Issue Summary

The U.S. retirement system, and the workers and retirees it was designed to help, face major challenges. The Social Security Old-Age and Survivors Insurance Trust Fund that supports retirement benefits is projected to be depleted in 2033, under current law, and continuing payroll taxes will be sufficient to pay only about an estimated 79% of scheduled benefits, according to the 2024 Social Security Trustees Report. Participation in employer-sponsored retirement plans hovers at about half of the total private-sector labor force, despite tax incentives and initiatives like automatic enrollment.

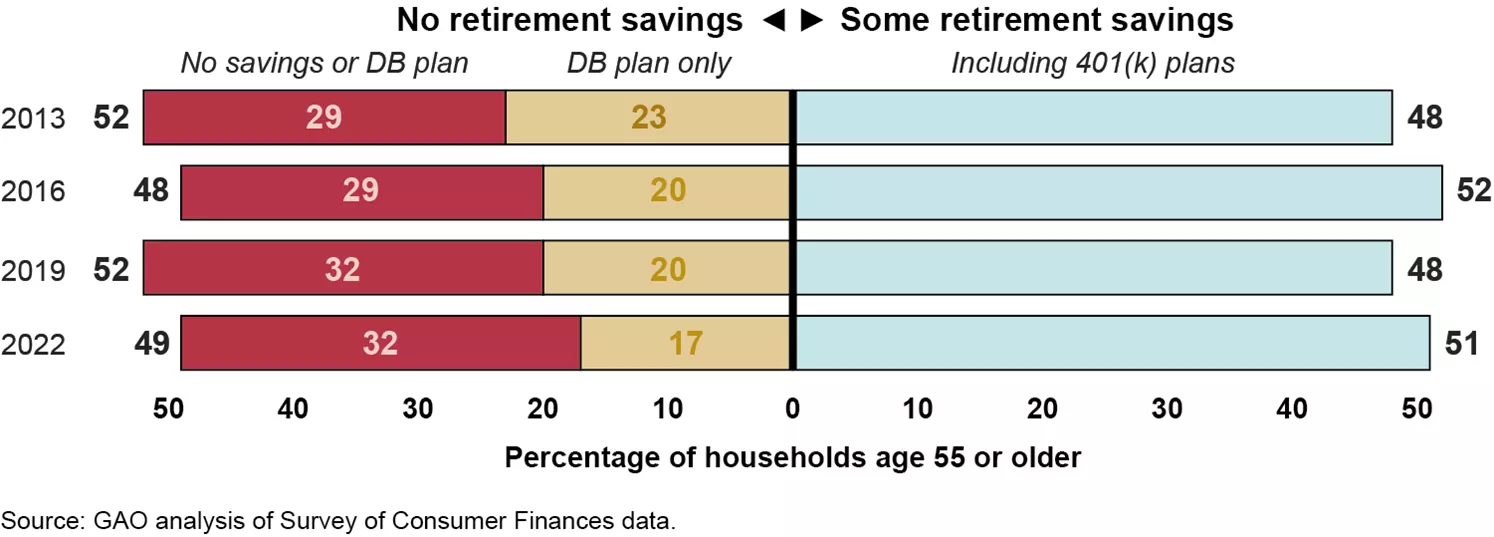

Even for those who do have access, traditional defined benefit pensions have become much less common as defined contribution plans, such as 401(k)s, have become the primary type of retirement plan. This shift has increased the risks and responsibilities for individuals in planning and managing their retirement. Yet research shows that many households are ill-equipped for this task and have little or no retirement savings.As of 2022, about half of households with a worker age 55 and older had no retirement savings, and 32% had no retirement savings or a defined benefit plan. Policymakers will need to consider how to best encourage expanded pension coverage, adequate and secure pension benefits, and more effective use of tax preferences to foster workers’ retirement security.

Retirement Resources for All Households Age 55 and Older, 2013-2022

Image

Note: Retirement savings include assets accrued in defined contribution plans, such as 401(k) plans, as well as individual retirement accounts (IRAs).

Policymakers and federal agencies—such as the Department of Labor (DOL)—can better help individuals ensure financial security for themselves and their families as they enter their retirement years.

For example:

- Social Security. Social Security is a major source of income for millions of retirees and other Americans. As program costs continue to exceed revenues, the fund that supports payments for retirees and their families is projected to be unable to pay full benefits in less than 10 years. The sooner policymakers address the financial challenges, the more gradually changes can be phased in. This would give workers more time to adjust to any changes and factor them into retirement plans. Additionally, being able to evaluate these changes for their effect on program finances, adequacy and equity, recent societal changes, and ease of implementation, as well as understanding the range of changes available, will help policymakers determine which changes best reflect our country’s goals for Social Security.

- 403(b) retirement plans. Millions of teachers and employees of tax-exempt organizations invest in 403(b) retirement plans. DOL provides educational materials to 403(b) plan sponsors and participants. However, the agency's website does not provide the same level of detailed information regarding 403(b) plans as it does for 401(k) plans. For example, the website does not contain targeted educational materials that could help participants understand 403(b) plan fees. Updated DOL information on 403(b) plans could help participants make more informed decisions.

- Fees for 401(k) plans. DOL requires 401(k) retirement plans to provide information on plan and investment fees to participants. Even small fees can significantly reduce retirement savings. But almost 40% of participants do not fully understand fee information, and 41% incorrectly believe that they pay no fees. DOL could help participants better understand and use fee information by, for example, requiring plans' fee disclosures to include fee benchmarks (an average fee among comparable funds) for comparing investment options. DOL could also take steps to provide information about fees' cumulative effects over time.

- 401(k) retirement plan tax notices. After separating from an employer, plan participants are sent a 402(f) notice that has some information on distribution options—like rolling over funds—and the tax consequences of cashing out funds from old plans. But only about a third of participants received this notice before they decided what to do with their retirement savings. About 80% of participants weren't aware of all their distribution options. To ensure plan participants receive easily-understandable information about all four distribution options and the associated tax consequences at the time they leave their job, DOL could help plans develop clear and concise communications to inform participants.

- Target date funds (TDFs). TDFs are the most widely used investment option in 401(k) plans and they allocate assets over time based on participants' targeted retirement dates. TDFs hold more in higher risk investments when participants are younger and shift to lower risk investments as they approach retirement. DOL developed guidance in 2010 for participants (and in 2013 for plan sponsors) to help them understand these and other key features and risks of TDFs. However, this guidance doesn’t include recent developments, such as the increase of TDFs structured as collective investment trusts. Without updated guidance, plans sponsors and participants may experience challenges identifying and understanding disclosures for collective investment trust TDFs. DOL should update its guidance with more recent information to help plan sponsors and participants better understand fund disclosures and risks.

- EBSA enforcement. The Employee Benefits Security Administration (EBSA) helps ensure that employer-sponsored retirement and group health plans comply with applicable federal requirements and that benefits are there for participants as promised. While EBSA’s responsibilities have increased in the last decade, its budget has generally remained flat. EBSA officials said the agency has several strategies to manage this—such as focusing resources on high-impact investigations and dedicating supplemental funds toward maintaining staff. But it doesn't have a clear and systematic process to reallocate resources. A clear, systematic, and thoroughly documented decision-making process could put EBSA in a better position to make informed decisions regarding resource reallocations due to changing circumstances.

- Conflicts of interest. The interests of financial professionals and retirement investors often conflict. For example, a financial professional may earn a commission from selling a product to a client—whether it makes money for the client or not. A review of 2,000 conflict disclosures and calls posing as potential clients to 75 financial professionals found many complex conflicts that can be difficult to explain. Additionally, mutual funds that paid financial professionals were associated with lower returns for investors. IRS should develop and implement a proactive process to identify prohibited transactions between IRA fiduciaries and IRAs and assess any associated excise tax.