Improper Payments: Inspector General Reporting of Agency Compliance under the Improper Payments Elimination and Recovery Act

Highlights

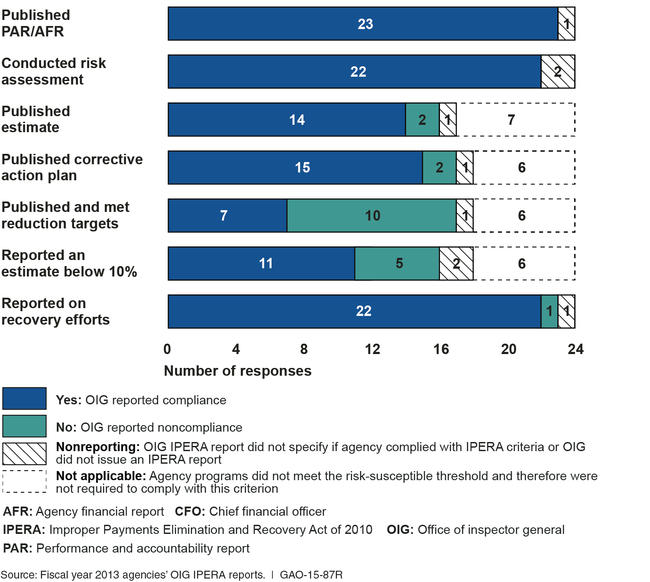

What GAO Found

For fiscal year 2013, the offices of inspector general (OIG) for 13 of the 24 Chief Financial Officer's Act (CFO Act) agencies reported that their agencies complied with all of the Improper Payments Elimination and Recovery Act of 2010 (IPERA) criteria that were applicable to their agencies. The OIGs for 10 agencies reported that their agencies did not satisfy at least one of the specified criteria, and 1 OIG did not issue a report, stating that its agency was not required to report improper payment data in its fiscal year 2013 performance accountability report. Fiscal year 2013 OIG IPERA reports showed that most CFO Act agencies reported on improper payments in their annual financial reports, conducted program risk assessments, and reported on actions to recover improper payments. However, the OIGs reported that many agencies did not meet their planned improper payment reduction targets or achieve and report gross improper payment error rates below 10 percent for each agency program or activity.

The most common area where OIGs found agencies noncompliant with the IPERA criteria was in publishing and meeting annual improper payment reduction targets, which 10 CFO Act agencies did not meet. The OIGs reported that factors affecting compliance with this requirement included the programs’ structure and continued challenges with supporting documentation. The second most common noncompliance finding reported by the OIGs—affecting 5 CFO Act agencies—was the inability to achieve and report improper payment error rates below 10 percent. Among these agencies, some reported as causes the complexities in the structure of the program and the lack of documentation, which prevented accurate authentication and verification of eligible recipients. According to OIG IPERA reports, agencies have shown overall improvement in reporting and addressing improper payments in the 3 years since IPERA was enacted. However, despite improvements in certain areas over this period, the OIGs for several agencies have not reported agency improvements in meeting planned reduction targets or lowering improper payment error rates to less than 10 percent.

Why GAO Did This Study

Improper payments—such as duplicate or erroneous payments, payments to ineligible recipients, or payments for ineligible services—have been a long-standing challenge of the federal government and have annually totaled billions of dollars. For fiscal year 2013, federal agencies reported an estimated $105.8 billion in improper payments. Fiscal year 2013 marked the third year of implementation of IPERA, which, among other things, requires that agencies perform risk assessments for all programs, publish corrective action plans, and meet planned reduction targets and error rates. IPERA also calls for executive agencies’ OIGs to annually determine whether their respective agencies are in compliance with six specific IPERA criteria. The Office of Management and Budget (OMB) has also asked the OIGs to assess compliance with one additional criterion, which calls for agencies to report on their efforts to recover improper payments.

In light of congressional interest in agency efforts to estimate, reduce, and recover improper payments, GAO performed its work under the authority of the Comptroller General to conduct evaluations to assist Congress with its oversight responsibilities. The objective of this review is to provide information on compliance with the seven criteria discussed above for the 24 agencies that are subject to the CFO Act, as reported in their OIGs’ IPERA reports.

Recommendations

GAO is not making any recommendations in this report. GAOprovided a draft of this report to the Director of OMB and the Inspectors General of all 24 CFO Act agencies. OMB provided written comments that highlighted initiatives to reduce improper payments, which it considers a key priority. All of the Offices of Inspectors General generally agreed with the information presented in this report. The Offices of Inspector General for the Departments of Education, Health and Human Services, Labor, and Veterans Affairs; the National Science Foundation; the Small Business Administration, and the Social Security Administration also provided technical comments that were incorporated, as appropriate.