Consumer Financial Protection Bureau: Observations from Small Business Review Panels

Highlights

What GAO Found

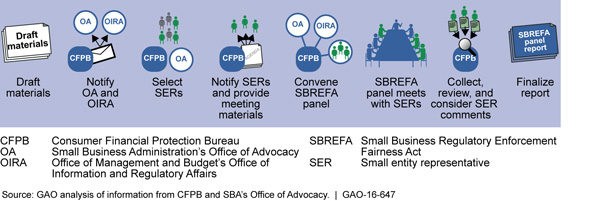

The Consumer Financial Protection Bureau (CFPB) has taken steps to solicit, consider, and incorporate inputs from small entities into its rulemaking process, as required by the Regulatory Flexibility Act, as amended by the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act). GAO reviewed documents from the four Small Business Regulatory Enforcement Fairness Act (SBREFA) panels that resulted in final rulemaking as of April 2016 and found CFPB completed required steps for conducting them (see fig.). CFPB addressed required elements for regulatory analyses that are components of the proposed and final rules. Based on a review of selected rules, GAO observed that the discussion of rule proposals and alternatives focused on reactions to proposals and alternatives CFPB presented. Some alternatives that small entity representatives raised at panels were discussed in a significant alternatives section of the proposed rules, while others were not. CFPB officials noted that data needed to make a fuller assessment of some alternatives from small entities were not always available. CFPB officials, consistent with statutory requirements for CFPB rulemakings, also said alternatives that CFPB presents for a panel discussion and in a proposed rule are those they deemed significant and consistent with applicable statutes.

Figure: Overview of SBREFA Panel Process

GAO interviewed 57 of the 69 small entity representatives who participated in the four SBREFA panels GAO reviewed and found they generally believed the process was useful but also that it could be improved. More than three-quarters stated the materials CFPB provided helped prepare them to provide constructive input, and two-thirds stated their industry was represented on the panels. However, two-thirds stated not enough time was allotted to discuss at least one of the topics on the panel agenda and a third suggested more time or additional meetings would improve the process. While 36 of 57 stated CFPB at least partially considered their comments in its rulemakings, most representatives expressed disagreement with CFPB's final rules for reasons such as increased cost of compliance. Specifically, 7 of 57 were satisfied with CFPB's final rules. CFPB officials noted that the rules for which GAO reviewed SBREFA panels were based on statutory requirements in the Dodd-Frank Act. In its rulemaking process, CFPB is to consider input from multiple sources and makes judgments deemed necessary to accomplish the stated objectives of applicable statutes.

Why GAO Did This Study

The Regulatory Flexibility Act, which was amended by the Dodd-Frank Act, requires CFPB to convene Small Business Review Panels (also known as SBREFA panels) for rulemaking efforts that are expected to have a significant economic impact on a substantial number of small entities. These panels are intended to seek direct input early in the rulemaking process from small entities (which can include small businesses, small not-for-profit organizations, and small governmental jurisdictions) that would be impacted by CFPB's rulemakings. This report addresses the extent to which CFPB solicited, considered, and incorporated such inputs into its rulemakings, and the views of small entity representatives on CFPB's rulemaking process.

GAO analyzed and reviewed CFPB's rulemaking processes and documents and conducted semi-structured interviews with 57 of the 69 participants on four panels who agreed to be interviewed. The scope was limited to the four SBREFA panels that had associated final rules as of April 2016.

GAO does not make any recommendations in this report. CFPB generally agreed with our findings.

For more information, contact William Shear at (202) 512-8678 or shearw@gao.gov.