Financial Infidelity: Removing Money from A Retirement Account Without A Spouse’s Knowledge or Consent

When you get married, you often think about how you’ll spend the rest of your life with your partner. And many married couples build that future through retirement savings. But what happens when one spouse removes money from retirement savings accounts without telling the other or getting their consent? It can have serious financial and personal consequences for them both.

Today’s WatchBlog post looks at our new report on this form of “financial infidelity” and the pros and cons of adding protections from it.

Image

What are the financial and personal consequences of removing funds without spousal knowledge or consent?

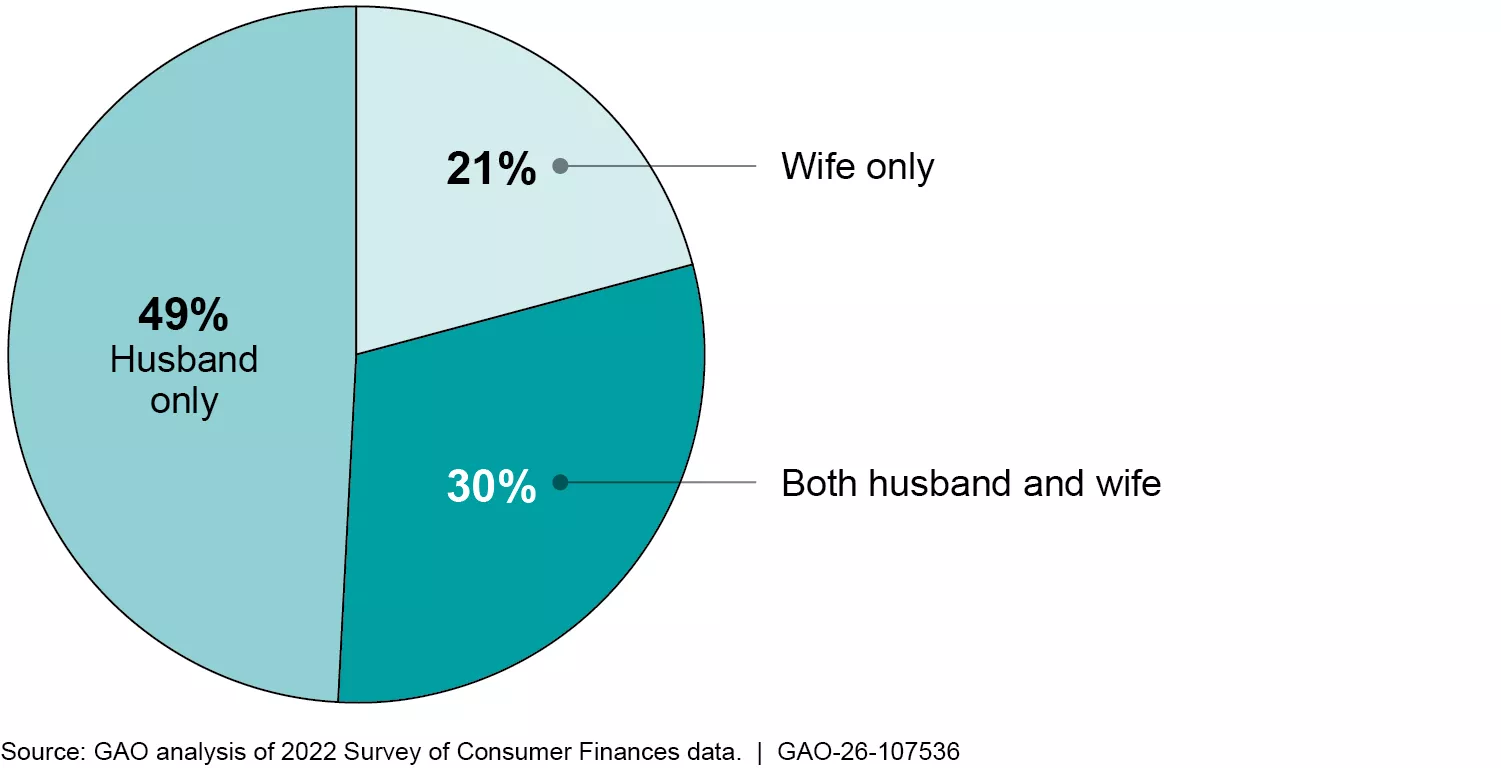

For many households, retirement accounts are their biggest financial asset outside of home property value. Often, retirement savings are built up through sacrifices from both parties. But the retirement account itself may be controlled or in the name of one spouse—because the account is created under that person’s employer.

How big is this problem? It’s not clear. Available data show that in any given year, about 11% of married households with 401(k)s took out money. And they typically took less than 10% of the balance.

What the data don’t tell us is whether spouses gave consent for the withdrawals or knew about it. Experts we spoke with said that removing funds without consent is likely uncommon. When it does happen, however, the fallout can be significant for everyone involved.

Younger spouses can lose decades of compound interest that they could have otherwise accrued. Older spouses maybe have fewer working years left to recoup lost funds. Those in lower-income households have less opportunity to replace savings—especially if they have little money left after paying bills.

And women may be more vulnerable. Women are more likely to work in part-time jobs that do not offer retirement plans. Women are also more likely to pause their careers to take care of family members—contributing less toward retirement accounts and relying on a spouse to save. As a result, married women may be more reliant on their spouse’s retirement savings and disproportionately subjected to financial hardship when funds are removed without them knowing.

Snapshot of 401(k)-type Account Ownership for Married Couples

Image

Why does this happen? The reasons for financial infidelity vary. The reasons aren’t always malicious—sometimes couples agree about what to buy but not how to pay for it. But other cases can involve intentional deceit. We interviewed people affected by these situations. They told us about everything from spouses removing assets in anticipation of a divorce, or to conceal expenses related to an extramarital affair, addiction, or hidden debt. One woman said she learned that her husband had been liquidating his retirement account for years while pretending to be employed.

While the reasons varied, the end results in the most severe cases were similar—major life changes and emotional tolls.

Major life changes. We interviewed several people impacted by these situations. Two shared that they had to delay retirement when a spouse took out funds. One legal representative told us about a spouse who removed more than half a million dollars from a 401(k) account without consent—impacting both spouses. Another shared that a client experienced homelessness after her husband drained his 401(k) account.

Emotional tolls. Several spouses told us they felt lied to and betrayed, which led to emotional hardships, marital discord, and divorce in some cases. Discovering the deceit can erode trust in the marriage. For example, a legal spokesperson and a spouse said that withdrawing funds without consent is a form of cheating.

What protections are there already, and what’s the downside of adding more?

There are some protections for couples. For example, federal laws require written spousal consent to remove funds or take loans from most defined benefit plans (pensions) in the private sector. This same protection extends to savings under the federal employees’ Thrift Savings Plan. But federal laws do not offer the same spousal protections for most private defined contribution plans (like 401(k)s).

Requiring spousal consent for all 401(k)s could:

- Help improve transparency by ensuring all spouses are aware of loans and withdrawals that ultimately affect their retirement security,

- Allow a spouse to withhold consent for removing any funds

- Help nonworking spouses who are unaware of their spouse’s account balances

But additional requirements could come with some potential drawbacks too. These include increasing administrative burdens and costs for retirement plans, and extending how long it could take to withdraw funds. For example,

- Plan sponsors may need additional staff to manage transactions or verify consent. These costs may then be passed on to account holders.

- Account holders may not be able to access their money as quickly if plans need additional processing time to determine marital status or get notarized consent from a spouse. For example, two companies that manage retirement plans told us that processing a request with spousal consent may take longer. Specifically, they said it could take a week or more compared to 2-3 days for transactions without it.

- And some plans expressed concerns about collecting marital status information and handling cases related to domestic violence, among other issues.

Our full report looks at these and other concerns—both for creating greater protections for spouses and their drawbacks. Learn more about this issue by reading our new report.

- GAO’s fact-based, nonpartisan information helps Congress and federal agencies improve government. The WatchBlog lets us contextualize GAO’s work a little more for the public. Check out more of our posts at GAO.gov/blog.

- Got a comment, question? Email us at blog@gao.gov.

GAO Contacts

Related Products

GAO's mission is to provide Congress with fact-based, nonpartisan information that can help improve federal government performance and ensure accountability for the benefit of the American people. GAO launched its WatchBlog in January, 2014, as part of its continuing effort to reach its audiences—Congress and the American people—where they are currently looking for information.

The blog format allows GAO to provide a little more context about its work than it can offer on its other social media platforms. Posts will tie GAO work to current events and the news; show how GAO’s work is affecting agencies or legislation; highlight reports, testimonies, and issue areas where GAO does work; and provide information about GAO itself, among other things.

Please send any feedback on GAO's WatchBlog to blog@gao.gov.