Small Business Administration: Targeted Outreach about Disaster Assistance Could Benefit Rural Communities

Fast Facts

This Q&A report explores the Small Business Administration's Disaster Loan Program, which helps businesses, homeowners, renters, and nonprofits in urban and rural communities recover after a disaster. But some rural communities may not know about the assistance or how to get it due to specific challenges in those areas, such as intermittent cellular or internet service.

SBA has new outreach efforts—such as portable centers that can be set up in hard-to-reach areas, staffed with people to help. But none of these efforts specifically target rural communities.

Our recommendation could help SBA address rural communities' unique needs.

Tornado damage in Mayfield, Kentucky in December 2021

Highlights

What GAO Found

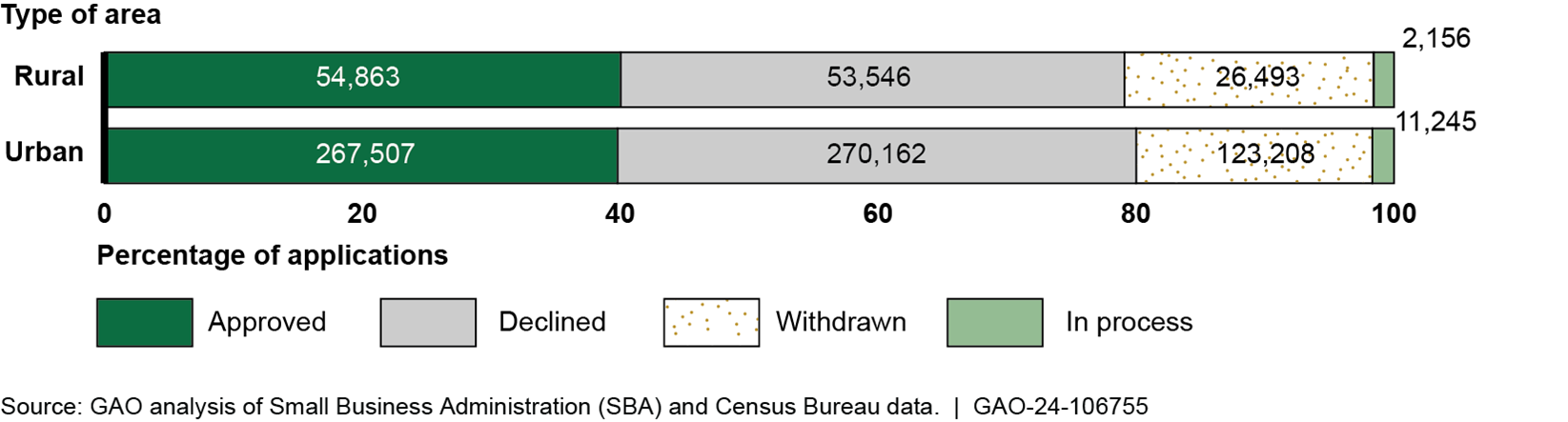

The Small Business Administration's (SBA) Disaster Loan Program is available to rural and urban communities to cover qualified losses after a declared disaster. Disaster loans are intended to help homeowners, renters, businesses, and nonprofits repair, rebuild, and recover from physical and economic losses. For fiscal years 2017–2022, applications for disaster loans from rural and urban areas were approved and declined at comparable rates. Across both types of areas, SBA approved about 40 percent and declined about 40 percent of applications that met minimum qualifications for acceptance. The remaining applications were withdrawn (18.5 percent) or were still being reviewed by SBA as of June 2023 (1.7 percent).

Outcomes of SBA Disaster Loan Applications SBA Accepted by Geographic Area, Fiscal Years 2017–2022, as of June 2023

Note: This analysis includes applications that met SBA’s minimum acceptance qualifications and excludes 20,882 applications that were duplicates or could not be classified as rural or urban.

GAO found that rural communities may have characteristics that can make recovering from a disaster difficult. For instance, they are more likely to have limited telecommunication services (broadband and cellular) because of geographic barriers, such as mountains, or limited demand due to smaller and sparser populations. A lack of reliable communications can hamper outreach to disaster survivors and can make it harder for survivors to apply for disaster assistance. Also, rural communities often do not have the capacity and resources to support recovery activities. Stakeholders also identified challenges to obtaining assistance from SBA. For example, stakeholders noted that rural communities may not be aware of SBA disaster assistance and may not know that SBA aids homeowners as well as businesses.

SBA has introduced new outreach approaches in recent years, such as portable outreach centers that can be established after a disaster in hard-to-reach areas, including rural communities. However, SBA's outreach policies and procedures do not distinguish between rural and urban communities, and SBA does not tailor its outreach to address the specific needs of rural communities. Developing outreach plans with specific methods to address challenges rural communities face after disasters could help improve their access to SBA's Disaster Loan Program.

Why GAO Did This Study

GAO previously reported that the number and cost of weather and climate disasters, such as tornadoes and wildfires, are increasing in the United States. The Disaster Assistance for Rural Communities Act enabled the SBA Administrator to declare disasters in rural areas if certain conditions are met and included a provision for GAO to examine the unique challenges rural areas face when seeking disaster assistance from SBA. This report examines disaster loan trends in rural and urban areas for fiscal years 2017–2022, challenges rural communities may face after disasters, and SBA's actions that may address these challenges.

GAO analyzed and geocoded SBA disaster loan application data for fiscal years 2017–2022 to show trends for approved, accepted, and declined loan applications for rural and urban areas. GAO also interviewed officials from SBA, four regional nonprofit organizations, and 18 state and local entities from three site visits. GAO further reviewed literature and key agency documents related to outreach, marketing, equity, and implementation of the new rural disaster declaration.

Recommendations

GAO recommends that SBA distinguish between rural and urban communities in its outreach and marketing plan and incorporate actions to mitigate challenges rural communities face in accessing the Disaster Loan Program.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Small Business Administration | The SBA Administrator should ensure that the Associate Administrator of the Office of Disaster Recovery and Resilience distinguishes between rural and urban communities in SBA's outreach and marketing plan and incorporates actions to mitigate challenges encountered by rural communities in accessing the Disaster Loan Program. (Recommendation 1) |

In December 2024, SBA provided GAO with SBA's Outreach and Engagement Framework (a power point slide presentation) and a numbered memo (#24-13) on Local Jurisdiction Outreach. Both documents contain specific instructions for identifying rural and underserved communities including specific state, local, and community service providers that SBA should coordinate with. While we recognize that these efforts are moving SBA in the right direction, SBA noted that it will replace the Framework with an Outreach and Engagement Guide. In June 2025, SBA told us that the Outreach and Engagement Guide is a tactical document that will provide direction to field staff. SBA also told us that it estimates completing this guide by the end of the first quarter of 2026. This recommendation will remain open until the agency provides evidence of its official guidance.

|