Retirement Plan Investing: Clearer Information on Consideration of Environmental Social and Governance Factors Would Be Helpful

Highlights

What GAO Found

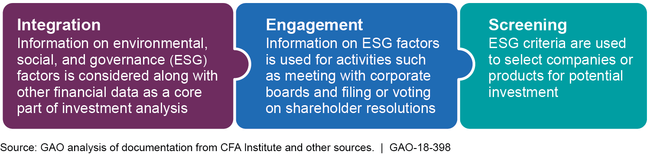

Few retirement plans in the United States incorporate environmental, social, and governance (ESG) factors into their investments according to available data. ESG factors that may affect investment returns include climate risk, executive compensation, and workplace safety issues among others. According to GAO's interviews with seven asset managers, inconsistent data and regulatory uncertainty create challenges to incorporating ESG factors in plan investment management. However, those plans considering ESG factors use various strategies to do so (see figure). Asset managers and plan representatives said they incorporate ESG factors to better manage risks and improve performance.

Strategies Used to Incorporate ESG Factors into Investment Management

The retirement plans GAO reviewed in France, the Netherlands, and the United Kingdom (UK) reported using integration and other strategies to incorporate ESG factors across their investments, particularly to address the risk of climate change. For example, the UK's National Employment Savings Trust—a defined contribution plan—used an ESG integration strategy in developing its default fund for participants who are automatically enrolled and do not select another investment. As part of their ESG strategies, representatives from these plans described targeted efforts to address climate risk related to financial performance. These representatives also said they are subject to governmental policies that encourage plans to address ESG risks.

In the United States, the Department of Labor's (DOL) guidance for private sector plans identifies ESG factors as proper components of investment analysis, but does not fully address uncertainties plans may face. In particular, sponsors of defined contribution plans face uncertainty about whether they may use ESG factors in a qualifying default fund—a widely used option in which a fiduciary is generally not liable for investment losses. DOL's mission includes assisting and educating plan fiduciaries. Providing clearer information about how to use ESG factors would help fiduciaries better understand whether and how to consider these potentially material risks. DOL is also considering steps to collect data on the use of ESG factors by retirement plans.

Why GAO Did This Study

ESG factors have emerged as a way for investors, such as retirement plans, to capture information on potential risks and opportunities that may otherwise not be taken into account. For example, climate change is expected to have widespread impacts according to a key federal study and may pose significant financial risks for long term investors, such as retirement plans that must manage risk to provide benefits for many years to come. A number of large plans in other countries have adopted ESG strategies, but less is known about their use among U.S. plans. Given the emerging use of ESG factors, GAO was asked to examine how such factors are used by retirement plans in the United States and other countries.

GAO examined: (1) the use of ESG factors by U.S. retirement plans, (2) the use of ESG factors by selected retirement plans in other countries, and (3) DOL's guidance on the use of ESG factors by private sector U.S. retirement plans. GAO reviewed available private sector survey data and other documentation and interviewed government officials, asset managers, and plan representatives in the United States, France, the Netherlands, and the United Kingdom—from retirement plans that were identified as leading examples in the use of ESG factors.

Recommendations

GAO is making two recommendations to DOL, including that DOL clarify whether the liability protection offered to qualifying default investment options allows use of ESG factors. DOL neither agreed nor disagreed with GAO's recommendations.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Department of Labor | The Assistant Secretary of Labor for the Employee Benefits Security Administration (EBSA) should clarify whether an Employee Retirement Income Security Act of 1974 plan may incorporate material ESG factors into the investment management for a qualified default investment alternative (QDIA). (Recommendation 1) |

In November 2020, DOL issued a final rule on the use of pecuniary factors, which included procedural and documentation requirements regarding the consideration of such factors and prohibited the use of non-pecuniary factors in QDIAs. In 2021, the Administration issued an Executive Order directing DOL to review the 2020 Final Rule. As part of that review, EBSA reported that it engaged in informal outreach efforts with interested stakeholders. EBSA issued a non-enforcement policy statement on the 2020 Final Rule on March 10, 2021. In October 2021, DOL issued a proposed rule to clarify that ESG factors can be financially material and, as such, may be considered by retirement plan fiduciaries, including in QDIAs. We believe the agency has addressed this recommendation by explicitly stating that the use of material ESG factors is permissible in a QDIA investment option.

|

| Department of Labor | The Assistant Secretary of Labor for EBSA should provide further information to assist fiduciaries in investment management involving ESG factors, including how to evaluate available options, such as questions to ask or items to consider. (Recommendation 2) |

DOL neither agreed nor disagreed with this recommendation. In November 2020, DOL issued a final rule on the use of pecuniary factors, which included procedural and documentation requirements regarding the consideration of such factors and prohibited the use of non-pecuniary factors in Qualified Default Investment Alternatives (QDIA). In 2021, the Administration issued an Executive Order directing DOL to review the 2020 Final Rule. As part of that review, EBSA reported that it engaged in informal outreach efforts with interested stakeholders. EBSA issued a non-enforcement policy statement on the 2020 Final Rule on March 10, 2021. In October 2021, DOL issued a proposed rule to clarify that ESG factors can be financially material and, as such, may be considered by retirement plan fiduciaries, including in QDIAs. Additionally, in February 2022, DOL issued a request for information on what it should do to protect retirement savings from financial risks associated with climate change. In December 2022, DOL issued a final rule regarding retirement plans' use of ESG factors, which included provisions to address challenges raised by plan fiduciaries during their outreach. We believe this final rule provides fiduciaries additional information to assist with investment decisions involving ESG factors.

|