2016 Filing Season: IRS Improved Telephone Service but Needs to Better Assist Identity Theft Victims and Prevent Release of Fraudulent Refunds

Fast Facts

Taxpayers rely on IRS to help them comply with the tax code and file their taxes. We testified that, although IRS improved its telephone service during the 2016 tax filing season, service year-round was not as good.

We also looked at how IRS helps taxpayers who are victims of ID theft refund fraud—wherein fraudsters pose as taxpayers and file returns seeking refunds. IRS has improved service for these victims, but inefficiencies remain.

In our previous report on the subject, we recommended that IRS display its service standards and performance online to let customers know what to expect, and improve service to refund fraud victims.

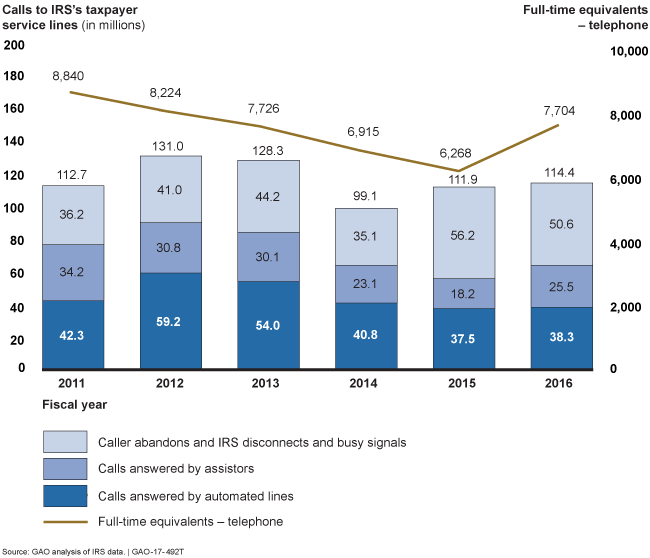

IRS's Ability to Answer Telephone Calls Improved Compared to Last Year, but Remains Lower than Prior Years

Graphic showing number of calls and IRS resources to answer them

Highlights

What GAO Found

The Internal Revenue Service (IRS) provided better telephone service to callers during the 2016 filing season--generally between January and mid-April--compared to 2015. However, its performance during the full fiscal year remained low. IRS does not make this nor other types of customer service information easily available to taxpayers, such as in an online dashboard. Without easily accessible information, taxpayers are not well informed on what to expect when requesting services from IRS.

IRS has improved aspects of service for victims of identity theft (IDT) refund fraud. However, inefficiencies contribute to delays, and potentially weak internal controls may lead to the release of fraudulent refunds. In turn, this limits IRS's ability to serve taxpayers and protect federal dollars. While IRS has reduced its backlog of IDT cases and formed a team to improve its handling of these cases, GAO has identified areas for potential improvement. Specifically:

- File retrieval and scanning processes contributed to delays and unnecessary requests for documents. For example, in 2 of 16 cases, resolution was delayed by at least 1 month while an assistor waited for another unit to retrieve and scan documents into IRS's system. In one of those cases, plus one other, the document request was unnecessary because the assistor closed the case without the document. Inefficient processes and unnecessary requests to retrieve and scan documents can delay case resolution and refunds to the legitimate taxpayer.

- Potential weaknesses in IRS's internal control processes could lead to IRS paying refunds to fraudsters. In discussion groups with GAO, IRS assistors and managers said some assistors may release refunds even if indicators on the account show that the tax return is under review for IDT, or two returns have been filed for that taxpayer. Some participants said assistors answering telephone calls can release these holds because they do not understand the codes on the taxpayer's account. IRS officials said that these errors are not widespread and provided data to support their position. However, GAO identified weaknesses in those data, which IRS officials acknowledged. In response to this report, in January 2017 officials provided another analysis of IRS data that they said showed this type of error does occur but may not be as widespread as staff and managers suggested. GAO will continue to work with IRS to determine if these additional data are sufficient to address its recommendation.

- IRS does not notify taxpayers when a dependent's identity appears on a fraudulent return. According to IRS officials, the agency does not consider a dependent to be a victim if his or her Social Security number had been used as a dependent on a fraudulent return. However, IRS has previously provided guidance to taxpayers when a dependent was a victim of identity theft. After one data breach in 2015, IRS notified taxpayers and provided information on actions that parents could take to protect a minor's identity when their dependents were also victims. By not notifying taxpayers that their dependents' information may have been used to commit fraud, IRS is limiting taxpayers' ability to take action to protect their dependents' identity.

Why GAO Did This Study

This testimony summarizes the information contained in GAO's January 2017 report, entitled 2016 Filing Season: IRS Improved Telephone Service but Needs to Better Assist Identity Theft Victims and Prevent Release of Fraudulent Refunds (GAO-17-186).

For more information, contact Jessica Lucas-Judy at (202) 512-9110 or lucasjudyj@gao.gov.