Information Technology: IRS Needs to Improve the Reliability and Transparency of Reported Investment Information

Highlights

What GAO Found

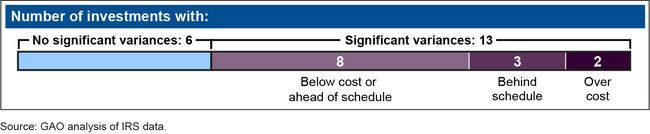

According to the Internal Revenue Service (IRS), 6 of its19 major information technology (IT) investments were within 10 percent of cost and schedule estimates during fiscal year 2013. The remaining 13 were reported as having significant cost and schedule variances for at least 1 month of the year. Specifically, IRS reported 8 investments as being below cost or ahead of schedule; 3 as behind schedule; and 2 as over cost (see figure). IRS reported a range of reasons for these variances, including cost savings from contract negotiations and scope deferrals for those below cost or ahead of schedule, and procurement delays for those behind schedule. It is important to note that the reported monthly cost and schedule variances are for the fiscal year only. IRS's reporting would be more meaningful if it were supplemented with cumulative cost and schedule variances for the investments or investment segments, consistent with the Office of Management and Budget's guidance for measuring progress towards meeting investment goals.

Summary of Investments with Significant Variances

The reported variances for six investments reviewed were not always reliable because the projected and actual cost and schedule amounts on which they depend were not consistently updated in accordance with OMB and Treasury reporting requirements. Specifically, projected amounts were not always updated on a monthly basis for in-process (i.e., ongoing) activities for a range of reasons; and actual information was not consistently updated for completed activities within the 60-day time frame required by Treasury guidance. Addressing these issues would help IRS improve the reliability of reported information and provide Congress with a more accurate report of the agency's performance in meeting cost and schedule goals.

IRS is currently not working on developing a quantitative measure of scope (i.e., functionality) as GAO recommended in June 2012 and does not plan on doing so, because it believes it is difficult to develop a single measure that would allow it to measure progress in delivering scope for the range of IRS's investments. However, the agency could develop measures using different methods as appropriate. In addition, IRS has started to include scope performance (in the functional performance section) in its quarterly reporting to Congress. However, this information does not include a quantitative measure of performance. In addition, it does not show how delivered scope compares to what was planned. Providing transparency into progress in delivering scope by reporting qualitatively in the congressional reports until a quantitative measure is developed would help IRS provide Congress a complete picture of the agency's performance in managing its major investments.

Why GAO Did This Study

IRS relies extensively on IT systems to annually collect more than $2 trillion in taxes, distribute more than $300 billion in refunds, and carry out its mission of providing service to America's taxpayers in meeting their tax obligations. For fiscal year 2014, the agency's budget request is $2.6 billion for IT. Given the size and significance of IRS's IT investments, and the challenges inherent in successfully delivering these complex IT systems, it is important that Congress be provided reliable cost, schedule, and scope information to assist with its oversight responsibilities.

Accordingly, GAO's objectives were to (1) summarize the reported cost and schedule performance for IRS's major IT investments and assess the reporting of the performance information (2) for selected investments, evaluate the reliability of reported cost and schedule variances; and (3) determine IRS's progress in implementing a quantitative measure of functionality delivered for projects. To address these objectives, GAO reviewed documentation, including monthly cost and schedule variance reports, and interviewed staff, including those from selected investments which are critical to IRS's mission.

Recommendations

GAO is making recommendations for IRS to report more comprehensive and reliable cost and schedule information and improve the transparency of reported scope information for its major investments. IRS agreed with GAO's recommendations and stated it believed it had addressed one of them. GAO continues to believe further actions are needed.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Internal Revenue Service | To improve the reliability of reported cost and schedule variance information for major investments, the Commissioner of IRS should direct the Chief Technology Officer to report cumulative investment and investment segment cost and schedule information in the quarterly reports to Congress, consistent with the Office of Management and Budget (OMB) requirements for measuring progress towards meeting goals. |

In response to our recommendation, the Internal Revenue Service (IRS) included cumulative cost and schedule information for the Return Review Program in the fourth quarterly report of fiscal year 2016. In addition, IRS added cumulative cost and schedule information for the Customer Account Data Engine 2 investment in the third quarterly report for fiscal year 2016. Starting with the first quarterly report of fiscal year 2017, IRS began including cumulative cost and schedule information for all of the investments in development that it reported on.

|

| Internal Revenue Service | To improve the reliability of reported cost and schedule variance information for major investments, the Commissioner of IRS should direct the Chief Technology Officer to ensure that projected cost and schedule variances for in-process activities are updated monthly, for the six investments for which we reviewed monthly updates, consistent with OMB and Treasury reporting requirements, by ensuring investment staff have a consistent understanding of the information to be included in monthly reports. |

In fiscal year 2016, IRS began using the Investment Performance Tool to track the performance of IT investments in development. The tool tracks the amount of planned scope (i.e., functionality) that was delivered during a reporting period and, as such, is expected to provide reliable measures of cost and schedule performance for ongoing activities, which was the intent of our recommendation. In addition, in October 2015, IRS issued guidance for its Investment Performance Tool to ensure investment staff has a consistent understanding of the information to be included in performance reports. We reviewed IRS's use of the tool as part of a review of the agency's major IT systems (see GAO-18-298 issued in June 2018) and, in September 2018, confirmed IRS's continued use of the tool and ability to generate monthly reports for 4 of the 5 investments for which IRS was reporting to Congress as of the third quarter of fiscal year 2018. (The four investments are Customer Account Date Engine 2, ECM, Return Review Program, and WebApps.) The fifth investment-Web Infrastructure--is no longer in development and is consequently not being tracked using the Investment Performance Tool. In September 2018, IRS told us that the tool is available for use for major investments in development and it is up to each owning organization to assess the value and applicability of the tool for their investments. We believe IRS's actions fully address the recommendation.

|

| Internal Revenue Service | To improve the reliability of reported cost and schedule variance information for major investments, until a quantitative measure of scope is developed, the Commissioner of IRS should direct the Chief Technology Officer to qualitatively report on how delivered scope compares to what was planned in its quarterly reports to Congress, for the seven investments for which we reviewed scope reporting. |

Starting with the first quarterly report of fiscal year 2015 to Congress, IRS began including the release plans listing project summaries and timeframes for each of the investments it was reporting on. The agency also provided a list of accomplishments for the past quarter and expected milestones for the upcoming quarter which described how delivered functionality compared to the expected functionality. As of the third quarter of fiscal year 2017, IRS was still continuing to include this information in its quarterly reports to Congress.

|