Retirement Security: Shorter Life Expectancy Reduces Projected Lifetime Benefits for Lower Earners

Highlights

What GAO Found

The increase in average life expectancy for older adults in the United States contributes to challenges for retirement planning by the government, employers, and individuals. Social Security retirement benefits and traditional defined benefit (DB) pension plans, both key sources of retirement income that promise lifetime benefits, are now required to make payments to retirees for an increasing number of years. This development, among others, has prompted a wide range of possible actions to help curb the rising future liabilities for the federal government and DB sponsors. For example, to address financial challenges for the Social Security program, various options have been proposed, such as adjusting tax contributions, retirement age, and benefit amounts. Individuals also face challenges resulting from increases in life expectancy because they must save more to provide for the possibility of a longer retirement.

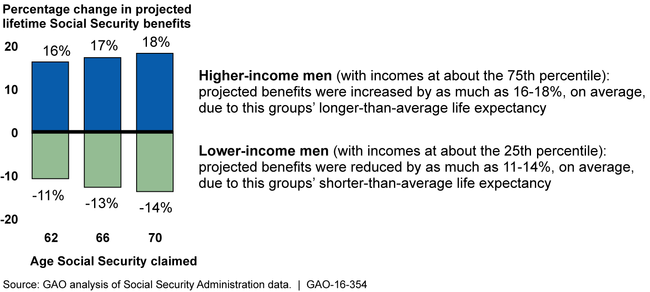

Life expectancy varies substantially across different groups with significant effects on retirement resources, especially for those with low incomes. For example, according to studies GAO reviewed, lower-income men approaching retirement live, on average, 3.6 to 12.7 fewer years than higher-income men. GAO developed hypothetical scenarios to calculate the projected amount of lifetime Social Security retirement benefits received, on average, for men with different income levels born in the same year. In these scenarios, GAO compared projected benefits based on each income groups' shorter or longer life expectancy with projected benefits based on average life expectancy, and found that lower-income groups' shorter-than-average life expectancy reduced their projected lifetime benefits by as much as 11 to 14 percent. Effects on Social Security retirement benefits are particularly important to lower-income groups because Social Security is their primary source of retirement income.

Disparities in Life Expectancy Affect Lifetime Social Security Retirement Benefits

Social Security's formula for calculating monthly benefits is progressive—that is, it provides a proportionally larger monthly earnings replacement for lower-earners than for higher-earners. However, when viewed in terms of benefit received over a lifetime, the disparities in life expectancy across income groups erode the progressive effect of the program.

Why GAO Did This Study

An increase in average life expectancy for individuals in the United States is a positive development, but also requires more planning and saving to support longer retirements. At the same time, as life expectancy has not increased uniformly across all income groups, proposed actions to address the effects of longevity on programs and plan sponsors may impact lower-income and higher-income individuals differently. GAO was asked to examine disparities in life expectancy and the implications for retirement security.

In this report, GAO examined (1) the implications of increasing life expectancy for retirement planning, and (2) the effect of life expectancy on the retirement resources for different groups, especially those with low incomes. GAO reviewed studies on life expectancy for individuals approaching retirement, relevant agency documents, and other publications; developed hypothetical scenarios to illustrate the effects of differences in life expectancy on projected lifetime Social Security retirement benefits for lower-income and higher-income groups based on analyses of U.S. Census Bureau and Social Security Administration (SSA) data; and interviewed SSA officials and various retirement experts.

GAO is making no recommendations in this report. In its comments, SSA agreed with our finding that it is important to understand how the life expectancy in different income groups may affect retirement income.

For more information, contact Charles Jeszeck at (202) 512-7215 or jeszeckc@gao.gov.