2016 Annual Report: Additional Opportunities to Reduce Fragmentation, Overlap, and Duplication and Achieve Other Financial Benefits

GAO-16-375SP

Published: Apr 13, 2016. Publicly Released: Apr 13, 2016.

Skip to Highlights

Highlights

Improving Efficiency and Effectiveness

GAO's 2016 Annual Report identified 12 new areas of fragmentation, overlap, and duplication in federal programs and activities. GAO also identified 59 new opportunities for cost savings and revenue enhancement. Related work and GAO's Action Tracker—a tool that tracks progress on GAO's specific suggestions for improvement—are available here.

What GAO Found

In its 2016 report, GAO presents 92 actions that the executive branch or Congress could take to improve efficiency and effectiveness across 37 areas that span a broad range of government missions and functions.

- GAO suggests 33 actions to address evidence of fragmentation, overlap, or duplication in 12 new areas across the government missions of defense, economic development, health, homeland security, and information technology.

- GAO also presents 59 opportunities for executive branch agencies or Congress to take actions to reduce the cost of government operations or enhance revenue collections for the Treasury across 25 areas of government.

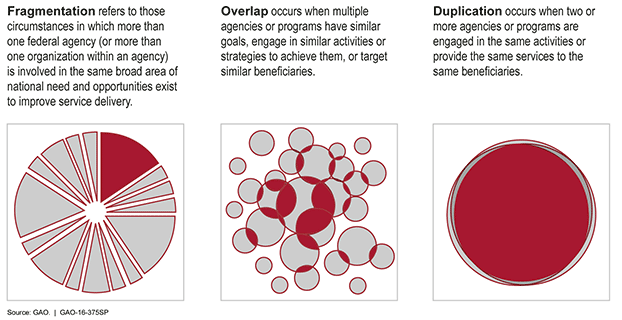

Defining Fragmentation, Overlap, and Duplication

.fancybox-wrap{width:760px !important;}

.fancybox-inner{width:740px !important;}

.fancybox-skin{padding-left:0;}

html,body{overflow-x:hidden !important;}

Full Report

GAO Contacts

Orice Williams Brown

Managing Director, Office of Congressional Relations

Congressional Relations

Public Inquiries

Topics

Budget obligationsDefense cost controlDefense procurementEconomic developmentExecutive agenciesFederal procurementFinancial analysisFunds managementFuture budget projectionsHealth care programsInternal controlsMedicaidMedicareOverpaymentsProperty disposalRedundancySurplus federal propertyDuplication of effortFiscal imbalanceProgram goals or objectivesSavings estimates