Banking at the Border, Money Laundering, and “Derisking”

Banks are an important line of defense for fighting financial crimes. Banks and other financial institutions are subject to the Bank Secrecy Act, which helps federal law enforcement detect and deter the use of financial institutions for money laundering and other criminal activities such as financing terrorism. Money that crosses an international boundary may be of particular interest to authorities.

There can be unintended effects due to the law, as well. In some cases, banks may become so concerned that they will run afoul of the rules that they “derisk” their operations—they deny or restrict services to legitimate customers.

Today’s WatchBlog takes a look at our recent reports dealing with some of the issues surrounding banking in the Southwest border and international money transfers.

Who is losing banking access and why?

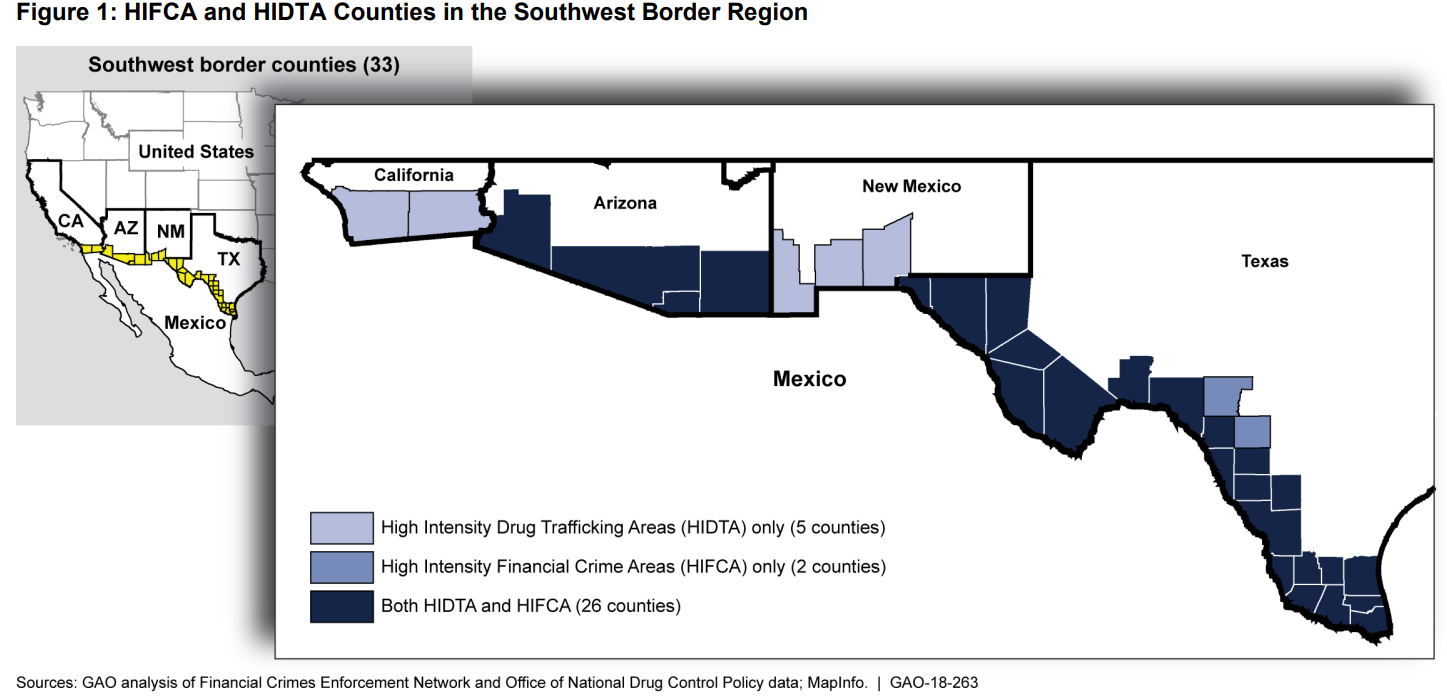

The Southwest border region of the United States is considered a high-risk area for money laundering activity because of a high volume of cash and cross-border transactions.

As a result, as our recent report noted, U.S. banks in the region tend to more intensively monitor accounts and investigate suspicious activities than in other parts of the country.

According to a GAO survey, an estimated 80% of Southwest border banks terminated accounts over the risk of noncompliance with the Bank Secrecy Act and related regulations. Cash-intensive small businesses were among the most common business customers for which banks reported such terminations.

Further, according to our survey, an estimated 80% of banks limited or did not offer accounts to customers that are considered high risk for money laundering because the customers drew heightened regulatory oversight. This behavior suggests the banks are derisking.

Remittances: How much money is transferred, where does it go, and how does it get there?

The United States is the largest source of remittances (transfer of funds from people in the United States to family and friends abroad, especially in poor countries), with an estimated $67 billion sent globally in 2016, according to the World Bank.

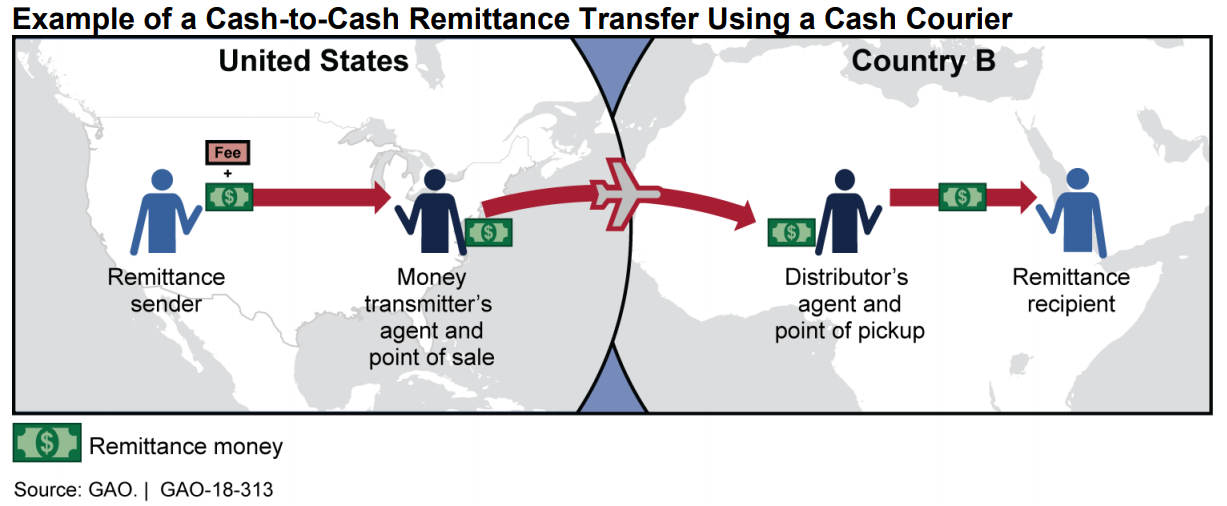

Historically, due to convenience, cost, familiarity, or tradition, many consumers have chosen to send remittances through money transmitter businesses, which facilitate global movement of money. Money transmitters generally use banks for their operations, including to transfer money internationally.

In a recent report, all 12 money transmitters we interviewed (serving Haiti, Liberia, Nepal, and Somalia) reported loss of banking access in the last 10 years. As a result, 9 of the 12 money transmitters had started using channels outside the banking system, such as cash couriers, to move funds domestically and, in the case of Somalia, internationally.

Transfer of payments through non-banking channels is problematic because these channels are generally less transparent than banking channels and thus more susceptible to the risk of money laundering and terrorism financing.

Most of the bank representatives we interviewed expressed concerns regarding account holders who are money transmitters because they tend to be low-profit, high-risk clients.

In addition, some bank representatives expressed concern that violations of anti-money laundering and terrorism financing guidelines by a money transmitter’s customer may result in fines for the bank, even when the bank has conducted enhanced due diligence and monitoring of transactions.

What is the U.S. government doing about these concerns?

While U.S. regulators have issued guidance to banks indicating that they should not terminate accounts without a case-by-case assessment, several banks we contacted remain apprehensive and are reluctant to incur additional costs for low-profit customers such as money transmitters.

As a result, we recommended that federal banking regulators conduct a review of Bank Secrecy Act regulations, focusing on how banks' regulatory concerns may be influencing their willingness to provide services. Additionally, we recommended that Treasury assess the risks of remittance transfers through non-banking channels, which are harder to monitor for criminal activity.

- Comments on GAO’s WatchBlog? Contact blog@gao.gov.

GAO Contacts

Related Products

GAO's mission is to provide Congress with fact-based, nonpartisan information that can help improve federal government performance and ensure accountability for the benefit of the American people. GAO launched its WatchBlog in January, 2014, as part of its continuing effort to reach its audiences—Congress and the American people—where they are currently looking for information.

The blog format allows GAO to provide a little more context about its work than it can offer on its other social media platforms. Posts will tie GAO work to current events and the news; show how GAO’s work is affecting agencies or legislation; highlight reports, testimonies, and issue areas where GAO does work; and provide information about GAO itself, among other things.

Please send any feedback on GAO's WatchBlog to blog@gao.gov.