objectives in the IRM as soon as December 2024. We will update the status of IRS's implementation of the recommendation after we complete review of any documents IRS provides on further actions taken, as we requested in February 2025.

|

| Internal Revenue Service | To ensure that Field Collection program case selection processes support IRS's and the Collection program's mission, including applying tax laws with integrity and fairness to all, the Commissioner of Internal Revenue should develop, document, and implement performance measures clearly linked to the Field Collection program and case selection objectives. |

IRS agreed with the recommendation and outlined planned actions to address it. In October 2022, IRS provided documented objectives that officials said were finalized that included clear links between performance measures and objectives. For example, IRS linked a percentage measure of open cases that are high priority to objectives on fairness and case selection. However, it was not clear that IRS had implemented the performance measures by formally approving and communicating them, along with any target goals for the measures. Also it was not clear that IRS had formally adopted the objectives and communicated them. IRS officials said they planned to communicate the objectives by publishing them in the Internal Revenue Manual (IRM) by April 2023. IRS later extended that timeframe while GAO and IRS continued to communicate about planned IRM revisions through February 2024. In July 2024 IRS said it planned to communicate Field Collection program and case selection objectives in the IRM as soon as December 2024. We will update the status of IRS's implementation of the recommendation after we complete review of any documents IRS provides on further actions taken, as we requested in February 2025.

|

| Internal Revenue Service | To ensure that Field Collection program case selection processes support IRS's and the Collection program's mission, including applying tax laws with integrity and fairness to all, the Commissioner of Internal Revenue should incorporate program and case selection objectives into existing risk management systems or use other approaches to identify and analyze potential risks to achieving those objectives so that Field Collection can establish risk tolerances and appropriate control procedures to address risks. |

IRS agreed with the recommendation and outlined planned actions to address it. In October 2022, IRS officials provided documents that demonstrated risk management actions taken based on Field Collection program and case selection objectives that were finalized. For example, for Field Collection objectives on fairness and case selection, IRS identified and analyzed the risk of automated case prioritization not functioning as intended and the risk of Field group managers not assigning primarily high-priority cases. These risks could potentially result in Field Collection not assigning work in alignment with business priorities and unfair treatment of compliant taxpayers because of IRS not addressing egregious tax delinquency cases. IRS also established a related control procedure to periodically review and validate automated routing and prioritization rules. IRS also established a related risk tolerance, with a proposed goal to maintain 80 percent of its open cases as high-priority. Additionally, Field Collection established procedures to use its internal risk register to track the Field group manager risk along with the internal controls used to address it and procedures to periodically validate the effectiveness of controls. However, IRS has not yet completed steps to formally adopt and communicate the Field Collection program and case selection objectives that these risk management actions are supposed to support. IRS officials said they planned to communicate the objectives by publishing them in the Internal Revenue Manual (IRM) by April 2023. IRS later extended that timeframe while GAO and IRS continued to communicate about planned IRM revisions through February 2024. In July 2024 IRS said it planned to communicate Field Collection program and case selection objectives in the IRM as soon as December 2024. We will update the status of IRS's implementation of the recommendation after we complete review of any documents IRS provides on further actions taken, as we requested in February 2025.

|

| Internal Revenue Service | To ensure that Field Collection program case selection processes support IRS's and the Collection program's mission, including applying tax laws with integrity and fairness to all, the Commissioner of Internal Revenue should develop, document, and communicate control procedures guidance for group managers to exercise professional judgment in the Field Collection program case selection process to achieve fairness and other program and collection case selection objectives. |

IRS agreed with the recommendation and described actions it will take to address it. In September 2020, IRS officials said they had revised the Internal Revenue Manual to guide group managers on elements to consider in selecting cases. We view this as a positive development. However, until IRS formally adopts and communicates the program objectives and related measures, we are unable to determine how those procedures help ensure they support the achievement of program objectives. IRS officials said they planned to communicate the objectives by publishing them in the Internal Revenue Manual (IRM) by April 2023. IRS later extended that timeframe while GAO and IRS continued to communicate about planned IRM revisions through February 2024. In July 2024 IRS said it planned to communicate Field Collection program and case selection objectives in the IRM as soon as December 2024. We will update the status of IRS's implementation of the recommendation after we complete review of any documents IRS provides on further actions taken, as we requested in February 2025.

|

| Internal Revenue Service | To ensure that Field Collection program case selection processes support IRS's and the Collection program's mission, including applying tax laws with integrity and fairness to all, the Commissioner of Internal Revenue should develop, document, and implement procedures to periodically monitor and assess the design and operational effectiveness of both automated and manual control procedures for collection case selection to assure their continued effectiveness in achieving program objectives. |

IRS agreed with the recommendation and outlined planned actions to address it. In October 2022, IRS provided documentation on procedures to periodically monitor and assess the design and operational effectiveness of both automated and manual control procedures for collection case selection based on Field Collection program and case selection objectives that were finalized. For example, the documents identified the automated controls in place to achieve Field Collection objectives on fairness and case selection and set forth related monitoring procedures to periodically review and validate automated routing and prioritization rules. More specifically, the document set out plans to monitor inventory reports on a weekly and monthly basis to note any anomalies and ensure inventory delivery is functioning as expected. IRS also set forth plans to conduct an annual prioritization process review of all rules to add, modify, or delete rules when appropriate; validate the rules to ensure they are functioning as intended; or create new rules to meet a new or existing business priority. IRS also set forth procedures to guide group managers in using professional judgement in manual case selection and use its internal risk register to track the related risk of Field group managers not assigning sufficient numbers of high-priority cases, along with the internal controls used to address the risk and procedures to periodically validate the effectiveness of controls. However, it was not clear how IRS would follow through to assure full implementation of all these procedures, such as through formal management directives about specifically when and how the monitoring and assessments would be conducted, documented, and reported. In addition, IRS provided no results of any completed monitoring or assessments of the design and operational effectiveness of an automated or manual control procedure. Furthermore, IRS has not yet completed steps to formally adopt and communicate the Field Collection program and case selection objectives that the control procedures--and related monitoring and assessing of their design and operational effectiveness--are supposed to support. IRS officials said they planned to communicate the objectives by publishing them in the Internal Revenue Manual (IRM) by April 2023. IRS later extended that timeframe while GAO and IRS continued to communicate about planned IRM revisions through February 2024. In July 2024 IRS said it planned to communicate Field Collection program and case selection objectives in the IRM as soon as December 2024. We will update the status of IRS's implementation of the recommendation after we complete review of any documents IRS provides on further actions taken, as we requested in February 2025.

|