Opportunity Zones: Census Tract Designations, Investment Activities, and IRS Challenges Ensuring Taxpayer Compliance

Fast Facts

Congress created the Opportunity Zones incentive to spur investment in distressed communities. Taxpayers who invest in Qualified Opportunity Funds—which invest in zones—can get significant tax benefits.

According to IRS, over 6,000 of these funds invested about $29 billion in Opportunity Zones through 2019. The incentive attracted investment in housing, renewable energy businesses, and other projects.

IRS developed plans to ensure these funds comply with requirements. But its plans depend on data that isn't readily accessible—which could make it hard for IRS to find investors who aren't following the rules. We recommended addressing this risk.

Example of development in an Opportunity Zone in Washington, D.C.

Highlights

What GAO Found

The 2017 law commonly known as the Tax Cuts and Jobs Act created a tax incentive that gave governors discretion to nominate generally up to 25 percent of their states' low-income census tracts as special investment areas called Opportunity Zones. The U.S. Department of the Treasury then verified eligibility and designated the nominated tracts. GAO found that on average, the selected tracts had higher poverty and a greater share of non-White populations than eligible, but not selected, tracts. These differences were statistically significant.

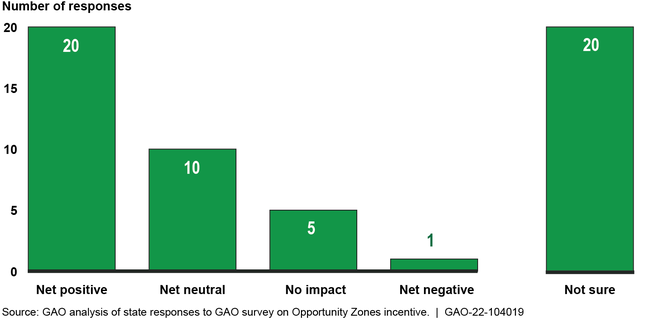

Most state government officials were aware of at least some Opportunity Zone investments but had differing views of the tax incentive's effect so far.

State Respondents' Views on Overall Impact of the Opportunity Zones Tax Incentive

Note: GAO surveyed government officials from the 50 states, Washington, D.C., and the five U.S. territories—American Samoa, Guam, the Commonwealth of the Northern Mariana Islands, Puerto Rico, and the U.S. Virgin Islands—and received 56 responses.

Based on case studies of Qualified Opportunity Funds—investment vehicles organized for investing in Opportunity Zones—the tax incentive attracted investment in a variety of projects, including multifamily housing, self-storage facilities, and renewable energy businesses. According to survey responses and other sources, most projects are real-estate focused.

Through 2019, more than 6,000 Qualified Opportunity Funds had invested about $29 billion, based on partial data from the Internal Revenue Service (IRS).

IRS developed plans to ensure Qualified Opportunity Funds and investors are complying with the tax incentive's requirements; however, IRS faces challenges in implementing these plans. Specifically, the plans depend on data that are not readily available for analysis. In addition, funds have attracted investments from high-wealth individuals, and some funds are organized as partnerships with hundreds of investors. IRS considers both of these groups to be high risk for tax noncompliance generally. However, IRS has not researched potential compliance risks these groups pose for this tax incentive. As a result, IRS may be unable to effectively direct compliance efforts.

Why GAO Did This Study

Congress created the Opportunity Zones tax incentive to spur investments in distressed communities. Taxpayers who invest in Qualified Opportunity Funds—that then invest in qualified property or businesses—could receive significant tax-related benefits. Funds and their investors generally must invest in Opportunity Zones for a minimum number of years and report information annually to receive tax benefits and avoid penalties. IRS administers and ensures compliance with these rules. GAO was asked to review implementation and use of this tax incentive.

This report describes the process for designating census tracts as Opportunity Zones and compares characteristics of designated and non-designated tracts; describes Qualified Opportunity Funds' experiences with and states' views on the tax incentive; analyzes available IRS data; and evaluates IRS's taxpayer compliance plans, among other objectives.

GAO analyzed census data on tracts designated and not designated as Opportunity Zones, analyzed data from a non-generalizable sample of 18 Qualified Opportunity Funds, and surveyed state officials. GAO also reviewed IRS documentation, including a compliance plan, and met with Treasury and IRS officials.

Recommendations

GAO is recommending that IRS (1) address risks caused by limited data availability, and (2) research compliance risks of high-wealth investors and large partnership Qualified Opportunity Funds. IRS generally agreed pending available resources.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Internal Revenue Service | The Commissioner of Internal Revenue should direct the Small Business and Self-Employed division to assess the risks that data limitations pose to its Opportunity Zones tax incentive compliance plan and take steps to mitigate those risks. (Recommendation 1) |

Open – Partially Addressed

IRS agreed with our recommendation and as of November 2022 had updated its compliance plan to mitigate the risks posed by data limitations. In February 2023, IRS provided us information on other actions being considered to mitigate compliance concerns such as developing further guidance to IRS examiners. IRS also said it was assessing the viability of compiling comprehensive lists of Opportunity Zone funds and investors. Continuing to assess the risks that data limitations pose to its Opportunity Zones compliance plan and taking steps to mitigate those risks, as we recommended, will help IRS identify and address taxpayer noncompliance.

|

| Internal Revenue Service | The Commissioner of Internal Revenue should direct the Small Business and Self-Employed and Large Business and International divisions to research compliance risks posed by high-wealth individuals and large partnerships that are using the Opportunity Zones tax incentive and take appropriate steps to address the risks identified. (Recommendation 2) |

Closed – Implemented

IRS conducted research on high-wealth individuals and large partnerships that participated in Opportunity Zones from 2018 to 2021 to identify potential compliance risks. Based on the results of that research, IRS SB/SE officials determined in September 2023 that existing examinations were sufficient to understand the compliance risks and that no additional risks were identified. By conducting this research for any previously unidentified compliance risks posed by high-wealth and large partnerships, IRS was able to determine additional actions are not needed to ensure taxpayer compliance.

|