Terrorism Insurance: Treasury Needs to Collect and Analyze Data to Better Understand Fiscal Exposure and Clarify Guidance

Highlights

What GAO Found

Comprehensive data on the terrorism insurance market are not readily available and Department of the Treasury (Treasury) analysis to better understand federal fiscal exposure under various scenarios of terrorist attacks has been limited. Treasury compiled some market data from industry sources, but the data are not comprehensive. Federal internal control standards state that agencies should obtain needed data and analyze risks, and industry best practices indicate that analysis of the location and amount of coverage helps understand financial risks. However, without more data and analysis, Treasury lacks the information needed to help ensure the goals of the Terrorism Risk Insurance Act (TRIA) of ensuring the availability and affordability of terrorism risk insurance and addressing market disruptions are being met and to better understand potential federal spending under different scenarios.

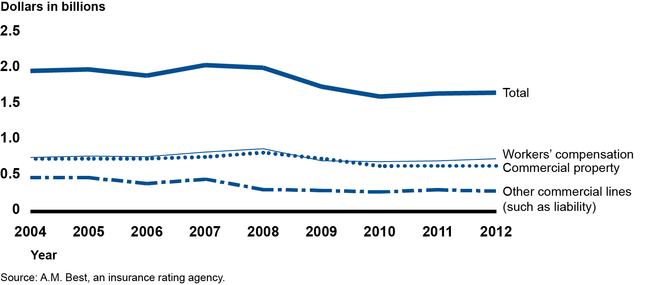

Available data show that terrorism insurance premiums and other market indicators are stable. For example, estimated terrorism insurance premiums have been relatively constant since 2010 (see figure). Insurers told GAO that, in 2012, terrorism insurance premiums made up on average less than 2 percent of commercial property and casualty premiums. According to industry participants, prices for terrorism coverage have declined, the percentage of businesses buying coverage seems to have leveled recently, and insurers' ability to provide it has remained constant.

Estimated Terrorism Insurance Premiums by Total and Selected Insurance Lines, 2004-2012

Insurers and other industry participants cited concerns about the availability and price of terrorism coverage if TRIA expired or was changed substantially, but some changes could reduce federal fiscal exposure. Some insurers GAO contacted said they would stop covering terrorism if TRIA expired. Changes such as increasing the deductible or threshold for required recoupment of the government's share of losses through surcharges on all commercial policyholders could reduce federal fiscal exposure. Most insurers GAO contacted expressed concerns about solvency and ability to provide coverage if their deductible or share of losses increased. Insurers were less concerned about increases to the thresholds for government coverage to begin or to the required recoupment of the government's share of losses.

Why GAO Did This Study

Congress passed TRIA in 2002 to help ensure the availability and affordability of terrorism insurance for commercial property and casualty policyholders after the September 11, 2001, terrorist attacks. TRIA was amended and extended twice and currently will expire at the end of 2014. Under TRIA, Treasury administers a program in which the federal government and private sector share losses on commercial property and casualty policies resulting from a terrorist attack. Because the federal government will cover a portion of insured losses, the program creates fiscal exposures for the government. GAO was asked to review TRIA.

This report evaluates (1) the extent of available data on terrorism insurance and Treasury's efforts in determining federal exposure, (2) changes in the terrorism insurance market since 2002, and (3) potential impacts of selected changes to TRIA. To address these objectives, GAO analyzed insurance data, information from 15 insurers selected primarily based on size of insurer, interviewed Treasury staff and industry participants, updated prior work, and developed examples to illustrate potential fiscal exposure under TRIA.

Recommendations

Treasury should collect and analyze data on the terrorism insurance market to assess the market, estimate fiscal exposure under different scenarios, and analyze the impacts of changing program parameters. Treasury agreed with these recommendations.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Department of the Treasury | The Secretary of the Treasury should collect the data needed to analyze the terrorism insurance market. Types of data may include terrorism coverage by line of insurance and terrorism insurance premiums earned. In taking this action, Treasury should determine whether any additional authority is needed and, if so, work with Congress to ensure it has the authority needed to carry out this action. |

The Terrorism Risk Insurance Program Reauthorization Act of 2015 required Treasury to collect certain data on terrorism insurance. In December 2016, Treasury issued a final rule implementing changes to the program required by the reauthorization act, including a requirement for annual data reporting. Treasury also issued proposed data collection templates for public comment. The information insurers are required to report includes the lines of property and casualty insurance subject to the program, the premiums earned for terrorism risk insurance within those lines, the geographical location of exposures covered, the pricing of terrorism risk insurance, the take-up rate for terrorism risk insurance, and the amount of private reinsurance obtained by participating insurers. According to the final rule, insurers are required to report these data by May 15th each year. Treasury held a voluntary data call in 2016, and insurers are required to submit data annually beginning May 15, 2017.

|

| Department of the Treasury | The Secretary of the Treasury should periodically assess data collected related to terrorism insurance, including analyzing differences in terrorism insurance by company size, geography, or industry sector; conducting hypothetical illustrative examples to help estimate the potential magnitude of fiscal exposure; and analyzing how changing program parameters may impact the market and fiscal exposure. |

In June 2016, Treasury released a report on the effectiveness of the Terrorism Risk Insurance Program. In this report, Treasury analyzed data the agency collected from insurers on pricing, take-up rates, exposure, and reinsurance. For example, the report includes analyses of differences in terrorism insurance pricing and take-up rates by geography. In addition, the report includes analyses of the exposure of insurers and the program to hypothetical terrorist event scenarios. Treasury has published a notice of proposed rulemaking that would require insurers to submit annual data on terrorism insurance beginning in calendar year 2017. As Treasury continues to collect data, it will continue to evaluate issues of availability, affordability, and impacts of the program on insurers of different sizes, and to analyze any identifiable trends in the data.

|

| Department of the Treasury | The Secretary of the Treasury should gather additional information needed from the insurance industry related to how cyber terrorism is defined and used in policies, and clarify whether losses that may result from cyber terrorism are covered under TRIA--clarification could be made through an interpretative letter or revisions to program regulations, some combination or any other vehicle that Treasury deems appropriate. |

In December 2016, Treasury issued a notice of guidance in the Federal Register clarifying how cyber liability insurance would be treated under the Terrorism Risk Insurance Program. The guidance acknowledges the uncertainty in the market regarding whether such risk would be covered under the program due to the evolving nature of insurance products covering cyber risk. Therefore, the guidance clarifies that policies written in lines of insurance that are eligible for the Terrorism Risk Insurance Program and which contain a "cyber risk component" or do not exclude losses arising from a cyber event are subject to the provisions of the program. In addition, the guidance states that policies identified under a new sub-category of "Cyber Liability" insurance are considered property and casualty insurance under the program. Thus, such policies are eligible for federal reimbursement in the event of a certified terrorist attack provided that the insurer has complied with other program requirements and regulations.

|