Cost Accounting Standards: Board Has Taken Initial Steps to Meet Recent Legislative Requirements

Fast Facts

When contracting for goods and services, the government uses Cost Accounting Standards to help ensure contractors accurately represent their costs and make contract cost information more comparable.

But Congress and others are concerned that the burden of a separate cost accounting system, on top of the accepted industry standard system, may deter some companies from competing for federal contracts.

Congress directed the Cost Accounting Standards Board to explore ways to make the federal standards more like the industry standards. We looked at the Board’s initial steps, which include figuring out where the federal and industry standards overlap.

money

Highlights

What GAO Found

The Cost Accounting Standards Board (the Board) is generally meeting recent legislative requirements and has taken initial steps to assess the extent to which the government's Cost Accounting Standards (CAS) can be conformed with a set of 12commercial financial reporting principles known as Generally Accepted Accounting Principles (GAAP).

Comprising five members representing the government and industry, the Board issued 19 standards between 1972 and 1980. After that point, the Board met intermittently until 2016. At that time, Congress included a provision in the National Defense Authorization Act for Fiscal Year 2017 to require the Board to meet quarterly, to review CAS-related disputes, to conform CAS with GAAP where practicable, and to report annually to Congress on its efforts, among other things.

Since the legislation went into effect, the Board has met regularly, has been briefed on CAS-related disputes, and is preparing its initial report to Congress. The Board has also taken initial steps to assess the extent to which CAS can be conformed with GAAP. The Board summarized its approach in a March 2019 staff discussion paper, which it released for public comment. In it, the Board:

outlined a set of five guiding principles to assess whether proposed CAS changes are necessary and whether those changes would reduce the burden on contractors while protecting the government's interests,

identified a roadmap that prioritized the Board's proposed review of the standards, and

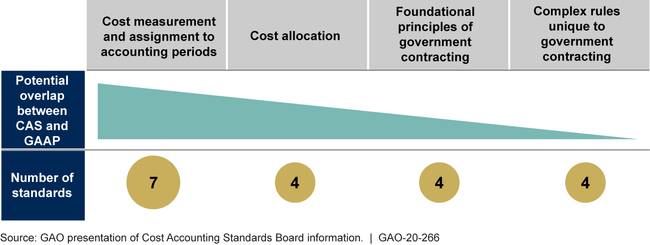

included a preliminary comparison of two of the seven standards identified as having the most overlap with GAAP (see figure).

Cost Accounting Standards Board Initial Assessment of the Potential Overlap between the 19 Cost Accounting Standards (CAS) and Generally Accepted Accounting Principles (GAAP)

Some comments submitted in response to the discussion paper by industry groups stated that each of the 19 CAS should be eliminated unless proven to be absolutely necessary. Board members told GAO they were considering all options for refining CAS but noted that GAAP and CAS are focused on two separate goals—GAAP on businesses' high-level financial performance, CAS on allocating costs to individual government contracts. The Board and other government officials said that eliminating CAS requirements to rely purely on GAAP would limit the government's ability to protect its interests.

Why GAO Did This Study

Each year, the federal government obligates billions of dollars on contracts for which the final costs depend, in part, on the amount of overhead and other costs charged to the contract.

Congress created the Board in 1970. The standards it created ensure contractors appropriately charge costs to government contracts. In contrast, GAAP is a set of financial reporting principles that commercial firms may use in preparing financial statements and which include the basis for recognizing and measuring costs in such statements . Industry representatives and others have raised concerns that complying with CAS may be burdensome and questioned whether the government could rely on GAAP.

In 2016, Congress included a provision in law that the Board, among other things, conform CAS with GAAP, where practicable. Congress also included a provision for GAO to assess Board efforts. This report assesses the extent to which the Board is taking steps to meet legislative requirements and describes the Board's efforts to conform CAS to GAAP.

GAO reviewed applicable laws, regulations and guidance, Federal Register notices and other documentation on the Board's activities. GAO also examined the Board's methodology for comparing CAS to GAAP and its preliminary analysis of two of the cost accounting standards. Finally, GAO interviewed Board members and federal procurement officials.

For more information, contact Timothy J. DiNapoli at (202) 512-4841 or dinapolit@gao.gov.