Columbia Class Submarine: Overly Optimistic Cost Estimate Will Likely Lead to Budget Increases

Fast Facts

The Navy will start taking certain submarines out of service in 2027 and is relying on its new Columbia class submarines to replace them. The schedule for construction and delivery of the first submarine is aggressive and leaves little room for error.

However, the Navy's cost estimate to construct 12 Columbia class submarines—$115 billion—is not realistic because it is based on several overly optimistic assumptions, such as the amount of labor needed for construction.

We made 3 recommendations to help the Navy calculate a more realistic cost estimate.

Design Rendering of the Columbia Class Submarine

Submarine on the water's surface

Highlights

What GAO Found

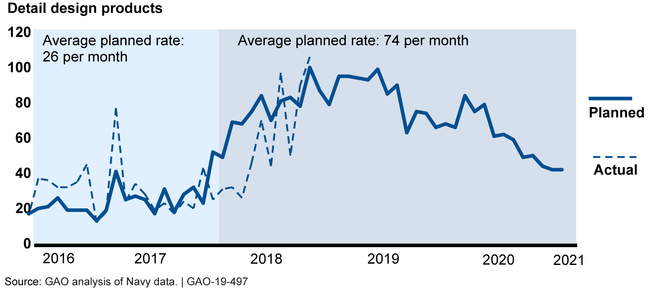

The Navy's goal is to complete a significant amount of the Columbia class submarine's design—83 percent—before lead submarine construction begins in October 2020. The Navy established this goal based on lessons learned from another submarine program in an effort to help mitigate its aggressive construction schedule. Achieving this goal may prove to be challenging as the shipbuilder has to use a new design tool to complete an increasingly higher volume of complex design products (see figure). The shipbuilder has hired additional designers to improve its design progress. The Navy also plans to start advance construction of components in each major section of the submarine, beginning in fiscal year 2019, when less of the design will be complete.

Shipbuilder's Workload Increases as Design Efforts Continue

The Navy's $115 billion procurement cost estimate is not reliable partly because it is based on overly optimistic assumptions about the labor hours needed to construct the submarines. While the Navy analyzed cost risks, it did not include margin in its estimate for likely cost overruns. The Navy told us it will continue to update its lead submarine cost estimate, but an independent assessment of the estimate may not be complete in time to inform the Navy's 2021 budget request to Congress to purchase the lead submarine. Without these reviews, the cost estimate—and, consequently, the budget—may be unrealistic. A reliable cost estimate is especially important for a program of this size and complexity to help ensure that its budget is sufficient to execute the program as planned.

The Navy is using the congressionally-authorized National Sea-Based Deterrence Fund to construct the Columbia class. The Fund allows the Navy to purchase material and start construction early on multiple submarines prior to receiving congressional authorization and funding for submarine construction. The Navy anticipates achieving savings through use of the Fund, such as buying certain components early and in bulk, but did not include the savings in its cost estimate. The Navy may have overestimated its savings as higher than those historically achieved by other such programs. Without an updated cost estimate and cost risk analysis, including a realistic estimate of savings, the fiscal year 2021 budget request may not reflect funding needed to construct the submarine.

Why GAO Did This Study

The Navy has identified the Columbia class submarine program as its top acquisition priority. It plans to invest over $100 billion to develop and purchase 12 nuclear-powered ballistic missile submarines to replace aging Ohio class submarines by 2031.

The National Defense Authorization Act for Fiscal Year 2018 and House Report 115-200 included provisions that GAO review the status of the program. This report examines (1) the Navy's progress and challenges, if any, in meeting design goals and preparing for lead submarine construction; (2) the reliability of the Navy's cost estimate; and (3) how the Navy is implementing a special fund and associated authorities to construct Columbia class submarines.

GAO reviewed Navy and shipbuilder progress reports, program schedules, and construction plans. GAO assessed the Navy's cost estimate and compared it to best practices for cost estimating. GAO also reviewed certain Navy funding and acquisition authorities and interviewed program officials.

This is a public version of a sensitive report that GAO issued in March 2019. Information that the Department of Defense (DOD) deemed sensitive has been omitted.

Recommendations

GAO is making three recommendations: that the Navy update the lead submarine cost estimate with cost risk analysis using current cost data, develop a realistic estimate of savings from use of the Fund's authorities, and use this updated cost estimate to inform its budget request for lead submarine construction. DOD concurred with GAO's recommendations.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Department of the Navy | The Secretary of the Navy should direct NAVSEA to incorporate current cost and program data and an updated cost risk analysis in its planned update of the Columbia class lead submarine cost estimate. (Recommendation 1) |

Closed – Implemented

DOD concurred with this recommendation, stating that the Columbia Class Program cost estimate was planned to be updated to support the lead ship authorization Decision Acquisition Board in 2020. In July 2020, prior to the Defense Acquisition Board meeting, the Navy provided a briefing on program costs that reflected NAVSEA's updated cost estimate, which included updated cost and program data, and cost risk analysis.

|

| Department of the Navy | The Secretary of the Navy should direct NAVSEA to develop a realistic and well-documented estimate of savings from use of the authorities associated with the Fund and incorporate the savings associated with the lead submarine into the Columbia lead submarine cost estimate. (Recommendation 2) |

Closed – Implemented

DOD agreed with this recommendation, stating that the updated Columbia Class Program cost estimate would incorporate estimated savings from use of the authorities associated with the fund and savings associated with the Columbia lead submarine cost estimate. In August 2020, Navy officials indicated that NAVSEA updated the Columbia lead submarine cost estimate to include updates to the estimate of savings from the use of the authorities associated with the Fund. In November 2021, the Navy provided additional documentation that includes the basis of savings for the Fund and incorporates updated cost and program data.

|

| Department of the Navy | The Secretary of the Navy should direct the Columbia class program office to update the lead submarine cost estimate and cost risk analysis prior to requesting funds for lead submarine construction. (Recommendation 3) |

Closed – Not Implemented

DOD concurred with this recommendation, stating that the lead submarine cost estimate and cost risk analysis will be updated to support the lead ship authorization Decision Acquisition Board in 2020. In August 2020, Navy officials indicated that NAVSEA updated the Columbia lead submarine cost estimate. However, this estimate was completed after funding was requested for lead submarine construction. While the Office of Cost Assessment and Program Evaluation conducted an assessment of this estimate in the summer of 2020, the assessment was too late to inform the Navy's initial funding request for lead submarine construction.

|