National Science Foundation: Actions Needed to Improve Oversight of Indirect Costs for Research

Fast Facts

The National Science Foundation awards billions of dollars annually to K-12 schools, universities, and others to support scientific research and education. NSF reimburses these organizations for direct costs, such as researchers' salaries and equipment, and has a formula for funding a portion of awardees' indirect costs like rent and utilities.

We found that NSF does not consistently take steps to ensure it pays no more than its fair share of indirect costs, which could unnecessarily limit the amount of funds available for research.

We made three recommendations to NSF to help it improve its guidance for setting indirect cost rates.

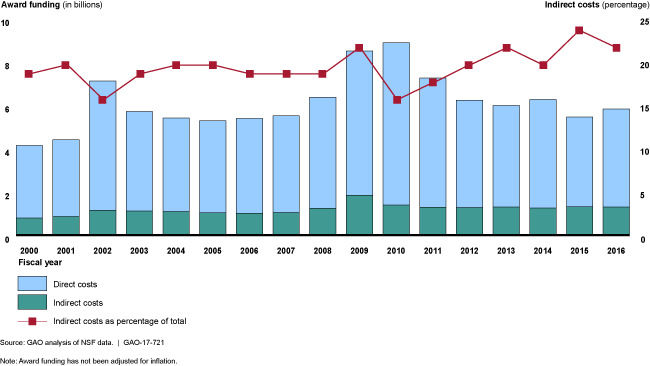

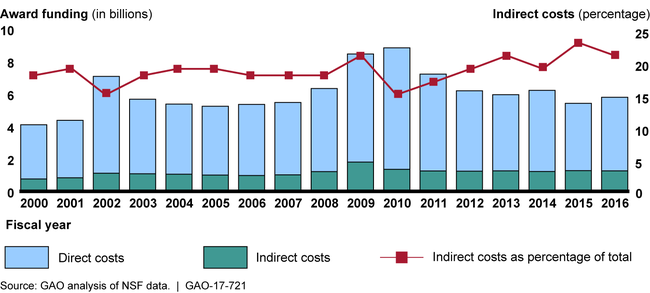

Indirect costs for National Science Foundation awards varied from 16 to 24 percent of total annual award funding, Fiscal Years 2000-2016

Graphic showing annual direct and indirect costs budgeted for the National Science Foundation awards.

Highlights

What GAO Found

For National Science Foundation (NSF) awards during fiscal years 2000 through 2016, budgeted indirect costs varied from 16 to 24 percent of the total annual amounts the agency awarded. The percentage fluctuated during this period, though this percentage generally has increased since reaching a low point in 2010. The variation from year-to-year was based on various factors such as by the types of activities supported by the awards and the types of awardee organizations receiving the awards.

Annual Direct and Indirect Costs Budgeted on National Science Foundation (NSF) Awards, Fiscal Years 2000–2016

Note: Award funding has not been adjusted for inflation.

NSF has developed internal guidance for setting indirect cost rates (ICR) but has not consistently implemented this guidance and has not included certain details and procedures, in particular:

NSF has not consistently implemented its guidance because it has not yet required NSF staff to follow aspects of its guidance, such as using a documentation checklist that NSF developed to verify that an awardee's ICR proposal package is complete.

NSF did not include details on supervisory activities, such as the criteria to be used by the supervisor of the ICR process for assessing an ICR proposal's risk level and mitigating risks at each level.

NSF did not include certain procedures, such as for implementing new provisions of federal guidance on setting ICRs.

NSF officials described ways that staff implement procedures even though the procedures are not fully detailed or included in guidance. Nevertheless, with complete guidance that includes the missing details and procedures and that is consistently followed, NSF could better ensure that ICRs are set consistently and in accordance with federal guidance on indirect costs and with federal internal control standards.

Why GAO Did This Study

NSF awards billions of dollars to institutions of higher education (universities), K-12 school systems, industry, science associations, and other organizations to promote scientific progress by supporting research and education.

NSF reimburses awardees for direct and indirect costs incurred for most awards. Direct costs, such as salaries and equipment, can be attributed to a specific project that receives an NSF award. Indirect costs, such as the costs of operating and maintaining facilities, are not directly attributable to a specific project but are necessary for the general operation of an awardee's organization. For certain organizations, NSF also negotiates ICR agreements, which are then used for calculating reimbursements for indirect costs. ICR negotiations and reimbursements are to be done in accordance with federal guidance and regulation and NSF policy.

GAO was asked to review the amount of NSF funding for indirect costs and NSF's negotiation of ICRs. This report examines (1) what is known about indirect costs on NSF awards over time, and (2) the extent to which NSF has implemented guidance for setting ICRs for organizations over which it has cognizance. GAO reviewed relevant regulations, guidance, and agency documents; analyzed budget data and a nongeneralizable sample of nine ICR files from fiscal year 2016 selected based on award funding; and interviewed NSF officials.

Recommendations

GAO recommends that NSF take three actions to improve its guidance for setting ICRs, including adding certain details and procedures. NSF concurred with GAO's recommendations and described plans to address them.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| National Science Foundation | The Director of NSF should require staff to follow written internal guidance for (1) using tools and templates NSF has developed for the process for setting indirect cost rates and (2) updating the agency's database to reflect the status of awardees for which NSF has cognizance and of indirect cost rate proposals. (Recommendation 1) |

NSF issued revised guidance for setting indirect cost rates in December 2017 and provided training to staff in January 2018. The training emphasized the need for a standardized process for setting indirect cost rates, including the use of standardized templates and verification of cognizance. In addition, NSF updated the cognizance of each individual awardee in its database, ensured that all applicable dates were entered into the database for the awardees' proposals, checked for overdue proposals, and sent notices to awardees as needed.

|

| National Science Foundation | The Director of NSF should add details to NSF's internal guidance for setting indirect cost rates specifying (1) the criteria to be used by the supervisor for assessing the level of risk and steps for mitigating the risks at each level and (2) the steps for supervisory review of the process for setting indirect cost rates and documentation of the results of the review. (Recommendation 2) |

NSF issued revised guidance for setting indirect cost rates in December 2017. The revised guidance included a new section that identified criteria for complexity designations for indirect cost rate proposals, such as a significant increase in an organization's requested rate. In addition, the guidance included a new checklist that specified steps for supervisory review of the rate-setting process, such as confirming that the analyst assigned to review an indirect cost rate proposal checked it for consistency and confirmed the accuracy of its calculation.

|

| National Science Foundation | The Director of NSF should add procedures to NSF's internal guidance for (1) implementing the applicable new provisions of the Uniform Guidance, including updating links to Office of Management and Budget guidance, and (2) monitoring the indirect cost rates that the Department of Interior sets on NSF's behalf. (Recommendation 3) |

NSF issued revised guidance for setting indirect cost rates in December 2017. The revised guidance included a new section on rate options authorized by the Uniform Guidance, such as extensions of negotiated rates. In addition, the guidance included a revised section that identified actions NSF will take to oversee indirect cost rates set by the Department of Interior, such as reviewing files for selected rates completed by the department to ensure the negotiation process meets appropriate standards.

|