Farm Credit System: Policy Considerations for a Potential Grant Program for Socially Disadvantaged Farmers and Ranchers

Fast Facts

Minorities and women may have trouble getting loans to buy and run farms. According to lending industry representatives, these socially disadvantaged farmers and ranchers are more likely to operate smaller, lower-revenue farms; have weaker credit histories; or lack clear title to their agricultural land.

The Farm Credit System provides low-cost credit to farmers and ranchers. Establishing a grant program for socially disadvantaged farmers and ranchers with revenue from the Farm Credit System would entail policy considerations and challenges. For example, such a program could increase borrowing costs and result in less money for new loans.

Highlights

What GAO Found

Establishing a grant program for socially disadvantaged farmers and ranchers within the Farm Credit System (FCS) would involve considerations for policymakers, including

- how the program size and funding approach would affect FCS's mission,

- whether the program would expose FCS to legal challenges, and

- whether the program would duplicate existing federal programs.

The Farm Credit Banks and other stakeholders also identified several potential challenges to establishing such a program. For example, the Banks

- lack experience with overseeing a grant program, and

- do not have the appropriate infrastructure or staff.

Banks could address these issues by following leading grant management practices—such as for staffing and training, oversight, and grant management—that have been developed by GAO and others.

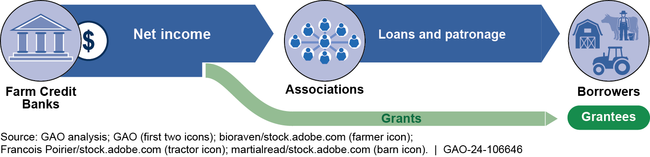

A grant program would involve costs for FCS and its Banks and borrowers, according to stakeholders. The Banks could fund the program by redirecting funds from net income, thereby reducing funds available for loans and patronage (i.e., funds Banks return to borrowers, who are also owners of the system). (See figure.) GAO analyzed FCS data for 2013–2022 and found that Banks would likely have raised effective borrowing costs in at least some years had they been required to fund a program. All four Banks said that a grant program would increase costs for borrowers, reduce FCS's capacity to lend, and diminish FCS's competitiveness with commercial banks as agricultural credit providers. Advocacy groups noted that a grant program could benefit FCS by helping grantees qualify for FCS loans—for example, by buying land to use as collateral.

How Farm Credit Bank Net Income Could Fund a Potential Grant Program

Although Farm Credit Banks' net income, which would potentially fund a grant program, has been relatively stable in recent years, it has been more volatile in the past. More specifically, FCS net income in 1984–1993 was more volatile than in 2013–2022. Further, Farm Credit Administration officials indicated that the most recent decade was unusually strong for the agricultural industry and thus for Farm Credit Bank net income. Farm Credit Banks may face greater income volatility than other financial institutions because of their specialization in agricultural credit. In addition, unique risks in the agricultural industry contribute to uncertainty for Farm Credit Banks' net income.

Why GAO Did This Study

Congress created FCS, a government-sponsored enterprise with a network of banks and associations, to meet the needs of creditworthy agricultural producers. FCS consists of four Farm Credit Banks, which fund associations that make loans to farmers and ranchers. Socially disadvantaged farmers and ranchers—defined by the U.S. Department of Agriculture as members of certain racial and ethnic minority groups and women—may face challenges in obtaining agricultural credit.

GAO was asked to provide information on the implications of establishing an FCS-funded grant program for socially disadvantaged farmers and ranchers. This report (1) describes considerations for policymakers and potential challenges such a program might face, (2) examines potential effects of a grant program on Farm Credit Banks, FCS, and borrowers, and (3) examines the stability of funding from net income for a potential FCS grant program.

GAO analyzed FCS data for 2013–2022 to examine the potential effects of a grant program. GAO also compared FCS data that reflected more and less stressful periods for FCS (1984–1993 and 2013–2022, respectively). GAO interviewed officials from the Farm Credit Administration, Farm Credit Banks, Farm Credit Council, and socially disadvantaged farmer and rancher advocacy groups.

In a letter representing the views of its bank members, the Farm Credit Council stated that the report is comprehensive but raised concerns about some of the analyses. GAO stands behind its analyses.

For more information, contact William B. Shear at (202) 512-8678 or ShearW@gao.gov.