Covid-19: Opportunities to Improve Federal Response and Recovery Efforts

Fast Facts

In response to the COVID-19 pandemic, Congress appropriated $2.6 trillion in emergency assistance for people, businesses, the health care system, and state and local governments.

How are federal agencies administering this spending?

We found that the Small Business Administration processed over $512 billion in guaranteed small business loans, but isn’t ready to address fraud risks and hasn’t said how it plans to oversee the loans.

Also, the IRS and Treasury made 160.4 million payments worth $269.3 billion to taxpayers as of May 31—including payments to more than a million deceased individuals.

Our recommendations address these and other issues.

Signing pointing toward COVID-19 screening

Highlights

What GAO Found

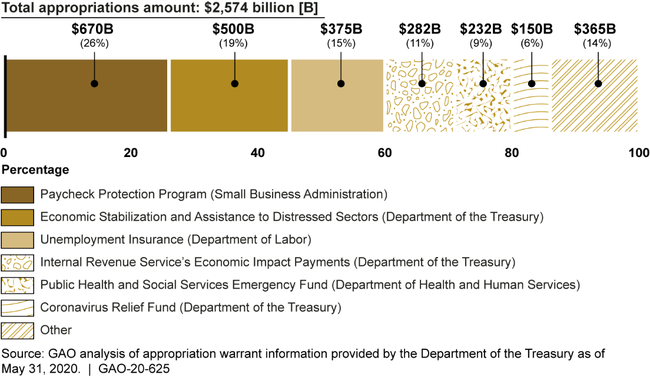

In response to the national public health and economic threats caused by COVID-19, four relief laws were enacted as of June 2020, including the CARES Act, in March 2020. These laws have appropriated $2.6 trillion across the government. Six areas—Paycheck Protection Program (PPP); Economic Stabilization and Assistance to Distressed Sectors; unemployment insurance; economic impact payments; Public Health and Social Services Emergency Fund; and Coronavirus Relief Fund—account for 86 percent of the appropriations (see figure).

Appropriations for COVID-19 Response from COVID-19 Relief Laws Enacted as of May 31, 2020

Note: COVID-19 relief laws enacted as of May 31, 2020 include the Coronavirus Preparedness and Response Supplemental Appropriations Act, 2020, Pub. L. No. 116-123, 134 Stat. 146; Families First Coronavirus Response Act, Pub. L. No. 116-127, 134 Stat. 178 (2020); CARES Act, Pub. L. No. 116-136, 134 Stat. 281 (2020); and Paycheck Protection Program and Health Care Enhancement Act, Pub. L. No. 116-139, 134 Stat. 620 (2020).

These amounts represent appropriation warrants issued as of May 31, 2020, by the Department of the Treasury to agencies in response to appropriations made by COVID-19 relief laws. A warrant is an official document issued upon enactment of an appropriation that establishes the amount of money authorized to be withdrawn from the Treasury. These amounts could increase in the future for programs with indefinite appropriations. In addition, this figure does not represent transfers of funds that agencies may make between accounts or transfers of funds they may make to other agencies, to the extent authorized by law.

Total federal spending data are not readily available because, under Office of Management and Budget guidance, federal agencies are not directed to report COVID-19 related obligations (financial commitments) and expenditures until July 2020. It is unfortunate that the public will have waited more than 4 months since the enactment of the CARES Act for access to comprehensive obligation and expenditure information about the programs funded through these relief laws.

In the absence of comprehensive data, GAO collected obligation and expenditure data from agencies, to the extent practicable, as of May 31, 2020. For the six largest spending areas, GAO found obligations totaled $1.3 trillion and expenditures totaled $643 billion. The majority of the difference was due to the PPP, for which the Small Business Administration (SBA) obligated $521 billion. The amounts for loan guarantees will not be considered expenditures until the loans are forgiven, and for those that are not forgiven, whether they are timely repaid.

GAO also collected expenditure data on other programs affected by the federal response. For example, GAO also found that the Department of Health and Human Services (HHS) has provided $7 billion in COVID-19 Medicaid funding related to a temporary increase in the Federal Medical Assistance Percentage (FMAP), the statutory formula the federal government uses to match states' Medicaid spending. Based on the information GAO collected, government-wide spending totals at least $677 billion, as of May 31, 2020.

Given the sweeping and unfolding public health and economic crisis, agencies from across the federal government were called on for immediate assistance, requiring an unprecedented level of dedication and agility among the federal workforce, including those serving on the front lines to quickly establish services for those infected with the virus. Consistent with the urgency of responding to serious and widespread health issues and economic disruptions, agencies have given priority to moving swiftly where possible to distribute funds and implement new programs. As tradeoffs were made, however, agencies have made only limited progress so far in achieving transparency and accountability goals.

GAO has identified several challenges related to the federal response to the crisis, as well as recommendations to help address these challenges, including the following:

Viral testing. The Centers for Disease Control and Prevention (CDC) reported incomplete and inconsistent data from state and jurisdictional health departments on the amount of viral testing occurring nationwide, making it more difficult to track and know the number of infections, mitigate their effects, and inform decisions on reopening communities. However, HHS issued guidance on June 4, 2020, to laboratories that identifies required data elements to collect and how to report it to CDC. GAO will continue to examine activities related to COVID-19 testing.

Distribution of supplies. The nationwide need for critical supplies to respond to COVID-19 quickly exceeded the quantity of supplies contained in the Strategic National Stockpile, which is designed to supplement state and local supplies during public health emergencies. HHS has worked with the Federal Emergency Management Agency (FEMA) and the Department of Defense (DOD) to increase the availability of supplies. However, federal, state, and local officials have expressed concerns about the distribution, acquisition, and adequacy of supplies. GAO will continue to examine these issues as well as the administration's efforts to mitigate supply gaps.

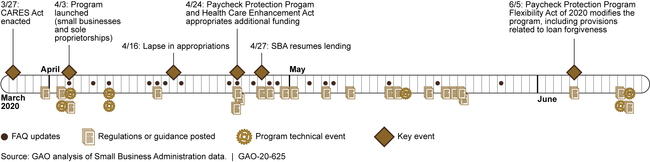

Paycheck Protection Program. As of June 12, 2020, the Small Business Administration (SBA) had rapidly processed over $512 billion in 4.6 million guaranteed loans through private lenders to small businesses and other organizations adversely affected by COVID-19. The $512 billion represents loan obligations for SBA and does not include lender fees. As of May 31, 2020, SBA had expended about $2 billion in lender fees. SBA moved quickly to establish a new nationwide program, but the pace contributed to confusion and questions about the program and raised program integrity concerns. First, borrowers and lenders raised a number of questions about the program and eligibility criteria. To address these concerns, SBA and the Department of the Treasury (Treasury) issued a number of interim final rules and several versions of responses to frequently asked questions (see figure). However, questions and confusion remained. The Paycheck Protection Program Flexibility Act of 2020, enacted in June 2020, modified key program components. Second, to help quickly disburse funds, SBA allowed lenders to rely on borrower certifications to determine borrowers' eligibility, raising the potential for fraud. GAO recommends that SBA develop and implement plans to identify and respond to risks in PPP to ensure program integrity, achieve program effectiveness, and address potential fraud. SBA neither agreed nor disagreed, but GAO believes implementation of its recommendation is essential.

Timeline for Paycheck Protection Program, as of June 12, 2020

Economic impact payments. The Internal Revenue Service (IRS) and the Treasury moved quickly to disburse 160.4 million payments worth $269 billion. The agencies faced difficulties delivering payments to some individuals, and faced additional risks related to making improper payments to ineligible individuals, such as decedents, and fraud. For example, according to the Treasury Inspector General for Tax Administration, as of April 30, almost 1.1 million payments totaling nearly $1.4 billion had gone to decedents. GAO recommends that IRS should consider cost-effective options for notifying ineligible recipients how to return payments. IRS agreed with the recommendation.

Unemployment Insurance (UI). States are implementing three new, federally funded UI programs created by the CARES Act and, as of May 2020, states have received more than 42 million UI claims. The Department of Labor (DOL) has taken steps to help states manage demand, but DOL is developing its approach to overseeing the new UI programs. GAO will be evaluating DOL's monitoring efforts in future reports. Further, the UI program is generally intended to provide benefits to individuals who have lost their jobs; under PPP, employers are generally required to retain or rehire employees for full loan forgiveness. According to DOL, no mechanism currently exists that could capture information in real time about UI claimants who may receive wages paid from PPP loan proceeds. GAO recommends that DOL, in consultation with SBA and Treasury, immediately provide help to state unemployment agencies that specifically addresses PPP loans, and the risk of improper payments associated with these loans. DOL neither agreed nor disagreed with the recommendation, but noted it was planning forthcoming guidance.

Contract obligations. Government-wide contract obligations in response to the COVID-19 pandemic totaled about $17 billion as of May 31, 2020. Goods procured include ventilators; services contracted for include vaccine development. In addition, the CARES Act provided $1 billion for Defense Production Act (DPA) purchases—$76 million of which, for example, was awarded to increase production of N95 respirators.

GAO recommends Congress consider taking legislative action in the following areas:

Aviation-preparedness plan. In 2015, GAO recommended that the Department of Transportation (DOT) work with federal partners to develop a national aviation-preparedness plan for communicable disease outbreaks. DOT agreed, but as of May 2020, maintains that HHS and DHS should lead the effort. Thus far, no plan exists. GAO recommends Congress take legislative action to require DOT to work with relevant agencies and stakeholders to develop a national aviation-preparedness plan to ensure safeguards are in place to limit the spread of communicable disease threats from abroad while at the same time minimizing any unnecessary interference with travel and trade.

Full access to death data. The number of economic impact payments going to decedents highlights the importance of consistently using key safeguards in providing government assistance to individuals. IRS has access to the Social Security Administration's full set of death records, but Treasury and its Bureau of the Fiscal Service, which distribute payments, do not. GAO recommends that Congress provide Treasury with access to the Social Security Administration's full set of death records, and require that Treasury consistently use it, to help reduce similar types of improper payments.

Medicaid. GAO previously found that during economic downturns—when Medicaid enrollment can rise and state economies weaken—the FMAP formula does not reflect current state economic conditions. GAO previously developed a formula that offers an option for providing temporary automatic, timely, and targeted assistance. GAO recommends Congress use this formula for any future changes to the FMAP during the current or any future economic downturn to help ensure that the federal funding is targeted and timely.

Evolving lessons from the initial response highlight the importance of the following:

- Establishing clear goals and defining roles and responsibilities for the wide range of federal agencies and other key players are critically important actions when preparing for pandemics and addressing an unforeseen emergency with a whole-of-government response.

- Providing clear, consistent communication in the midst of a national emergency—among all levels of government, with health care providers, and to the public—is key.

- Collecting and analyzing adequate and reliable data can inform decision-making and future preparedness—and allow for midcourse changes in response to early findings.

- Establishing transparency and accountability mechanisms early on provides greater safeguards and reasonable assurance that federal funds reach the intended people, are used for the intended purposes, help ensure program integrity, and address fraud risks.

Why GAO Did This Study

The outbreak of COVID-19 quickly spread around the globe. As of June 17, 2020, the United States had over 2 million reported cases of COVID-19, and over 100,000 reported deaths, according to federal agencies. Parts of the nation have also seen severely strained health care systems. Also, the country has experienced a significant and rapid downturn in the economy. Four relief laws, including the CARES Act, were enacted as of June 2020 to provide appropriations to address the public health and economic threats posed by COVID-19. In addition, the administration created the White House Coronavirus Task Force.

The CARES Act includes a provision for GAO to report bimonthly on its ongoing monitoring and oversight efforts related to the COVID-19 pandemic. This initial report examines key actions the federal government has taken to address the COVID-19 pandemic and evolving lessons learned relevant to the nation's response to pandemics, among other things.

GAO reviewed data and documents from federal agencies about their activities and interviewed federal and state officials as well as industry representatives. GAO also reviewed available economic, health, and budgetary data.

Recommendations

GAO is making 3 new recommendations for agencies and 3 matters for consideration for Congress that are detailed in this Highlights and in the report.

Matter for Congressional Consideration

| Matter | Status | Comments |

|---|---|---|

| In the absence of efforts to develop a plan, we urge Congress to take legislative action to require the Secretary of Transportation to work with relevant agencies and stakeholders, such as the Departments of Health and Human Services and Homeland Security, and members of the aviation and public health sectors, to develop a national aviationpreparedness plan to ensure safeguards are in place to limit the spread of communicable disease threats from abroad while at the same time minimizing any unnecessary interference with travel and trade. (Matter for Consideration 1) | With the recurring threat of communicable diseases quickly spreading around the globe through air travel, it is imperative that the U.S. aviation system is sufficiently prepared to help respond to any future communicable disease threat. GAO previously recommended that the Secretary of Transportation work with relevant stakeholders, such as the Department of Health and Human Services (HHS), to develop a national aviation-preparedness plan for communicable disease outbreaks. In 2020, GAO reported that while the Department of Transportation (DOT) agreed that an aviation-preparedness plan is needed, no such plan had been developed. DOT has previously maintained that because HHS and the Department of Homeland Security (DHS) are responsible for communicable disease response and preparedness planning, respectively, these departments should lead any efforts to address planning for communicable disease outbreaks, including for transportation. GAO maintains that DOT is in the best position to lead a multiagency effort to develop a national aviation-preparedness plan and that such a plan is critically needed. Until a national aviation-preparedness plan is developed, the United States risks being unprepared to respond quickly and effectively to communicable disease events, including the continued spread of COVID-19. Therefore, GAO recommended that Congress take legislative action to require the Secretary of Transportation to work with relevant agencies and stakeholders to develop a national aviation preparedness plan. In 2022, Congress passed and the President signed into law the Consolidated Appropriations Act of 2023, which among other things, requires the Secretary of Transportation, in coordination with the Secretaries of HHS and DHS, and the heads of other Federal departments or agencies as the Secretary of Transportation consider appropriate, to develop a national aviation preparedness plan for communicable disease outbreaks. This legislative requirement will help ensure that DOT develops a national aviation preparedness plan to minimize and quickly respond to future communicable disease events and garner international cooperation in addressing pandemics. | |

| To provide agencies access to Social Security Administration's more complete set of death data, we urge Congress to provide the Department of the Treasury with access to the Social Security Administration's full set of death records, and to require that the Department of the Treasury consistently use it. (Matter for Consideration 2) | In December 2020, Congress passed and the President signed into law the Consolidated Appropriations Act, 2021, which requires the Social Security Administration (SSA), to the extent feasible, to share its full death data with Treasury's Do Not Pay working system for a 3-year period, effective on the date that is 3 years from enactment of this Act. Sharing this data will allow agencies to enhance their efforts to identify and prevent improper payments to deceased individuals. Therefore, it will be important for SSA and Treasury to work together to implement this legislation. | |

| To help ensure that federal funding is targeted and timely, we urge Congress to use GAO's Federal Medical Assistance Percentage formula for any future changes to the Federal Medical Assistance Percentage during the current or any future economic downturn. (Matter for Consideration 3) | Our past work has found that during economic downturns-when Medicaid enrollment can increase and state economies weaken-the formula, which is based on each state's per capita income, does not reflect current state economic conditions. No congressional action has been taken as of February 2026. |

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Department of Labor | The Secretary of Labor should, in consultation with the Small Business Administration and the Department of the Treasury, immediately provide information to state unemployment agencies that specifically addresses the Small Business Administration's Paycheck Protection Program loans, and the risk of improper payments associated with these loans. (Recommendation 1) |

The Department of Labor (DOL) neither agreed nor disagreed with our recommendation. Following our recommendation, DOL issued guidance on August 12, 2020, that clarified that individuals working full-time and being paid through PPP are not eligible for unemployment insurance (UI), and that individuals working part-time and being paid through PPP would be subject to certain state policies, including state policies on partial unemployment to determine their eligibility for UI benefits. Further, the guidance clarified that individuals being paid through PPP but not performing any services would similarly be subject to certain provisions of state law, and noted that an individual receiving full compensation would be ineligible for UI.

|

| Internal Revenue Service | The Commissioner of Internal Revenue should consider cost-effective options for notifying ineligible recipients on how to return payments. (Recommendation 2) |

Treasury and the Internal Revenue Service (IRS) took steps to implement our recommendation, such as providing instructions on the IRS website requesting that individuals voluntarily mail the appropriate economic impact payment (EIP) amount sent to the decedent back to IRS, for both electronic and paper check payments. Treasury has also held and canceled payments made to decedents, along with those that have been returned. As of April 30, 2021, around 57 percent (just over $704 million) of the $1.2 billion in first-round payments sent to deceased individuals had been recovered. As of March 2021, Treasury and IRS had not taken any further action to recoup payments made to decedents that had not been returned. IRS officials determined that further actions, such as initiating erroneous refund cases against the estates of the decedents to which payments were made and not returned, could be burdensome to taxpayers, the federal court system, and IRS. As such, IRS officials concluded that doing so is not prudent at this time.

|

| Small Business Administration |

Priority Rec.

The Administrator of the Small Business Administration should develop and implement plans to identify and respond to risks in the Paycheck Protection Program to ensure program integrity, achieve program effectiveness, and address potential fraud, including in loans of $2 million or less. (Recommendation 3) |

At the time of our report, SBA neither agreed nor disagreed with our recommendation. In late December 2020, SBA provided a Master Review Plan outlining steps it planned to take to review the PPP loans made in 2020. The document described three steps in the process: automated screenings of all loans, manual reviews of selected loans, and quality control reviews to ensure the quality, completeness, and consistency of the review process. Most of the loan reviews were to be conducted by contractors with SBA oversight. SBA later updated the plan in January 2022 to incorporate changes to its oversight, including the screening performed of 2021 loan applications before the loans were originated. To implement the plan, SBA's loan review contractor conducted automated screenings for all of the PPP loans made in 2020 in August and early September 2020. Specifically, the contractor used an automated rules-based tool to compare PPP loan data against publicly available information and apply eligibility and fraud detection rules to identify anomalies or attributes that may indicate noncompliance with eligibility requirements, fraud, or abuse. For example, the tool would flag loans made to a borrower in active bankruptcy or one who used the tax identification number of a deceased person. SBA and its contractor began conducting manual reviews of flagged loans of less than $2 million in early November 2020, and of loans of $2 million or more in January 2021. Starting in January 2021, SBA screened all PPP loans before the lender approved the loan. To screen these loans, the contractor used a subset of the automated screening rules it used to review the 2020 loans for potential indicators of non-eligibility or fraud risks. According to SBA officials, contractor staff had completed about 78,000 manual reviews and referred about 8,900 loans to SBA for further review, as of November 15, 2021. SBA will continue to conduct manual reviews of flagged loans.

|