Affordable Ways to Save

For many of us, U.S. savings bonds bring back memories of birthday or graduation gifts from grandparents or aunts or uncles. But U.S. savings bonds have also provided Americans with a safe, affordable way to save and invest.

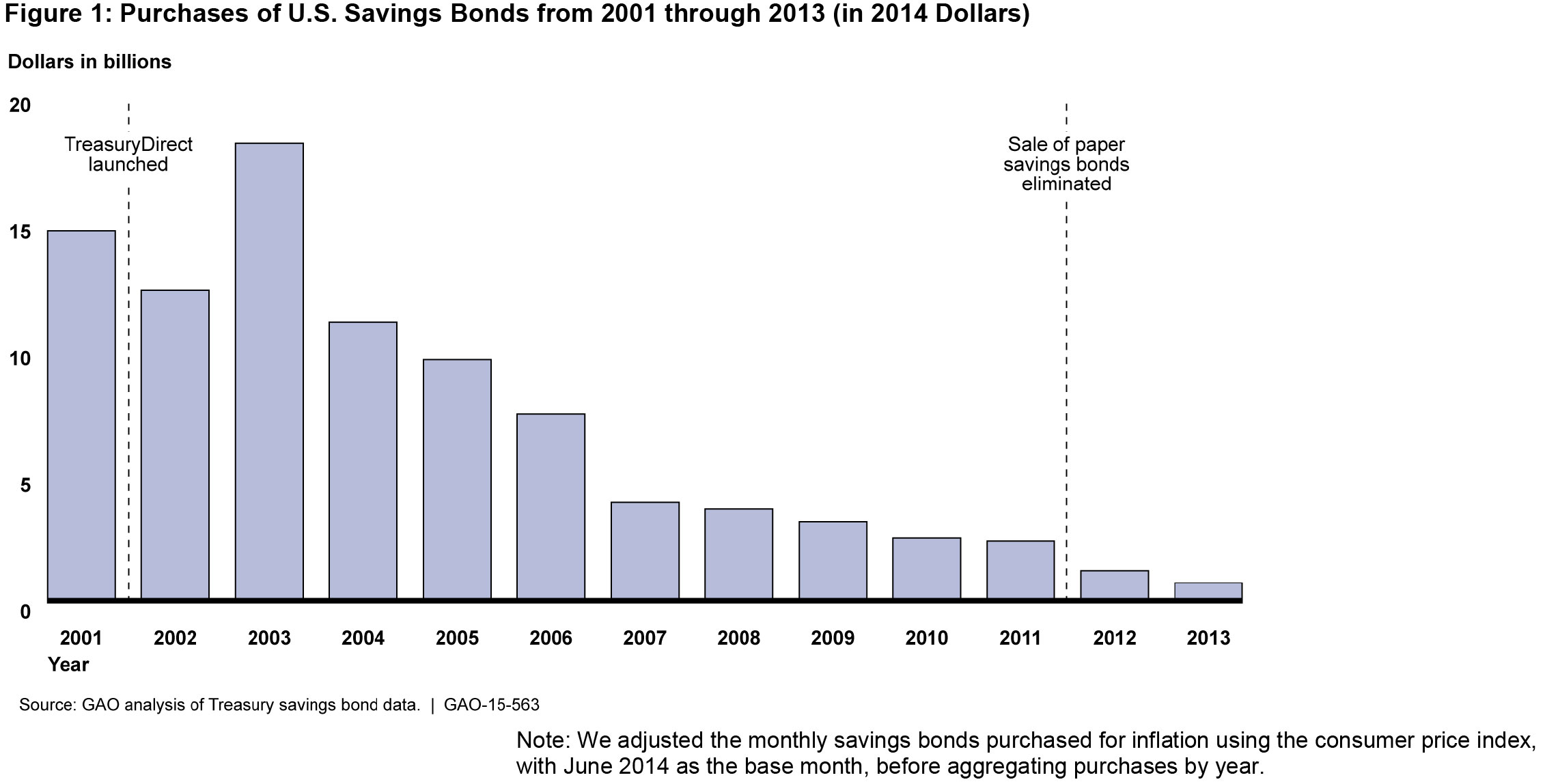

We recently reported on changes to the ways Americans buy savings bonds and on how the government is helping to promote savings. For America Saves Week, today’s WatchBlog shares what we found.

Savings bonds go paperless

Who knew? The U.S. Treasury Department stopped selling paper savings bonds through banks in 2012 after a long-term decline in savings bond purchases. Now, the 2 ways to buy U.S. savings bonds are

- Online. If you have internet access and a bank account, you can use Treasury’s online system, TreasuryDirect®, to buy, manage, and redeem savings bonds at any time.

- With your tax refund. Since 2010, U.S. tax filers may use their tax refund to buy paper savings bonds through IRS’s Tax Time Savings Bond Program. About 142,000 tax filers bought more than $72 million in paper savings bonds through the program between 2010 and 2013.

Although the Tax Time program was scheduled to expire after the 2015 tax season, Treasury extended it another year, partly because participation rates indicated that the program was providing benefits.

However, Treasury generally hasn’t considered the program’s costs. We recommended that Treasury consider the program’s benefits and costs in its future decisions about whether to extend the program.

(Excerpted from GAO-15-563)

Help for low-income savers

Whether paper or online, saving money can be tough—especially for those without a lot to save. In 2013, the bottom fifth of income earners had a median income of $14,200 and a median of $550 in savings. That means that half had more than $550—and half had less.

In light of this low level of savings, federal, state, and local agencies, as well as nonprofits, have developed programs to help low-income families save and build assets. These programs provide financial literacy and education services, and promote both short- and long-term financial goals, such as saving for an emergency as well as retirement. For example,

- The Federal Deposit Insurance Corporation’s Money Smart financial education program is designed to help consumers and entrepreneurs, especially those with low and moderate incomes, enhance their financial skills and help create positive banking relationships;

- FDIC also launched pilot programs to encourage.banks to help low-income earners set up bank accounts and young people to start saving early;

- Treasury’s myRA® promotes retirement savings for people without access to employer-sponsored retirement plans;

- The departments of Health and Human Services and Housing and Urban Development run grant programs for low-income families looking to become financially self-sufficient.

Check out our full report, which provides additional details on these and other programs.

Comments on GAO’s WatchBlog? Contact blog@gao.gov.

GAO Contacts

Image

Related Products

GAO's mission is to provide Congress with fact-based, nonpartisan information that can help improve federal government performance and ensure accountability for the benefit of the American people. GAO launched its WatchBlog in January, 2014, as part of its continuing effort to reach its audiences—Congress and the American people—where they are currently looking for information.

The blog format allows GAO to provide a little more context about its work than it can offer on its other social media platforms. Posts will tie GAO work to current events and the news; show how GAO’s work is affecting agencies or legislation; highlight reports, testimonies, and issue areas where GAO does work; and provide information about GAO itself, among other things.

Please send any feedback on GAO's WatchBlog to blog@gao.gov.