Community Development Capital Initiative: Status of the Program and Financial Health of Remaining Participants

Highlights

What GAO Found

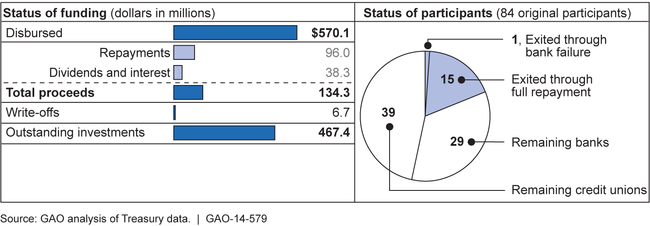

As of April 30, 2014, 82 percent of the Department of the Treasury's (Treasury) $570 million total investment in eligible banks and credit unions through the Community Development Capital Initiative (CDCI) was still outstanding. Sixteen institutions have exited the program, leaving 29 banks and 39 credit unions, respectively, in the program. Treasury had received repayments and investment income of $134.3 million, but has also recorded a $6.7 million write-off based on the failure of one participant's subsidiary. As of February 28, 2014 (most recent information available), Treasury estimated a lifetime cost of $80 million for CDCI, down from an estimated cost of $290 million in November 2010.

Status of Community Development Capital Initiative Funding and Participants, as of April 30, 2014

Note: Treasury invested in 84 institutions by purchasing preferred equity or subordinated debt.

Representatives of participant banks and credit unions GAO interviewed said that access—or lack thereof—to similar forms of capital was a key factor in institutions' willingness or ability to exit the program. They noted that CDCI continued to be one of the few sources of capital for small banks and credit unions. In addition, they listed program terms, such as the scheduled increase in the dividend or interest rate from 2 percent to 9 percent in 2018, as considerations. Treasury has not yet announced an exit strategy for CDCI but said it will consider the interests of the financial institutions and taxpayers as they consider options for winding down the program. For example, they noted that any strategy would need to take into account how the wind down of the program may impact the community development mission of the remaining participants.

The financial health of the remaining CDCI banks and credit unions is mixed. For example, few CDCI institutions have missed their dividend or interest payments to Treasury since 2010. The Federal Deposit Insurance Corporation and National Credit Union Administration (NCUA) had identified very few of the remaining banks and credit unions as exhibiting serious financial, operational, or managerial weaknesses as of March 2014. GAO's analysis of financial data found that banks remaining in CDCI tended to be more profitable, held stronger assets, and had higher capital and reserve levels when compared to non-CDCI banks that were eligible for the program but did not participate. However, remaining credit unions were less profitable, held slightly more poorly performing assets, and had lower capital levels and less protection against losses than non-CDCI credit unions that were eligible for the program but did not participate.

Why GAO Did This Study

Treasury established CDCI under the Troubled Asset Relief Program (TARP) in February 2010 to help banks and credit unions certified as Community Development Financial Institutions (CDFI) maintain their services to underserved communities in the aftermath of the 2007-2009 financial crisis. Treasury invested a total of $570 million in 84 eligible institutions by September 2010.

TARP's authorizing legislation mandates that GAO report every 60 days on TARP activities, including CDCI. This report examines (1) the financial status of CDCI; (2) factors affecting participants' decisions to remain in or leave the program and Treasury's exit strategy; and (3) the financial condition of institutions remaining in the program.

To assess the program's status, GAO reviewed Treasury reports on CDCI. GAO also used regulatory financial data to compare the financial condition of banks and credit unions remaining in CDCI with those that would have been eligible but did not participate. In addition, GAO interviewed staff from Treasury and NCUA, associations representing CDCI participants, and representatives of a nonprobability sample of CDFI banks and credit unions that participated in CDCI. GAO selected banks and credit unions based on asset size and geography.

GAO is making no recommendations in this report. In comments on a draft of this report, Treasury and NCUA concurred with our findings.

For more information, contact A. Nicole Clowers at (202) 512-8678 or clowersa@gao.gov.