National Nuclear Security Administration: A Plan Incorporating Leading Practices Is Needed to Guide Cost Reporting Improvement Effort

Fast Facts

The National Nuclear Security Administration has experienced a number of issues with contract management and oversight over the past several years, and submitted a plan to Congress in 2016 outlining its strategy to improve its financial management.

However, we found that this plan did not incorporate leading strategic planning practices, and that it lacked the necessary details to be a meaningful tool to improve financial oversight at the agency.

We recommended that NNSA develop a plan that fully incorporates leading strategic practices, such as defining strategies and identifying resources needed to achieve goals.

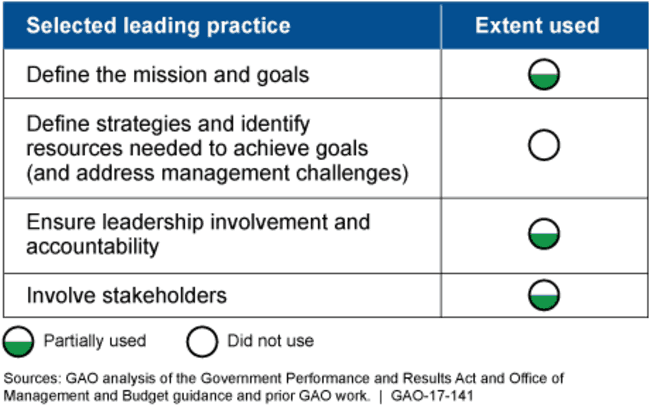

Selected Leading Practices in Federal Strategic Planning, Their Characteristics, and the Extent to Which NNSA Used Them in Developing Its Plan

Table showing 4 practices, 1 of which was not used, 3 of which were partially used.

Highlights

What GAO Found

On February 5, 2016, more than 13 months after the statutory reporting deadline, the National Nuclear Security Administration (NNSA) submitted to Congress a plan for improving and integrating its financial management. The plan includes the four elements required by the National Defense Authorization Act for Fiscal Year 2014—a feasibility assessment, estimated costs, expected results, and an implementation timeline—but contains few details related to each of these elements. For example, NNSA's feasibility assessment includes a list of implementation concerns—including general concerns related to the availability of resources and to identifying and implementing an information technology solution—but does not provide any specific information regarding these concerns. In addition, NNSA's plan includes a cost estimate of between $10 million and $70 million but provides no details on how the estimate was developed beyond stating that it is based on professional judgment and input from NNSA's contractors. The plan also includes a “notional” implementation timeline that calls for the plan's core elements to be completed in 3 to 5 years but does not include details on which elements are considered core elements.

NNSA's financial integration plan does not fully incorporate leading strategic planning practices, which limits its usefulness as a planning tool as well as the effectiveness of NNSA's effort to provide meaningful financial information to Congress and other stakeholders. As GAO has reported previously, in developing plans for implementing new initiatives, agencies can benefit from following leading practices for strategic planning. These leading practices include (1) defining the missions and goals of a program or initiative, (2) defining strategies and identifying resources needed to achieve goals, (3) ensuring leadership involvement, and (4) involving stakeholders in planning. However, NNSA's plan does not fully incorporate any of these leading practices. For example, beyond the high-level cost estimate provided, NNSA's plan does not include a description of the specific resources needed to meet specific elements of the plan or define strategies that address management challenges, including the implementation concerns identified in the plan's feasibility assessment. In addition, NNSA did not involve key stakeholders in developing its plan. Because NNSA's plan does not incorporate leading strategic planning practices, it has not provided a useful road map for guiding NNSA's effort. NNSA officials told GAO that the plan they submitted to Congress was never intended to provide a road map to guide their efforts. Instead, they said the purpose of the plan was to identify general principles and a strategic vision for achieving financial integration. The NNSA official responsible for overseeing the plan's execution told GAO, he has begun to develop a more comprehensive and actionable plan to guide NNSA's effort. However, it is unclear when the new plan will be finalized or the extent to which it will incorporate leading practices. Until a plan is in place that incorporates leading strategic planning practices, NNSA cannot be assured that its efforts will result in a cost collection tool that produces reliable enterprise-wide information that satisfies the needs of Congress and program managers. Such information would better position NNSA to address long-standing contract and project management challenges. Without proper planning, NNSA could waste valuable resources, time, and effort on its financial integration effort.

Why GAO Did This Study

Effective management and oversight of contracts, projects, and programs are dependent upon the availability of reliable enterprise-wide financial management information. Such information is also needed by Congress to carry out its oversight responsibilities and make budgetary decisions. However, meaningful cost analysis of NNSA programs, including comparisons across programs, contractors, and sites, is not possible because NNSA's contractors use different methods of accounting for and tracking costs.

The National Defense Authorization Act for Fiscal Year 2014 required NNSA to develop and submit to Congress a plan to improve and integrate its financial management. An explanatory statement accompanying the act included a provision for GAO to review the adequacy of NNSA's plan. This report evaluates the extent to which NNSA's plan (1) addresses the objectives of the act and (2) follows leading practices for planning. GAO reviewed NNSA's plan and compared it with legislative requirements and leading practices for planning and interviewed NNSA officials.

Recommendations

To provide a road map to guide NNSA's financial management improvement effort, GAO recommends that the NNSA Administrator direct the Program Director of Financial Integration to develop a plan for producing cost information that fully incorporates leading planning practices. NNSA agreed to update its plan and address the items GAO identified.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| National Nuclear Security Administration |

Priority Rec.

To help provide a roadmap to effectively guide NNSA's effort to integrate and improve its financial management, the NNSA Administrator should direct the Program Director of Financial Integration to develop a plan for producing cost information that fully incorporates leading practices. |

NNSA agreed with the recommendation. In its written responses to our report, NNSA stated that it would address the items we identified in its annual update to Congress on its financial integration initiative. NNSA issued its annual 2017 update, but the report did not fully incorporate leading strategic planning practices. For example, its 2017 report included a "next steps" section under each goal that provided some information on the strategy needed and an estimate of costs, but those sections contained limited details. NNSA planned to incorporate additional leading practices as implementation of its financial integration effort evolved. As of November 2018, we decided to close this recommendation as not implemented because NNSA has moved into the implementation phase for its financial integration efforts and it is not planning to perform additional planning that would incorporate leading practices. The Senate report accompanying the National Defense Authorization Act for Fiscal Year 2018 includes a provision for us to review NNSA's implementation of financial integration. We will continue to monitor NNSA's implementation of financial integration as part of that effort.

|