Armed Forces Retirement Home: Congress and Agency Management Should Take Actions to Improve Financial Sustainability

Fast Facts

The Armed Forces Retirement Home is an independent federal entity that provides housing, health care, and other services to certain retired and disabled military personnel.

AFRH faces serious financial challenges as revenues decrease and costs increase over time. The trust fund that finances AFRH's operations is at risk of being exhausted in 20 years. AFRH has some proposals to address these challenges, but it needs help from Congress to implement them.

Congress should consider taking action to address AFRH's financial shortfalls. We also made 7 recommendations to AFRH, including that it develop more detailed plans for its proposals.

AFRH staff member assisting a resident at the Gulfport, MS facility

Highlights

What GAO Found

The Armed Forces Retirement Home (AFRH) prepares at least four financial projections yearly for varying purposes. However, GAO found that AFRH's processes for preparing these projections do not conform to actuarial standards and practices. Specifically, AFRH used inaccurate and inconsistent data, did not have sufficient supporting information for its assumptions of future events and values, and did not make trust fund projections based on reasonable assumptions of expected occupancy levels. Without policies and procedures for preparing financial projections to help ensure staff consistently apply relevant standards and consult with appropriate experts, such as actuaries, AFRH increases the risk that its projections will not be useful for decision-making.

AFRH has identified several proposals to generate revenue and address potential financial shortfalls. However, challenges affect its plans to implement them, including factors outside of AFRH's control. AFRH's planned proposals include a statutory increase in military withholdings, requiring all military service members who are currently eligible for AFRH residency to contribute, and obtaining health and medical care reimbursements from programs such as TRICARE and Medicare for services it provides. However, these proposals require actions from Congress for AFRH to effectively implement them.

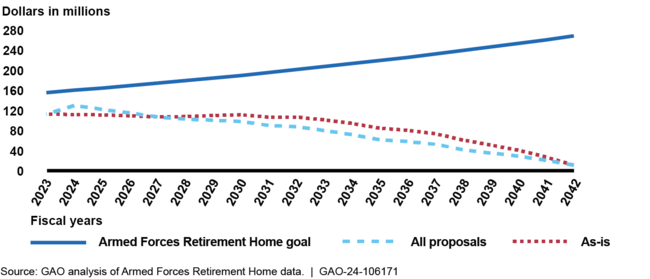

GAO developed projections of AFRH's trust fund balance through fiscal year 2042 under two scenarios: AFRH continuing to operate as-is and AFRH operating with all quantifiable proposals implemented. GAO's analysis shows that whether AFRH continues to operate under its current scenario or implements all proposals, the trust fund will likely continue to decline without other significant efforts to bolster it (see figure). Additionally, AFRH is not projected to meet its goal for the trust fund balance.

GAO Projection of Armed Forces Retirement Home's Trust Fund Balance

AFRH has not achieved its goals to raise its declining occupancy or to implement its other proposals. Also, AFRH faces further financial risks from costly repairs to deteriorating facilities. AFRH has not developed plans to address these issues. Without further actions, AFRH may continue to face financial shortfalls that in the future could affect its ability to fulfill its mission.

Why GAO Did This Study

AFRH is an independent entity within the executive branch designed to provide housing, health care, and well-being assistance to eligible veterans. AFRH is financed through a dedicated trust fund. However, certain revenue sources for its funding have decreased or remained static over time while costs have increased. To address its financial challenges without cutting services to residents, AFRH has worked to identify new revenue sources to help rebuild its trust fund balance.

House Report 117-397 includes a provision for GAO to review the financial sustainability of AFRH. GAO examined the extent to which AFRH projected estimated revenues and expenses for its trust fund through 2042, and developed plans to address any potential financing shortfalls, among other objectives.

GAO reviewed relevant laws, federal guidance, audit reports, and agency guidance and policies; interviewed agency officials and actuarial experts; conducted site visits; and developed a projection to analyze AFRH's financial position.

Recommendations

Congress should consider taking action to address AFRH's financial shortfalls and may wish to consider actions proposed by AFRH management. GAO is also making seven recommendations to AFRH, including that it develop policies for financial projections and plans for revenue-generating proposals. AFRH agreed with four recommendations, partially agreed with one, and did not agree with two. GAO believes all recommendations are warranted.

Matter for Congressional Consideration

| Matter | Status | Comments |

|---|---|---|

Congress should consider taking action to address AFRH's financial shortfalls. This could include consideration of some level of continued General Fund transfers and the following proposals by AFRH management:

|

Congress directed DOD to provide a briefing no later than April 2025 to discuss any impediments with the authority within the Medicare-Eligible Retiree Health Care Fund statute to transfer funds to the Armed Forces Retirement Home (AFRH). In the FY 2026 appropriations process, Congress authorized $27 billion to be transferred from the General Fund to AFRH (PL 119-37). As of February 2026, there was no pending legislation that would address AFRH funding. We will continue to monitor. |

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Armed Forces Retirement Home | AFRH's Chief Operating Officer should develop and implement policies and procedures for preparing financial projections, including consistent application of relevant standards and inclusion of individuals with the appropriate expertise, such as an actuary. (Recommendation 1) |

AFRH and DOD concurred with this recommendation. AFRH's Chief Operating Officer approved an updated financial management directive in April 2024. As of February 2026, AFRH reported that it consulted with the DOD's Office of the Actuary, which advised that its expertise narrowly focuses on the Military Retirement and Health Care Fund, related defined-benefit programs, and lacks experience with life plan community-style models. As a result, the office is unable to provide practical guidance or modeling support tailored to AFRH's resident population, service mix, or trust-fund structure. AFRH also reported that it conducted an actuarial study that concluded no clearly defined, cost-effective actuarial service offerings fit AFRH's statutory mission and funding construct. Additionally, AFRH's exploratory efforts indicated that applying a private-sector life plan community actuarial model would first require substantial conceptual work -- effectively designing a bespoke methodology -- before producing actionable output. We acknowledge AFRH's steps to consult DOD and private-sector actuarial firms. However, AFRH remains a retirement community with uncertain future costs and revenues, thus the need to develop adequate projections that requires expertise in projection modeling, assessing data adequacy, and making informed assumptions about economic and demographic factors affecting future costs and revenues, as well as modeling sensitivity to key assumptions. These needs are common to life plan communities notwithstanding certain unique features of AFRH; therefore, this recommendation remains valid. Although AFRH prepares financial projections, including a 20-year projection, our findings indicated it was insufficient, resulting in inadequate information for decision-makers. We will continue to monitor AFRH's efforts to address this recommendation.

|

| Armed Forces Retirement Home | AFRH's Chief Operating Officer, in coordination with the Secretary of Defense, should take steps to ensure that AFRH has an oversight body with the responsibilities and qualifications outlined in federal internal control standards, and consider whether the advisory council could be structured in a way to serve this role. (Recommendation 2) |

AFRH and DOD partially concurred with this recommendation, stating that AFRH has abundant oversight and external control mechanisms. AFRH noted that its advisory council is not appropriate as an oversight body. However, as of January 2025, it updated AFRH Directive 3-1, Financial Management, it's Financial Management Manual, and standard operating procedures (SOP). AFRH also noted that it holds AFRH Advisory Council meetings and briefings on its financials on an ongoing basis. Although the estimated completion dates remain unknown, AFRH stated that DOD is in the process of updating its policies on AFRH (DOD Instruction 1000.28) and issue an enterprise risk management framework (DOD Instruction 5010.40). While federal internal control standards state that federal government organizations may have key stakeholders for an entity, such as the White House and Office of Management and Budget; the roles and responsibilities of an oversight body differ from those of key stakeholders. The oversight body works with these key stakeholders to understand their expectations and help the federal entity fulfill these expectations, if appropriate. The overall intent of this recommendation is to ensure that AFRH has an appropriately structured oversight body for its internal control system, and that the designated oversight body has documented roles and responsibilities to effectively oversee AFRH's development and performance of control activities. AFRH and DOD previously noted they identified officials composing the oversight body with authority to direct and act as described in federal internal control standards (GAO-14-704G). AFRH updated Directive 3-1 and the Financial Management Manual to assign responsibilities for AFRH's day-to-day oversight and AFRH functions. However, these are not functions of an oversight body. We continue to emphasis the importance of a separate oversight body, such as the Advisory Council, that has the authority to direct and act as described in federal internal control standards. We will continue to monitor AFRH's efforts to address this recommendation.

|

| Armed Forces Retirement Home | AFRH's Chief Operating Officer should develop a written plan for managing occupancy levels at both campuses that is consistent with management's goal and industry standards. (Recommendation 3) |

AFRH and DOD partially concurred with this recommendation and stated that goals and initiatives were laid out regarding occupancy in AFRH's strategic plans, budget submissions, and other documents. However, neither the strategic plan nor AFRH's budget submissions include detailed written plans for how it intends to execute initiatives to achieve its objectives and goals. AFRH updated its admissions program directive, procedures, and processes including elements to further define and operationalize these plans. As of February 2026, AFRH noted it is in the process of updating its occupancy management plan using industry data with an estimated completion date of March 31, 2026. We will continue to monitor AFRH's efforts to address this recommendation.

|

| Armed Forces Retirement Home | AFRH's Chief Operating Officer should develop and implement policies and procedures for estimating deferred maintenance costs and reporting fiscal exposures for all of its facilities. (Recommendation 4) |

AFRH and DOD concurred with this recommendation. In January 2025, AFRH noted that the General Services Administration is targeting to enter AFRH's data to its real property profile in fiscal year 2026. Additionally, as of February 2026, AFRH noted it completed a contract to assess the condition of active historic structures and will contract for assessments of active non-historic structures and inactive structures as funds are available. It also stated it will use the lessons learned from the condition assessments to develop and implement deferred maintenance policies, procedures, and reporting. AFRH has an estimated completion date of November 30, 2026. We will continue to monitor AFRH's efforts to address this recommendation.

|

| Armed Forces Retirement Home | AFRH's Chief Operating Officer should update its financial management policy to include specific implementing guidance (SOPs) for staff performing the daily procedures related to the financial management of its trust fund, and to reflect current processes. (Recommendation 5) |

AFRH and DOD concurred with this recommendation. AFRH updated and released its financial management policies. As of February 2026, AFRH Campus Administrators at each campus developed an SOP to assist staff with daily financial management related tasks. The Chief Finance Officer reviewed the SOPs to ensure alignment with the agency's updated policies and implemented the SOPs in January 2026.

|

| Armed Forces Retirement Home | AFRH's Chief Operating Officer should develop and document a process to periodically review existing financial management policies and procedures to ensure that they remain up to date. (Recommendation 6) |

AFRH and DOD concurred with this recommendation. AFRH published AFRH Directive 3-1, Financial Management, and the Financial Management Manual. As of February 2026, AFRH updated its Publication Management Directive to document a process for annual reviews of policy documentation.

|

| Armed Forces Retirement Home | AFRH's Chief Operating Officer, in coordination with the Secretary of Defense, should document, in a charter or other document, expected tasks for an oversight body as outlined in federal internal control standards. Such tasks should include providing oversight to AFRH management in developing and performing control activities and periodically updating policies and procedures as necessary. (Recommendation 7) |

AFRH and DOD partially concurred with this recommendation, linking their comments and estimated completion dates to the corrective actions for recommendation 2. We continue to believe that the validity of this recommendation is warranted and will continue to follow-up with AFRH about efforts to address this recommendation.

|