Student Loans: Oversight of Servicemembers' Interest Rate Cap Could Be Strengthened

Highlights

What GAO Found

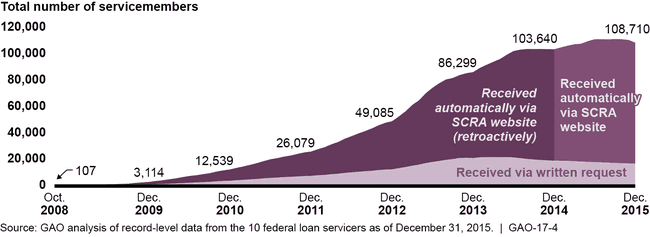

The Servicemembers Civil Relief Act (SCRA) provides servicemembers with an interest rate cap of 6 percent on student loans while they are on active duty. The number of servicemembers with federal student loans who received this rate cap increased as a result of the Department of Education (Education) requiring federal loan servicers to regularly use the Department of Defense's (DOD) SCRA website to identify eligible servicemembers and automatically apply the rate cap without requiring servicemembers to provide written notice of active duty (see figure). Using the automated process, some federal loan servicers identified borrowers who had been eligible for the rate cap as far back as 2008, when the SCRA rate cap first applied to federal loans, and retroactively applied the cap.

Number of Servicemembers with Federal Student Loans Who Received the Servicemembers Civil Relief Act (SCRA) Interest Rate Cap, October 2008 to December 2015

Note: In December 2014 the Department of Education issued the final in a series of updates to its contracts with the 10 federal student loan servicers directing them to use the SCRA website on a monthly basis.

Servicemembers can face challenges obtaining the SCRA rate cap due to their failure to receive accurate information. Federal internal control standards state that agencies should externally communicate the information necessary to achieve their objectives. However, some servicemembers eligible for the cap may not receive it because information used by DOD to inform them about the cap is inaccurate: for example, some DOD information states that the rate cap does not apply to student loans. In addition, because the automated process to identify eligible servicemembers is not required for private student loans, servicemembers with private loans may be particularly at risk of not receiving the accurate information needed to obtain the cap themselves.

While Education monitors the application of the SCRA cap for federally owned or guaranteed student loans, there is a gap in oversight for private student loans. The Consumer Financial Protection Bureau (CFPB), four federal financial regulators of banks, and the Department of Justice (DOJ) each oversees aspects of private student loans or SCRA, but none has the authority to routinely oversee SCRA compliance at nonbank entities that handle private student loans. These nonbank entities include institutions of higher education and private companies. The resulting gap in oversight of SCRA compliance for these nonbank entities that make or service private student loans increases the risk that servicemembers will not receive a benefit for which they are eligible.

Why GAO Did This Study

SCRA helps servicemembers financially by capping interest rates on student loans during active duty. As of May 2016, about 1.3 million servicemembers were on active duty. The number of active duty servicemembers with student loans is unknown, as is the number eligible for the rate cap who may not have received it. GAO was asked to review implementation of the rate cap for servicemembers' student loans.

This report examines: (1) the number of servicemembers who received the cap for student loans (2) challenges that servicemembers face in doing so, and (3) the extent to which federal agencies oversee implementation of the cap. GAO analyzed data from 2008 through 2015 from the 10 federal student loan servicers; reviewed relevant federal laws, regulations, policies, and training materials; and interviewed representatives of the servicers and servicemember advocacy groups, and officials from DOD, Education, the CFPB and DOJ.

Recommendations

GAO is making four recommendations, including that DOD improve the accuracy of SCRA information on student loans, and that CFPB and DOJ collaborate to ensure routine oversight of nonbank lenders and servicers, and seek additional authority, if needed. DOD disagreed and said it already provides accurate information. DOJ agreed and CFPB did not specifically agree, but said that all eligible servicemembers should receive the cap. GAO maintains that DOD's outreach materials are not always accurate and that routine oversight is necessary for nonbank lenders and servicers.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Department of Defense | To help ensure quality information is conveyed to servicemembers about how the Servicemembers Civil Relief Act (SCRA) interest rate cap applies to student loans, the Secretary of Defense should direct the secretaries of each service branch, and work with other secretaries as appropriate, to ensure that all information about the SCRA interest rate cap for student loans is accurate when provided to servicemembers and to those who work with servicemembers to help them obtain SCRA benefits, including information contained in outreach materials. |

The Department of Defense (DOD) disagreed with this recommendation believing it to be unnecessary because it is already providing accurate information. Specifically, DOD noted that the information provided in several documents GAO reviewed is accurately based on statute whereas Education's updated requirement to automatically apply the cap is based on policy that could change in the future. Moreover, the automated process applies only to federal and commercial FFEL student loans in contrast to other types of debt. DOD said that providing information based on statute rather than policy would cause less confusion and was a better approach than what we recommend. However, our report noted that Education formalized the automated process through federal regulations, effective July 2016, which legally require servicers to use this process for all federal and commercial FFEL loans. In addition, DOD said it was unable to verify whether DOD's Military OneSource website inaccurately states that the SCRA rate cap does not apply to commercial FFEL loans. However, our searches of the website still turned up this inaccuracy. DOD said it would look into a means of verifying website information but that in the meantime, it is satisfied that its training provides correct information. Given that Military OneSource is a key source of information for servicemembers and that some documents DOD provided state that the SCRA rate cap does not apply to student loans, we continue to believe that servicemembers are not always receiving accurate and up-to-date information. As of April 2026, DOD continues to disagree with this recommendation based on the rationale above.

|

| Office of the Attorney General | To ensure that all eligible servicemembers with student loans receive the SCRA interest rate cap, the Attorney General should direct the Department of Justice to consider modifying its proposed changes to SCRA to require use of the automatic eligibility check for private student loans. |

The Department of Justice (DOJ) stated that its current package of proposed legislative changes provides benefits to servicemembers with all kinds of loans, including private student loans. Rather than requiring servicemembers to submit written notice and a copy of military orders, they need only give their creditors oral or written notice of eligibility for the cap. Creditors would then have to search Department of Defense records to verify servicemembers' military service and apply the SCRA interest rate cap, when applicable. DOJ believes these changes would significantly benefit all servicemembers with loans while providing a uniform standard for all types of creditors. However, as stated in our report, servicemembers with private student loans would still need to be aware of the rate cap to give notice, whether written or oral. As such, an automatic eligibility check would ensure that servicemembers with private student loans receive a benefit for which they are eligible. In 2021, DOJ stated it cannot require private lenders to perform automatic eligibility checks and that it will not modify its proposed legislative changes to require such checks. Accordingly, DOJ plans no further action toward implementing this recommendation.

|

| Department of Education | To enhance customer service, the Secretary of Education should direct the Office of Federal Student Aid to identify ways to modify the data collected in its unified borrower complaint system to allow the agency to more precisely identify and analyze complaints specifically about the SCRA interest rate cap. |

The Department of Education said it is committed to monitoring the Servicemembers Civil Relief Act (SCRA)-related complaints it receives through its Federal Student Aid Feedback System. Toward that end, it has created a complaint subcategory for SCRA under the "Military and Veterans Benefit" category, which will allow Education to track, analyze, and report any feedback regarding SCRA. In addition, it will continue to run key word searches to identify other complaints that may have been miscategorized by the complainant that pertain to SCRA's requirements, and ensure they are considered appropriately. Further, the results of the key word search will be captured in Education's annual report.

|

| Consumer Financial Protection Bureau | To better ensure that servicemembers with private student loans benefit from the SCRA interest rate cap, the Director of the Consumer Financial Protection Bureau and the Attorney General of the Department of Justice should coordinate with each other, and with the four federal financial regulators, as appropriate, to determine the best way to ensure routine oversight of SCRA compliance for all nonbank private student loan lenders and servicers. If CFPB and DOJ determine that additional statutory authority is needed to facilitate such oversight, CFPB and DOJ should develop a legislative proposal for Congress. |

The Consumer Financial Protection Bureau (CFPB) stated that it is committed to working with the Department of Justice (DOJ) and federal financial regulators, when possible, to facilitate oversight of SCRA compliance and that it will support all relevant federal agencies in using their respective authorities to identify and address SCRA violations as efficiently and effectively as possible. While CFPB coordinates with DOJ and other federal regulators in general, there is no single agency authorized to enforce SCRA compliance. As a result, there is still no entity conducting routine supervisory reviews of nonbank private student loan lenders and servicers. In addition, CFPB may refer complaints from servicemembers about the SCRA rate cap for private student loans to DOJ and other financial regulators. However, we believe this does not constitute routine, proactive oversight and also presumes servicemembers are aware of the SCRA rate cap. In June 2021, CFPB stated that it plans no further action toward implementing our recommendation. The agency's efforts are insufficient to address this recommendation and, without further action, the agency may not be able to ensure that servicemembers with private student loans benefit from the SCRA interest rate cap.

|

| Office of the Attorney General | To better ensure that servicemembers with private student loans benefit from the SCRA interest rate cap, the Director of the Consumer Financial Protection Bureau and the Attorney General of the Department of Justice should coordinate with each other, and with the four federal financial regulators, as appropriate, to determine the best way to ensure routine oversight of SCRA compliance for all nonbank private student loan lenders and servicers. If CFPB and DOJ determine that additional statutory authority is needed to facilitate such oversight, CFPB and DOJ should develop a legislative proposal for Congress. |

The Department of Justice (DOJ) believes that it is in full compliance with this recommendation and that the four federal financial regulators do not have statutory authority to examine nonbank private student loan lenders and servicers unaffiliated with a depository institution. With regard to SCRA compliance, DOJ stated that it already coordinates extensively with the Consumer Financial Protection Bureau (CFPB) and the financial regulators through such mechanisms as referrals from CFPB for any SCRA-related violations and access to its consumer complaint database, and regular meetings with CFPB, and that it will continue to build upon these efforts. GAO believes that these mechanisms, while commendable, do not constitute exercising routine oversight of nonbank private student loan lenders and servicers who are not affiliated with a depository institution. We believe that additional interagency coordination, including working with CFPB to seek additional statutory authority, as needed, is necessary to ensure routine SCRA compliance. In 2021, DOJ stated that it lacks statutory authority over private, nonbank lenders and servicers and that it will not seek additional authority. Accordingly, DOJ plans no further action toward implementing this recommendation.

|