Small Employer Health Tax Credit: Limited Use Continues Due to Multiple Reasons

Highlights

What GAO Found

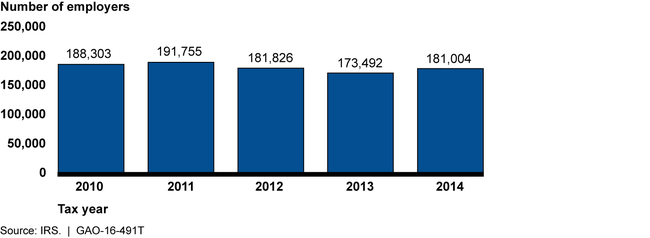

Claims of the small employer health tax credit have continued to be lower than thought eligible by government agency and small business group estimates, limiting the effect of the credit on expanding health insurance coverage through small employers. In 2014, about 181,000 employers claimed the credit, down somewhat from 2010 (see figure). These numbers are relatively low compared to the number of employers eligible for the credit. In 2012, GAO reported that selected estimates of the number of employers eligible ranged from about 1.4 million to 4 million. In 2010, claims totaled $468 million compared to initial estimates of $2 billion by the Congressional Budget Office and the Joint Committee on Taxation. Actual claims for the credit in 2013 and 2014 increased slightly to about $511 million and $541 million, respectively.

Number of Employers That Claimed Small Employer Health Tax Credit

The small employer health tax credit has not been widely claimed for a variety of reasons, as GAO reported in May 2012. The maximum amount of the credit does not appear to be a large enough incentive for employers to offer or maintain insurance. Also, few small employers qualify for the maximum credit amount. For those employers who do claim the credit, the credit amount “phases out” to zero as employers employ up to 25 full time equivalent (FTE) employees at higher wages. The amount of the credit is also limited if premiums paid by an employer are more than the average premiums for the small group market in the employer's state. Furthermore, the credit can only be claimed for two consecutive years after 2013. GAO also found that the cost and complexity involved in claiming the tax credit was significant, deterring small employers from claiming it. Many small businesses have also reported that they were unaware of the credit. Even so, the Internal Revenue Service (IRS) had been taking steps since April 2010 to raise awareness about the credit and reduce the burden on taxpayers by offering tools to help taxpayers determine eligibility for the credit.

Congress and the administration have proposed a number of changes to the credit. These include expanding the size of eligible employers, altering the phase out rules, and allowing the credit to be claimed in more than two consecutive years. Amending the eligibility requirements or increasing the amount of the credit may allow more businesses to claim the credit. However, these changes would increase its cost to the federal government.

Why GAO Did This Study

Many small employers do not offer health insurance. The Small Employer Health Insurance Tax Credit was established as part of the Patient Protection and Affordable Care Act to help eligible small employers—businesses or tax-exempt entities—provide health insurance for employees. The base of the credit is premiums paid or the average premium for an employer's state if premiums paid were higher. In 2016, for small businesses, the credit is 50 percent of the base unless the business had more than 10 FTE employees or paid average annual wages over $25,900.

This statement summarizes and updates GAO's prior work in May 2012, November 2014, and March 2015 on the extent to which the credit is claimed, any reasons that limit claims, and changes to the credit proposed by Congress and the administration. To conduct the updates, GAO reviewed 2013 and 2014 IRS data on credit claims and academic and government studies, and summarized proposed legislation related to the credit.

Recommendations

GAO is not making recommendations in this testimony statement.