Retirement Security: Debt Increased for Older Americans over Time, but the Implications Vary by Debt Type

Fast Facts

Older Americans held nearly half of the total debt in 2020—debt that may affect their retirement security. We found that older Americans had significantly more debt in 2016 than in 1989.

We also found that low-income, older Americans had greater "debt stress"—the ratio of debts to assets. In 2016, debt stress was about two times higher for minority households than White households.

Experts said that different debt types (credit cards, housing debt, etc.) have varying effects on retirement security. For example, carrying credit card debt with high variable interest rates may make it difficult for the elderly to save for retirement.

Highlights

What GAO Found

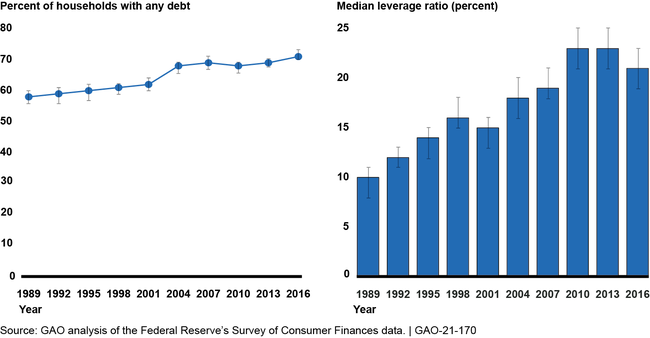

Americans age 50 or older had significantly more debt in 2016 than in 1989, according to GAO's analysis of Survey of Consumer Finances (SCF) data.

- Debt. The share of older households with debt was 71 percent in 2016 compared to 58 percent in 1989 (see figure). The median debt amount for older households with debt was about three times higher in 2016 ($55,300) than in 1989 ($18,900 in real 2016 dollars) and the share of older households with home, credit card, and student loan debt was significantly higher in 2016 than in 1989.

- Debt stress. The median ratio of debt to assets—known as the leverage ratio, a measure of debt stress—for older households was twice as high in 2016 than in 1989.

- Adverse debt outcomes. Measures of older individuals' adverse debt outcomes, including their share of mortgage and credit card debt that was late by at least 90 days, generally followed economic trends, peaking after the Great Recession of 2007-2009, according to GAO's analysis of Consumer Credit Panel (CCP) data from 2003 to 2019. However, the share of student loan debt that was late was significantly higher for older individuals in 2019 than in 2003.

These trends in debt, debt stress, and adverse debt outcomes varied by older Americans' demographic and economic characteristics, including their age, credit score, and state of residence. For example, from 2003 to 2019, individuals in their late 70s often had higher shares of credit card and student loan debt that was late than those aged 50-74. In addition, older individuals with credit scores below 720—including those with subprime, fair, or good credit—had median student loan debt amounts that were more than twice as high in 2019 as in 2003. Further, older individuals in the Southeast and West had much higher median mortgage and student loan debt, as well as student loan delinquency rates, in 2019 than in 2003.

Percent of Households Age 50 or Older with Any Debt (Left) and Median Leverage Ratio (Right) for These Households, 1989 to 2016

Note: The bars above and below the lines represent the bounds of 95 percent confidence intervals.

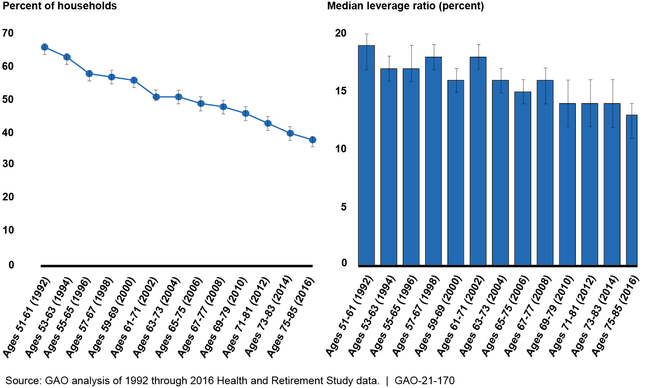

While older Americans' overall debt and debt stress decreased as they aged, those in low-income households experienced greater debt stress according to GAO's analysis of Health and Retirement Study (HRS) data, a nationally representative survey that follows the same individuals over time. The share of older households in this cohort that had debt continuously decreased as they aged, from about 66 percent of households in 1992 to 38 percent in 2016, and the median leverage ratio declined from about 19 to 13 percent over this period (see figure). However, low-income households in this cohort consistently had greater levels of debt stress than high-income households. This disparity in debt stress increased as these households aged.

Estimated Percent of Households with Any Debt for Those Born in 1931-1941 (Left) and Median Leverage Ratio for Those Households from 1992-2016 (Right)

Notes: The lines overlapping the bars represent 95 percent confidence intervals.

According to experts GAO interviewed, differences in debt type (that is, credit card versus housing debt) and debt stress levels will have varying effects on the retirement security of different groups. For example, experts noted that credit card debt has negative implications for older Americans' retirement security because credit cards often have high, variable interest rates and are not secured by any assets. In contrast, an increase in mortgage debt may have positive effects on retirement security because a home is generally a wealth-building asset. Experts also said that older individuals with lower incomes and unexpected health expenses are likely to experience greater debt stress, which can negatively affect retirement security. Similarly, experts noted that the increased debt stress faced by low-income households is also faced by non-White households. Further, GAO's analysis of data from the Survey of Consumer Finances found that in 2016, debt stress levels were about two times higher for Black, Hispanic/Latino, and Other/multiple-race households than for White households.

Experts GAO interviewed noted it is too early to evaluate the retirement security implications of the recession caused by the COVID-19 pandemic, in part because CARES Act provisions suspend or forbear certain debt payments. However, as with past recessions, the COVID-19-related recession may reveal any economic fragility among older Americans who, for example, lost jobs or cannot work because of the pandemic.

Why GAO Did This Study

GAO reported in 2019 that an estimated 20 percent of older American households aged 55 or older had less than $22,000 in income in 2016 and GAO reported in 2015 that about 29 percent of older households had neither retirement savings accounts (such as a 401(k) plan) nor a defined benefit plan in 2013. Older Americans held nearly half of the total outstanding debt in 2020—and these debts may affect retirement security. The Census Bureau projects the number of older Americans will increase.

GAO was asked to report on debt held by older Americans. This report examines (1) how the types, levels, and outcomes of debt changed for older Americans over time, including for different demographic and economic groups; (2) how the types and levels of debt held by the same older Americans changed as they aged, including for those in different demographic groups; and (3) the implications of these debt trends for the general retirement security of older Americans and their families.

GAO analyzed data from two nationally representative surveys–the SCF (1989 through 2016 data) and the HRS (1992 through 2016 longitudinal data)–and nationally representative administrative data from the Federal Reserve Bank of New York's CCP (2003 through 2019). These datasets were the most recent available at the time of GAO's analyses. GAO also reviewed studies and interviewed experts that GAO identified from these studies to further analyze the relationship between debt and retirement security.

For more information, contact Kris Nguyen, (202) 512-7215 or NguyenTT@gao.gov.