Foreign Assistance: USAID Should Analyze Data on the Timeliness of Expenditures

Fast Facts

The U.S. Agency for International Development obligated (legally committed) $185 billion in FY 2009-2019 appropriations to spend on various projects.

Under its policies, USAID tries to spend its money before the end of the next fiscal year following the obligation. We consider spending after that to be delayed. For selected accounts funded in FY 2009-2017, we found as much as $23 billion in delayed spending. Analyzing delayed spending could help USAID identify excess funds, which could be used for other projects.

USAID does not review the timeliness of its spending. We recommended USAID routinely analyze the timeliness of its spending, and more.

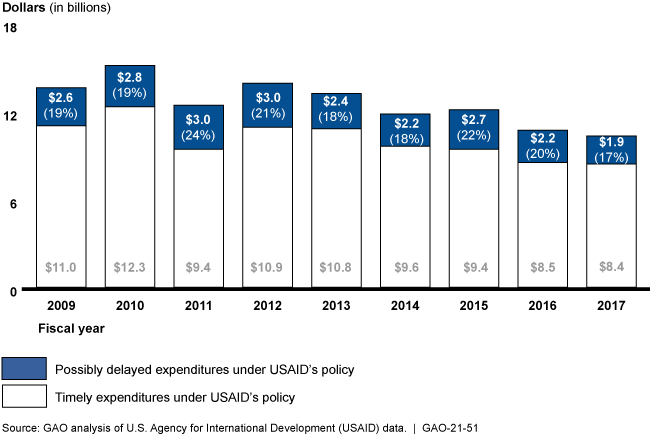

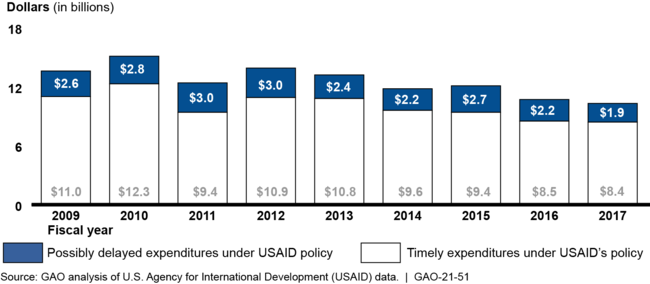

USAID's Timely or Possibly Delayed Expenditures for Selected Funds Appropriated in Fiscal Years 2009-2017, as of March 31, 2020

Highlights

What GAO Found

Almost $20 billion of the $185 billion (11 percent) that the U.S. Agency for International Development (USAID) obligated from funds appropriated in fiscal years 2009–2019 remained unliquidated (or not yet expended), as of March 31, 2020. Funds appropriated for Development Assistance (DA), Economic Support Fund (ESF), and Global Health Programs (GHP) made up about 78 percent of these unliquidated obligations (ULO).

GAO estimates that $23 billion in DA, ESF, and GHP obligations from funds appropriated in fiscal years 2009–2017 may have had delayed expenditures under USAID's forward funding policy (see fig.). Based on this policy, GAO defines delayed expenditures as those made after the end of the fiscal year following the fiscal year of obligation, if exceptions have not been granted. The actual amount of delayed expenditures may be less than $23 billion because, for example, this estimate likely includes projects with exceptions to USAID's forward funding policy.

USAID's Obligations from Development Assistance, Economic Support Fund, and Global Health Programs with Timely or Possibly Delayed Expenditures under USAID Policy in Fiscal Years 2009–2017, as of March 31, 2020

Note: GAO's analysis is based on USAID's data on subobligations, and obligations made outside of bilateral agreements. GAO defines these expenditures as delayed under USAID's forward funding policy, but the funds remain legally available for expenditure for the entire period of availability for obligation plus 5 fiscal years after the period of availability for obligation has expired, in accordance with the account closing law. See 31 U.S.C. §§ 1552(a) and 1553(a).

USAID has processes for monitoring ULOs but does not analyze data on what GAO refers to as the timeliness of expenditures under its policy. USAID monitors ULOs by completing quarterly financial reviews, among other activities. However, USAID does not analyze data to identify (1) expenditures that occur after the fiscal year following obligation and (2) exceptions to timelines established in its policy. Doing so could enable USAID to make more informed resource decisions.

USAID officials cited various factors that contribute to expenditure delays and possible excess ULOs, and USAID has taken some steps to manage them. USAID officials cited external factors such as political changes and internal factors such as reform initiatives, as contributing to increased ULOs. In response, USAID has launched an automated deobligation tool, among other steps taken.

Why GAO Did This Study

Congress provides foreign assistance funding through various appropriation accounts for international development projects. USAID is the primary U.S. agency responsible for implementing these projects and may have up to 11 fiscal years to expend its appropriations from certain accounts. USAID requires program managers to follow its forward funding policy, with some exceptions, and annually monitor ULOs to identify excess funds that may be eligible for deobligation and used for other purposes.

A Senate report provides for GAO to consult with the appropriations committee on a review of USAID's expenditure rates. This report examines (1) USAID data on ULOs for funds appropriated in fiscal years 2009–2019, (2) the extent to which expenditures in selected accounts met our definitions of timely or delayed under USAID policy, (3) the extent to which USAID monitors ULOs and the timeliness of expenditures, and (4) factors that USAID cites as contributing to expenditure delays and excess ULOs and steps taken to manage them. GAO analyzed financial data—primarily for DA, ESF, and GHP—reviewed USAID policies, and interviewed officials in Washington, D.C., and at three missions with large amounts of ULOs.

Recommendations

GAO is making three recommendations, including that USAID should routinely analyze data on (1) the timeliness of expenditures and (2) exceptions granted under its policy. USAID generally agreed with these recommendations.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| U.S. Agency for International Development | The Administrator of USAID should revise USAID's policy to clarify whether the date of obligation or subobligation should be used as the standard for calculating forward funding. (Recommendation 1) |

In December 2020, GAO reported that USAID's forward funding policy is unclear and has led to inconsistent implementation. Specifically, USAID's policy does not specify whether to use the obligation or subobligation date when calculating forward funding length (or the length of the pipeline in months) in the context of bilateral agreements. To help ensure that USAID officials are implementing this policy as intended and allow them to compare the timeliness of expenditures across missions and bureaus, GAO recommended that the USAID Administrator revise USAID's policy to clarify whether the date of obligation or subobligation should be used as the standard for calculating forward funding, and USAID concurred. In January 2021, USAID distributed an Executive Message, or general notice, and posted it on the agency's intranet for record purposes. The notice clarified that when USAID has a bilateral agreement with the government of a partner country, the forward funding policy applies to subobligations, not the original bilateral obligation. This clarification should make it easier for USAID to follow required procedures so that their forward funding does not exceed reasonable standards.

|

| U.S. Agency for International Development |

Priority Rec.

The Administrator of USAID should analyze financial data on the timeliness of expenditures. (Recommendation 2) |

In December 2020, GAO reported that USAID headquarters was not analyzing financial data to identify expenditures that occur after the end of the fiscal year following the fiscal year of obligation. GAO recommended that the USAID administrator should analyze data on the timeliness of expenditures and USAID concurred. In June 2021, USAID notified GAO that it had developed financial indicators to measure and analyze the timeliness of expenditures and incorporated these metrics into an agency level "organizational health index dashboard." According to USAID, this dashboard contains financial indicators including planned funding flows, which USAID has used to identify and manage expenditure and liquidation rates more effectively through improved visualization and routinized aggregate reporting. In January 2022, USAID provided GAO with a report on the timeliness of program expenditures, as of September 30, 2021. The report analyzes USAID's "pipeline"-that is, the difference between the amounts obligated and expended. The report includes information on USAID's pipeline in dollar amount and in months, potential excess pipeline, percentage of bilateral pipeline not yet sub-obligated, and pipeline by fund structure and obligation level. USAID said that this report will be issued quarterly and will be used to guide and assist the operating units to ensure they achieve and maintain timely expenditures and reasonable pipelines. Based on these steps taken by USAID, we are closing this recommendation as implemented.

|

| U.S. Agency for International Development | The Administrator of USAID should routinely gather and analyze data on exceptions granted to the timelines established in USAID's forward funding policy. (Recommendation 3) |

In December 2020, GAO reported that USAID headquarters was not analyzing financial data to identify expenditures that occur after the end of the fiscal year following the fiscal year of obligation. In addition, USAID lacked centralized aggregated information on the nature and extent of exceptions granted to the timelines established in its forward funding policy. GAO recommended that the USAID administrator routinely gather and analyze data on exceptions granted to the timelines established in USAID's forward funding policy, and USAID concurred. In September 2021, USAID provided GAO with a report showing their analysis of forward funding exceptions by operating units as of June 30, 2021. This report showed USAID's analysis of forward funding exceptions by categories such as top dollar exceptions, and exceptions by location, cause, fund, and funding year. USAID also provided GAO with the form it used to collect this data from operating units on a quarterly basis. Based on the steps taken by USAID, we are closing this recommendation as implemented.

|