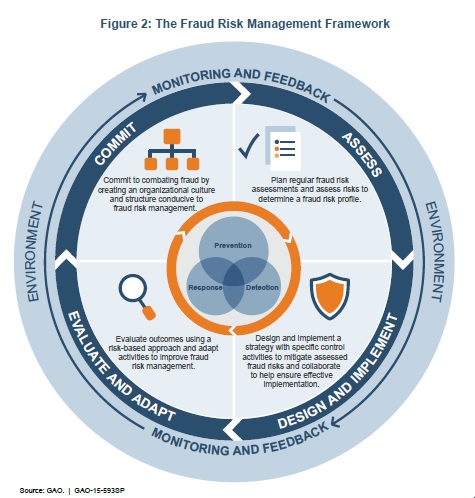

Our New Framework for Managing Fraud Risk

- Prevent fraud. Stopping fraud before it happens, by strategically evaluating risks and closing vulnerabilities, is much more cost effective than simply trying to recoup funds lost to fraud (say, disability benefits already paid to a fraudster).

- Detect fraud. However, fraud can occur in even the best-designed programs. Therefore, it’s important to continuously monitor potential fraudulent activity and use data analysis and other tools to uncover existing fraud and deter future schemes.

- Respond to fraud. Finally, investigating potential fraud and imposing fines, disciplinary actions, and prosecutions not only punishes fraudsters, but discourages future nefarious activity. Programs should also use the results of investigations and other findings to enhance applicant screenings and fraud indicators.

(Excerpted from GAO-15-593SP)

Easier said than done? These steps can help. Of course, fraud management doesn’t happen in isolation. A program’s larger environment, including its budget constraints and other risk-management initiatives, can affect how managers address fraud. The framework outlines clear steps federal managers can take to perform the above core activities successfully within their existing environments:- Demonstrate commitment by making sure efforts to fight fraud have executive sponsorship, are part of the organizational culture, and are led by a designated entity within the program office.

- Tailor fraud risk assessments to each program, involve relevant stakeholders, and determine risk tolerances.

- Implement a strategy focusing on prevention, developing a fraud response plan, and considering the costs and benefits of related controls.

- Evaluate outcomes based on risk and adapt activities based on data analysis and real-time monitoring of fraud trends.

- Questions on the content of this post? Contact Steve Lord at lords@gao.gov.

- Comments on GAO’s WatchBlog? Contact blog@gao.gov.

GAO's mission is to provide Congress with fact-based, nonpartisan information that can help improve federal government performance and ensure accountability for the benefit of the American people. GAO launched its WatchBlog in January, 2014, as part of its continuing effort to reach its audiences—Congress and the American people—where they are currently looking for information.

The blog format allows GAO to provide a little more context about its work than it can offer on its other social media platforms. Posts will tie GAO work to current events and the news; show how GAO’s work is affecting agencies or legislation; highlight reports, testimonies, and issue areas where GAO does work; and provide information about GAO itself, among other things.

Please send any feedback on GAO's WatchBlog to blog@gao.gov.