Are Financial Planners Always Working in Your Best Interest?

People frequently use financial planners for help with such things as selecting investments and insurance products, and managing tax and estate planning. Entrusting someone with your money can be risky. What steps can you take to mitigate that risk? We reviewed oversight of financial planners after the financial crisis.

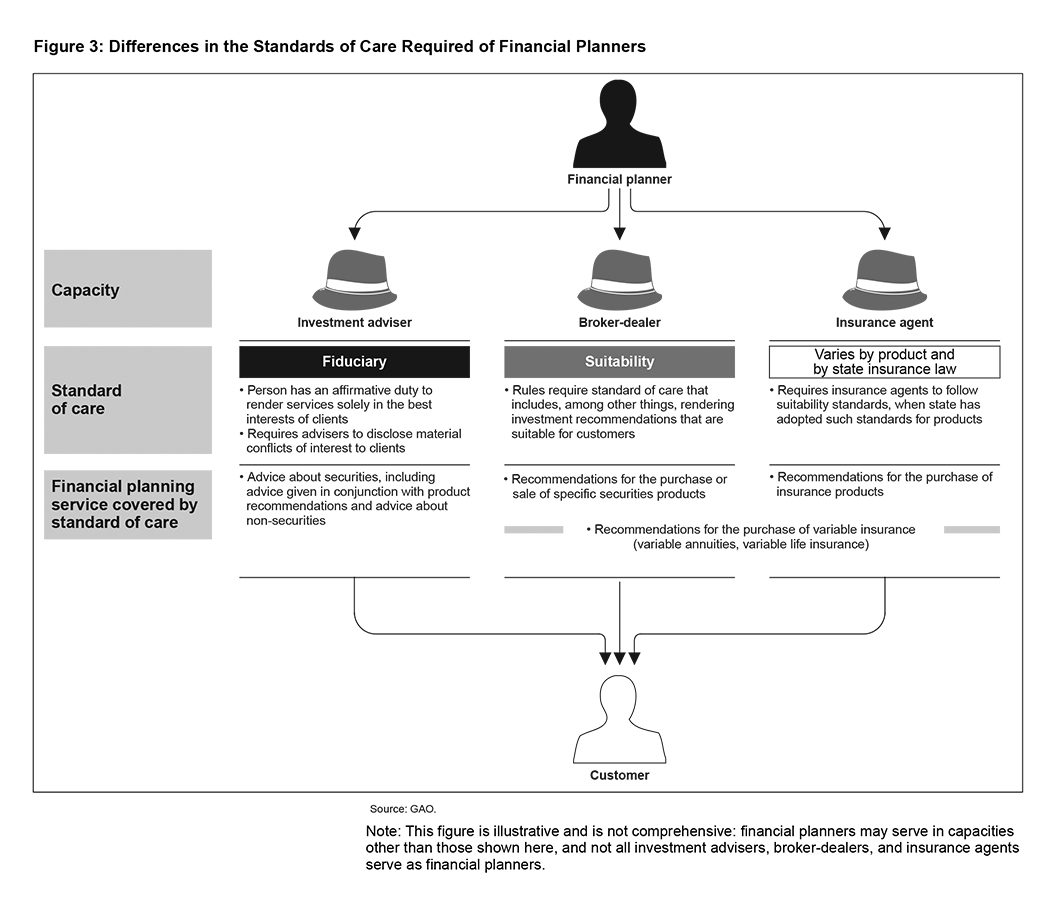

1.Ensure that you understand the standard of care your financial planner is required to give.

There is no specific, direct regulation of "financial planners" per se at the federal or state level, but the standard of care that applies is based on the specific services each planner provides to you. For example, a financial planner serving as an investment adviser is required to put your best interest ahead of his or her own (a “fiduciary standard”), but when serving as a stockbroker or insurance agent, the standards of care may be more lenient. As another example, if a stockbroker receives a commission for selling you a certain investment product, he or she may only be subject to a suitability standard of care, and does not need to disclose the potential conflict of interest to you as long as the product is suitable for you.

Excerpted from GAO-11-235

2. Understand your financial planner’s experience and credentials—titles may not tell the whole story.

Financial planners may adopt a variety of privately conferred professional designations, but regular people may not understand or be able to distinguish among them. These designations range from those with rigorous competency, practice, and ethical standards and enforcement, to those that can be obtained with minimal effort and no ongoing evaluation.

Federal and state regulators recommend that you not rely solely on a title to determine whether a financial professional has the expertise that you need. Instead, you should seek to understand that professional’s experience and credentials.

Find out more in our report CONSUMER FINANCE: Regulatory Coverage Generally Exists for Financial Planners, but Consumer Protection Issues Remain, GAO-11-235, Jan 18, 2011.

Read other GAO reports on topics related to consumer financial planning, including:

- 401(k) PLANS: Other Countries' Experiences Offer Lessons in Policies and Oversight of Spend-down Options, GAO-14-9, Nov. 20, 2013

- RETIREMENT SECURITY: Annuities with Guaranteed Lifetime Withdrawals Have Both Benefits and Risks, but Regulation Varies across States, GAO-13-75, Dec. 10, 2012

- HIGHER EDUCATION: A Small Percentage of Families Save in 529 Plans, GAO-13-64, Dec. 12, 2012

Also check out our related blog post on retirement planning in the new year.

Comments on GAO’s WatchBlog? Contact blog@gao.gov.

GAO Contacts

Image