Corporate Income Tax: Most Large Profitable U.S. Corporations Paid Tax but Effective Tax Rates Differed Significantly from the Statutory Rate

Highlights

What GAO Found

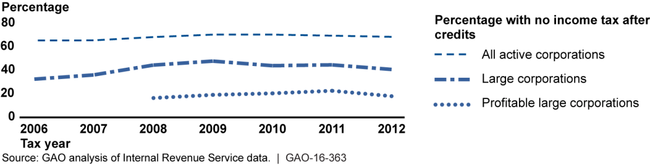

In each year from 2006 to 2012, at least two-thirds of all active corporations had no federal income tax liability. Larger corporations were more likely to owe tax. Among large corporations (generally those with at least $10 million in assets) less than half—42.3 percent—paid no federal income tax in 2012. Of those large corporations whose financial statements reported a profit, 19.5 percent paid no federal income tax that year. Reasons why even profitable corporations may have paid no federal tax in a given year include the use of tax deductions for losses carried forward from prior years and tax incentives, such as depreciation allowances that are more generous in the federal tax code than those allowed for financial accounting purposes. Corporations that did have a federal corporate income tax liability for tax year 2012 owed $267.5 billion.

Percentage of Corporations That Reported No Tax Liability after Tax Credits, Tax Years 2006 to 2012

These reasons also explain why corporate effective tax rates (ETR) can differ substantially from statutory tax rates. ETRs attempt to measure taxes paid as a proportion of economic income, while statutory rates indicate the amount of tax liability (before any credits) relative to taxable income, which is defined by tax law and reflects tax benefits built into the law. The statutory tax rate on net corporate income ranges from 15 to 35 percent, depending on the amount of income earned. For tax years 2008 to 2012, profitable large U.S. corporations paid, on average, U.S. federal income taxes amounting to about 14 percent of the pretax net income that they reported in their financial statements (for those entities included in their tax returns).

When foreign and state and local income taxes are included, the average ETR across all of those years increases to just over 22 percent. GAO also computed ETRs that combine large profitable corporations and those large corporations with current year losses, which pay little if any actual tax. Over tax years 2008 to 2012, all large corporations—profitable and those that reported current year losses—paid 25.9 percent of their pretax net income in U.S. federal income taxes, and 40.1 percent when foreign and state and local taxes are included. Including corporations with losses results in a more comprehensive estimate, but makes the results difficult to interpret because ETR is not meaningful for a corporation in a year in which it has a net loss. GAO could not examine the variation in ETRs across corporations with the aggregated data available, although GAO's prior work suggests that ETRs are likely to vary considerably.

Why GAO Did This Study

Congress and the administration continue to express interest in reforming the U.S. corporate income tax and the rate at which U.S. corporations' income is taxed. Currently, the top statutory corporate income tax rate is 35 percent. GAO's 2013 report on corporate ETRs found that in tax year 2010, whether for all large corporate filers or only profitable ones, the average ETRs were significantly below the statutory rate.

To provide an update, GAO was asked to assess the extent to which U.S. corporations pay federal income tax and the percentage that had no federal income tax liability. In this report, GAO estimates (1) the percentage of all and large corporations that had no federal income tax liability and (2) average ETRs based on financial statement reporting and tax reporting. To conduct this work, GAO reviewed economic literature, analyzed IRS data for tax years 2006 to 2012 (the most recent data available), including the financial and tax information that large corporations report on Schedule M-3, and interviewed Internal Revenue Service (IRS) officials and subject matter experts.

Recommendations

GAO does not make recommendations in this report. GAO provided a draft of this report to IRS for review and comment. IRS provided technical comments, which were incorporated, as appropriate.