International Remittances: Money Laundering Risks and Views on Enhanced Customer Verification and Recordkeeping Requirements

Highlights

What GAO Found

Financial institutions, such as money transmitters and depository institutions that provide remittance transfers—funds sent from individuals in one country to a recipient in another country—are subject to anti-money laundering (AML) requirements under the Bank Secrecy Act (BSA). For example, these remittance providers must report suspicious and other transactions, and obtain and record information for each funds transfer of $3,000 or more. Remittance providers GAO spoke with identified challenges related to BSA compliance—including monitoring large amounts of remittance data to identify and prevent illicit activity, and keeping up to date with the changing behavior of criminals. Further, some banks have ended account relationships with money transmitters—which need bank accounts to conduct business. Money transmitters going out of business could lead remittance senders to use informal methods that are less detectable.

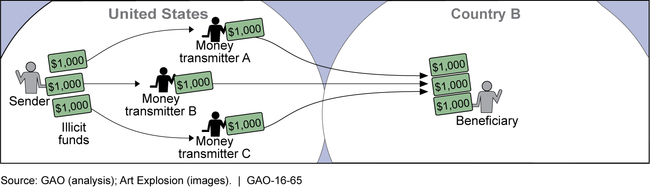

Remittances can pose money laundering risks, as funds related to illicit activity may go undetected due to the large volume of transactions or remittance providers' inadequate oversight of the various entities involved. Stakeholders identified money laundering risks associated with customers, geographic location, products, and agents (entities authorized to provide remittances) that may fail to follow BSA requirements. Remittances can be used to launder proceeds from different types of criminal activities, including drug trafficking and human smuggling, through methods such as structuring. For example, as the figure shows, a sender may structure remittances by breaking up a transaction into multiple transactions to avoid the $3,000 funds transfer threshold.

Example of Structuring to Launder Illicit Funds

Many stakeholders said that a lower dollar threshold would benefit agencies' AML efforts, but verifying remitters' legal immigration status might not benefit such efforts. Law enforcement officials GAO spoke with said that a centralized database of remittances—one potential result of a proposed rule that would require remittance providers to report certain remittances data at a low dollar threshold—would be useful in assisting AML efforts. Larger remittance providers generally did not object to lowering the funds transfer threshold because they had already self-imposed lower thresholds. But bank regulators and some stakeholders said that a lower threshold could create additional recordkeeping requirements and costs for smaller providers and for customers. Stakeholders generally expressed concern that a requirement to check the legal status of a remittance sender might not assist AML efforts because it could lead senders to use less detectable forms of transmitting money.

Why GAO Did This Study

The World Bank has estimated remittance outflows will reach $586 billion in 2015. However, some reports have indicated that remittance providers may be vulnerable to money laundering. Remittance providers are generally subject to both federal and state oversight.

GAO was asked to examine the potential illicit uses of remittances and assess whether requiring remittance senders to provide certain types of identification at a threshold below the current $3,000 level would be useful for U.S. AML efforts. This report examines (1) BSA remittance requirements that exist for remittance providers and related challenges that remittance providers face in complying with these requirements; (2) money laundering risks that remittances pose; and (3) stakeholders' views on the extent to which requiring remittance providers to verify identification and collect information at a lower dollar transaction amount than is currently required, or adding a requirement to verify legal immigration status, would assist federal agencies' AML efforts. GAO reviewed laws and regulations, analyzed compliance data, and interviewed stakeholders (Financial Crimes Enforcement Network, regulators, remittance providers, law enforcement, and industry and other associations). GAO also interviewed a nongeneralizable selection of five money transmitters and four depository institutions based on factors such as remittance volume.

GAO is not making recommendations in this report. Agencies provided technical comments, which we incorporated as appropriate.

For more information, contact Lawrance L. Evans, Jr. at (202) 512-8678 or evansl@gao.gov.