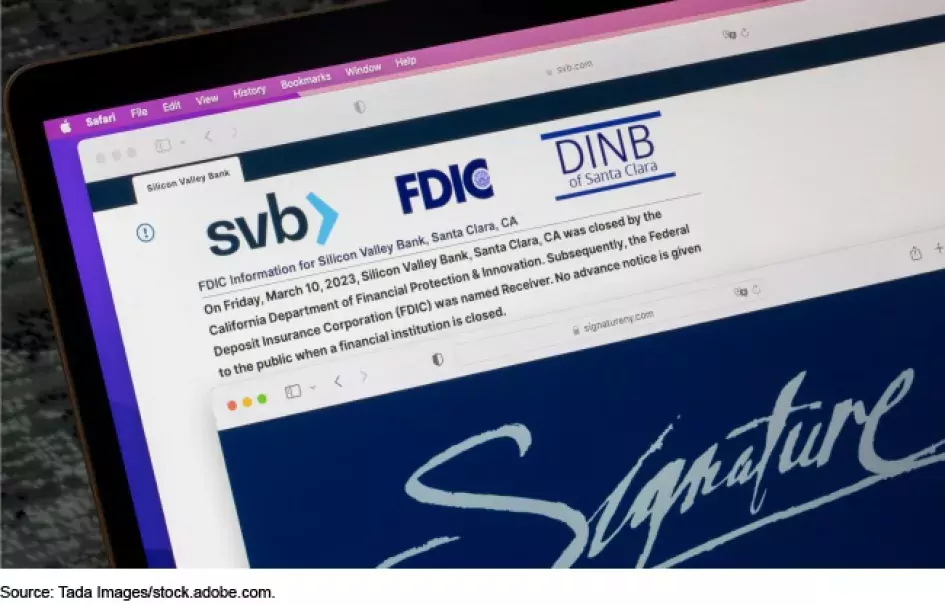

March 2023 Bank Failures—Risky Business Strategies Raise Questions About Federal Oversight

When Silicon Valley Bank and Signature Bank failed in March, they suffered two of the largest bank failures in U.S. history.

Today, we released our first report on these bank failures. While we continue to look into a number of related issues, today’s WatchBlog post looks at our observations about why these two banks failed, and what federal regulators did before it happened.

Image

What went wrong with the banks?

Risky business strategies and weak risk management contributed to the failures of Silicon Valley Bank (the 16th largest U.S. bank by asset value) and Signature Bank (the 29th largest).

Risky business: Both banks grew rapidly over a relatively short period and relied on less stable funding to support their rapid growth.

Silicon Valley Bank (SVB) primarily served entrepreneurs in technology, health care, and private equity. It added products and services to maintain clients as they matured from their startup phases, and expanded into banking and financing for venture capital. From December 2018 to December 2022, SVB’s total assets more than tripled from $56 billion to $209 billion (an increase of 198%).

Signature Bank focused primarily on multifamily and other commercial real estate banking. Then, it launched services to the private equity industry, including financing for venture capital. It also expanded to the digital assets industry (e.g., cryptocurrency). From December 2018 to December 2022, Signature Bank’s total assets more than doubled from $47 billion to $110 billion (an increase of 134%).

Growth of Assets at the Two Failed Banks vs 19 Peer Banks

Image

Rapid growth can be an indicator of risk in a bank’s business. Regulators like the Federal Reserve System (the Fed) and the Federal Deposit Insurance Corporation (FDIC) were concerned about whether the banks’ risk management practices maintained pace with their rapid growth. Funding rapid growth with uninsured deposits—deposits that exceed the $250,000 FDIC insurance limit—increased risks to the banks. Customers with uninsured deposits may be more likely to withdraw their funds, or “run” on the bank, during times of economic uncertainty.

From 2018-2022, SVB’s uninsured deposits ranged from 70-80% of its total assets, and Signature Bank’s uninsured deposits ranged from 63-82% of total assets. By comparison, banks of similar size had median uninsured deposits ranging from 31-41%.

Uninsured Deposits as a Percentage of Total Assets at the Two Failed Banks vs 19 Peer Banks

Image

Risk Management: The ineffective risk management may have made the banks more vulnerable to external factors—and good-old-fashioned bank runs.

- Rising interest rates: As interest rates rose, SVB’s lower-yielding securities (like bonds) lost value. When SVB’s customers with large sums of uninsured deposits started withdrawing their money, SVB had to sell some of those securities to cover deposits—realizing those losses. Just before it failed, on March 8, SVB announced the sale of $21 billion in securities, resulting in a loss of $1.8 billion.

- Digital asset market volatility: Signature Bank had conducted business with the digital assets industry, which became increasingly volatile throughout 2022. Signature Bank was starting to decrease its exposure to the industry when customers started withdrawing their money after SVB’s collapse. Signature Bank’s balance sheet cash holdings went from $31 billion in 2021 to $6 billion in 2022.

What went wrong with federal oversight and response?

We’ve looked at bank failures before, notably during the 2007-2009 financial crisis—which saw the largest bank failure in U.S. history (Washington Mutual). Both then and now, we’ve found that although regulators often identified risky practices early, the regulators’ corrective actions either didn’t work or came too late to prevent failure.

For example, we found that the Fed voiced concerns about how SVB was managing liquidity—cash and assets that can be easily turned into cash to meet outflows—in August 2021, while still providing the bank with an overall “satisfactory” rating. By late June 2022, the Fed downgraded SVB’s rating, and in August 2022, the Fed issued a supervisory letter informing the bank of its intent to initiate enforcement action focusing on correcting the management and liquidity issues that ultimately resulted in the bank’s failure. But efforts to take the enforcement action were not finalized to allow regulators to complete additional examinations of the bank.

Signature Bank also received a “satisfactory” rating between December 2018 and December 2021, while FDIC took numerous supervisory actions to address liquidity and management risks at the bank. FDIC had not completed its 2022 examination documents for Signature Bank at the time of its failure in March 2023. FDIC staff told us they were considering escalating supervisory actions in 2022. But these actions wouldn’t have taken effect until the second quarter of 2023. On March 11, the day before Signature Bank was closed, FDIC downgraded the bank’s rating and notified the bank of its intent to pursue an enforcement action.

What’s next for GAO’s work?

This is just our first report with preliminary findings about what caused these two banks to fail and the federal response before and after. We plan to continue investigating this issue, including a mandate from Congress to further review the federal agencies’ use of their emergency authority.

- Comments on GAO’s WatchBlog? Contact blog@gao.gov.

GAO Contacts

Image

Related Products

GAO's mission is to provide Congress with fact-based, nonpartisan information that can help improve federal government performance and ensure accountability for the benefit of the American people. GAO launched its WatchBlog in January, 2014, as part of its continuing effort to reach its audiences—Congress and the American people—where they are currently looking for information.

The blog format allows GAO to provide a little more context about its work than it can offer on its other social media platforms. Posts will tie GAO work to current events and the news; show how GAO’s work is affecting agencies or legislation; highlight reports, testimonies, and issue areas where GAO does work; and provide information about GAO itself, among other things.

Please send any feedback on GAO's WatchBlog to blog@gao.gov.