Federal Reserve Lending Programs: Main Street Program Continues to Hold Outstanding Loans Beyond Initial Maturity Dates

Fast Facts

The Federal Reserve authorized 13 emergency lending programs in response to COVID-19, including the Main Street Lending Program. This program made 1,830 loans—a total of $16.6 billion—to small and midsized businesses and nonprofits. These loans were supposed to be paid back by early January 2026.

Of the 1,830 loans made through this program:

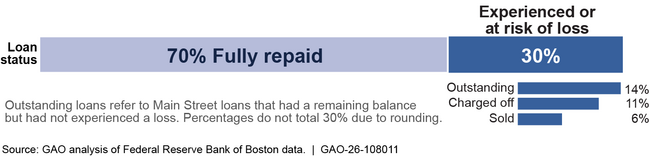

70% were fully repaid

16% either resulted in losses or were sold to lenders at a loss

The rest, worth $2 billion in total, remained outstanding. These borrowers were unable to make their final payments—generally due to the timing of payments and increases in variable interest rates.

One person's hands hold a calculator, while another's hold a bill and a pen. A notice of a past due payment is on the table next to them.

Highlights

What GAO Found

In response to the COVID-19 pandemic, the Board of Governors of the Federal Reserve System authorized 13 emergency lending programs—with lending facilities to implement the programs—to ensure the flow of credit across the economy. To improve oversight of these programs, the Federal Reserve evaluated program internal processes and controls and identified 20 opportunities to enhance internal controls. GAO found that Federal Reserve Banks, which manage the facilities, have implemented processes to address all 20 opportunities. In addition, the Federal Reserve has completed its review of all 20 opportunities. GAO also found that the Federal Reserve’s plans for ongoing monitoring of the facilities are generally aligned with federal internal control standards.

The five facilities under the Main Street Lending Program targeted small and midsize businesses and nonprofits. Of the 1,830 loans made through this program, 70 percent (1,277 loans) were fully repaid as of January 5, 2026, while 30 percent had experienced or were at risk of loss. Nearly 14 percent (251 loans) remained outstanding even though they should have closed by January 5, 2026. The other 16 percent resulted in losses to the program—$1.3 billion in charged-off loan amounts and $1.4 billion in authorized loan amounts sold back to their lenders at a net loss.

Main Street Lending Program Loan Status as of January 5, 2026

Loans to larger borrowers and those made by larger lenders had higher payoff rates and lower default rates. For example, loans to the largest businesses in the program (those with more than $42.1 million in revenue) had the highest percentage of repaid loans and the lowest percentage of impaired loans by number. Additionally, about 87 percent of loans made by the largest lenders (with revenue greater than $250 billion at program intake) were fully repaid, outperforming loans made by lenders of other sizes. Loan outcomes also varied by sector.

About 70 percent of borrowers with loans outstanding through their scheduled maturity date were unable to make the loan’s final balloon payment (remaining principal) on time, leaving nearly $2 billion in authorized loan amounts at risk of non-repayment. Elevated interest rates through the duration of the program and the timing of principal payment milestones generally were associated with a decreased likelihood of full loan repayment and increased likelihood of loan impairment. The Federal Reserve Bank of Boston has approved some loan modifications, and officials explained that they will continue to provide borrowers with the opportunity to modify their loans and make payments toward their remaining balance.

Why GAO Did This Study

As of January 2026, three of the Federal Reserve’s emergency lending facilities, all part of the Main Street Lending Program, continued to hold outstanding loans. As of that date, these facilities had approximately $672 million in outstanding loans. The three facilities were among the nine that received funds appropriated through the CARES Act (section 4003). The Federal Reserve plans to monitor and report on the status of the facilities until they no longer hold outstanding assets or loans.

The CARES Act includes a provision for GAO to annually report on section 4003 loans, loan guarantees, and investments. This report examines (1) the Federal Reserve’s oversight and monitoring of the CARES Act facilities and (2) the status and performance of Main Street Lending Program loans, including factors associated with losses.

GAO conducted loan-level analysis of Main Street Lending Program loan performance covering July 2020 through January 2026, reviewed Federal Reserve documentation, and interviewed Federal Reserve officials.

For more information, contact Michael E. Clements at ClementsM@gao.gov.