Internal Revenue Service: Preliminary Observations on the Fiscal Year 2017 Budget Request and 2016 Filing Season Performance

Highlights

What GAO Found

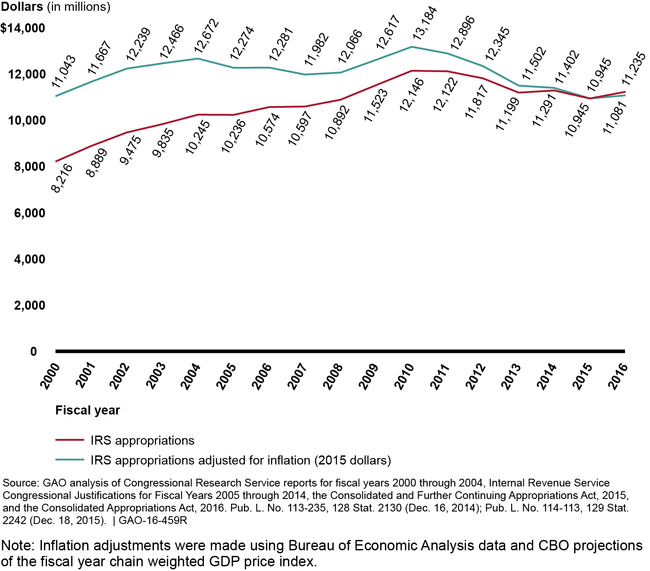

The Internal Revenue Service’s (IRS) fiscal year 2016 appropriation increased by $290 million to $11.2 billion over fiscal year 2015 but is about $900 million (7 percent) lower than fiscal year 2011. IRS allocated the funds across 3 appropriation accounts: Taxpayer Services ($176.8 million), Operations Support ($108.2 million), and Enforcement ($4.9 million). For fiscal year 2017, the President requested $12.3 billion in appropriations, about a $1 billion increase (9 percent) over fiscal year 2016 enacted levels. This includes $515 million in a program integrity cap adjustment. Excluding the spending cap adjustment, which would require separate legislation, the request is $11.8 billion, a 5 percent increase. IRS may also allocate other budgetary resources, such as user fee revenue. In fiscal year 2015, transfers of user fees ($454 million) accounted for 3.8 percent of total available resources ($11,976 million). Full-time equivalents funded with annual appropriations declined by 12,000 (13 percent) between fiscal years 2011 and 2016. After years of taking short-term actions such as limiting hiring and curtailing overtime, IRS is taking steps to strategically manage its resources by identifying priorities in formulating its 2017 budget request. Further, GAO has open recommendations to IRS—including 10 priority recommendations—that would help IRS better manage operations and improve taxpayer service. Implementing these recommendations is a key step in reducing the $385 billion net tax gap, as well as in strengthening tax administration and service to taxpayers.

Processing of individual income tax returns in 2016 has gone relatively smoothly through mid-February and IRS anticipates improved taxpayer service due, in part, to additional funding. Specifically, IRS projects that the percentage of callers seeking live assistance who receive it (level of service) will increase from a low of about 38 percent for fiscal year 2015 to 47 percent for fiscal year 2016—including 65 percent for the filing season. IRS also projects average telephone wait time will improve from about 31 minutes for fiscal year 2015 to about 26 minutes for fiscal year 2016. However, this will still be about twice as long as the wait time for fiscal year 2011. Nevertheless, IRS has provided improved telephone service through mid-February compared to the same time last year—level of service was 76 percent (a 33 percentage point increase) while the average wait time dropped to 9 minutes (an improvement of about 70 percent). Importantly, improved customer service, including for telephones, can help increase voluntary tax compliance. IRS took steps in 2016—including detailing staff from enforcement to customer service and providing overtime—to help improve service. Finally, IRS is leveraging industry partners to combat identity theft refund fraud and improve cybersecurity efforts to protect taxpayer information.

Figure 1: IRS Appropriations Nominal and Inflation Adjusted (2015 Dollars, in Millions), from Fiscal Years 2000 to 2016

Why GAO Did This Study

GAO has reported that, in recent years, IRS has absorbed significant budget cuts and struggled to provide quality service. During the filing season, IRS processes millions of tax returns, issues refunds, and provides telephone and other services to millions of taxpayers.

GAO was asked to provide preliminary information on the President’s fiscal year 2017 budget request for IRS and on IRS’s 2016 filing season performance. GAO’s objectives were to describe trends in IRS’s (1) budget and operations from fiscal year 2011 through the fiscal year 2017 request, including IRS efforts to strategically manage its budget, and (2) performance in providing taxpayer service during the 2016 filing season to date compared to prior years and interim performance of IRS’s processing of individual income tax returns.

To address these objectives, GAO reviewed the President's budget request and IRS's congressional justifications for fiscal years 2011 through 2017 as well as IRS planning documents. This time frame was selected to provide 5 years of full-year data in addition to current year and requested levels. In addition, GAO reviewed IRS filing season performance data between 2011 and 2016 through mid-February. GAO also interviewed IRS budget and operations officials as well as industry partners.

Recommendations

GAO is not making new recommendations at this time but has previously recommended actions IRS could take to improve operations and plan more strategically. GAO highlighted 10 open recommendations as being the highest priority for implementation. IRS reported to GAO that it has identified points of contact for each recommendation and is working internally to respond.