Federal Student Loans: Actions Needed to Improve Oversight of Schools' Default Rates

Highlights

What GAO Found

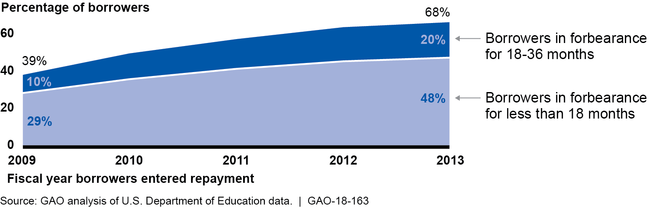

According to federal law, schools may lose their ability to participate in federal student aid programs if a significant percentage of their borrowers default on their student loans within the first 3 years of repayment. To manage these 3-year default rates, some schools hired consultants that encouraged borrowers with past-due payments to put their loans in forbearance, an option that allows borrowers to temporarily postpone payments. While forbearance can help borrowers avoid default in the short-term, it increases their costs over time and reduces the usefulness of the 3-year default rate as a tool to hold schools accountable. At five of the nine selected default management consultants (that served about 800 of 1,300 schools), GAO identified examples when forbearance was encouraged over other potentially more beneficial options for helping borrowers avoid default, such as repayment plans that base monthly payments on income. Based on a review of consultants' communications, GAO found four of these consultants provided inaccurate or incomplete information to borrowers about their repayment options in some instances. A typical borrower with $30,000 in loans who spends the first 3 years of repayment in forbearance would pay an additional $6,742 in interest, a 17 percent increase. GAO's analysis of Department of Education (Education) data found that 68 percent of borrowers who began repaying their loans in 2013 had loans in forbearance for some portion of the first 3 years, including 20 percent that had loans in forbearance for 18 months or more (see figure). Borrowers in long-term forbearance defaulted more often in the fourth year of repayment, when schools are not accountable for defaults, suggesting it may have delayed—not prevented—default. Statutory changes to strengthen schools' accountability for defaults could help further protect borrowers and taxpayers.

Borrowers in Forbearance during the First 3 Years of Repayment, 2009 to 2013

Education's ability to oversee the strategies that schools and their consultants use to manage their default rates is limited. Education's strategic plan calls for protecting borrowers from unfair and deceptive practices; however, Education states it does not have explicit statutory authority to require that the information schools or their consultants provide to borrowers after they leave school regarding loan repayment and postponement be accurate and complete. As a result, schools and consultants may not always provide accurate and complete information to borrowers. Further, Education does not report the number of schools sanctioned for high default rates, which limits transparency about the 3-year default rate's usefulness for Congress and the public.

Why GAO Did This Study

As of September 2017, $149 billion of nearly $1.4 trillion in outstanding federal student loan debt was in default. GAO was asked to examine schools' strategies to prevent students from defaulting and Education's oversight of these efforts.

This report examines (1) how schools work with borrowers to manage default rates and how these strategies affect borrowers and schools' accountability for defaults; and (2) the extent to which Education oversees the strategies schools and their default management consultants use to manage schools' default rates. GAO analyzed Education data on student loans that entered repayment from fiscal years 2009–2013, the most recent data at the time of this analysis; reviewed documentation from Education and a nongeneralizable sample of nine default management consultants selected based on the number of schools served (about 1,300 schools as of March 2017); reviewed relevant federal laws and regulations; and interviewed Education officials.

Recommendations

Congress should consider strengthening schools' accountability for student loan defaults and requiring that the information schools and consultants provide to borrowers about loan repayment and postponement options be accurate and complete. GAO recommends that Education increase transparency of reporting on default rate sanctions. Education agreed with our recommendation.

Matter for Congressional Consideration

| Matter | Status | Comments |

|---|---|---|

| Congress should consider strengthening schools' accountability for student loan defaults, for example, by 1) revising the cohort default rate (CDR) calculation to account for the effect of borrowers spending long periods of time in forbearance during the 3-year CDR period, 2) specifying additional accountability measures to complement the CDR, for example, a repayment rate, or 3) replacing the CDR with a different accountability measure. (Matter 1) |

Open

|

As of February 2024, no legislation has been enacted and relevant legislation has not been introduced in the 118th Congress. In the 117th Congress, legislation was introduced to revise the cohort default rate calculation and add new accountability measures to complement the CDR, as we suggested in our report. The Acting on the Annual Duplication Report Act of 2021 (S. 2782) and Accountability in Student Loan Data Act of 2022 (H.R. 7727) included provisions that, if enacted, would revise the cohort default rate calculation to change how borrowers who spend long periods in forbearance are accounted for in the calculation. The Protect Student Borrowers Act of 2022 (S. 5065), included provisions that, if enacted, would hold colleges accountable for some of the costs of student loan defaults if their cohort default rate or repayment rate exceeds specified thresholds. We will continue to monitor congressional action. Statutory changes to strengthen the cohort default rate, such as by changing how borrowers in forbearance are accounted for or adding new accountability measures, could help further protect borrowers and the billions of dollars of federal student aid the government distributes each year. |

| Congress should consider requiring that schools and default management consultants that choose to contact borrowers about their federal student loan repayment and postponement options after they leave school present them with accurate and complete information. (Matter 2) |

Open

|

As of March 2024, no legislation has been enacted and relevant legislation has not been introduced in the 118th Congress. The Transparency in Student Loan Consultation Act of 2018 (H.R. 6473), introduced in the 115th Congress, included provisions to require schools and their default management consultants to provide borrowers with information that is accurate and complete. We are continuing to monitor congressional action. |

Recommendations for Executive Action

| Agency Affected | Recommendation | Status Sort descending |

|---|---|---|

| Office of Federal Student Aid | The Chief Operating Officer of the Office of Federal Student Aid should increase the transparency of the data Education publicly reports on school sanctions by adding information on the number of schools that are annually sanctioned and the frequency and success rate of appeals. (Recommendation 1) |

Closed – Implemented

Education agreed with this recommendation. In March 2020, following the conclusion of the appeal cycle for fiscal year 2016 Cohort Default Rates, Education posted additional information on its website indicating which schools subject to sanctions submitted appeals and the disposition of the appeals, including whether schools withdrew from the Title IV program.

|