Federal Student Loans: Education Could Do More to Help Ensure Borrowers Are Aware of Repayment and Forgiveness Options

Highlights

What GAO Found

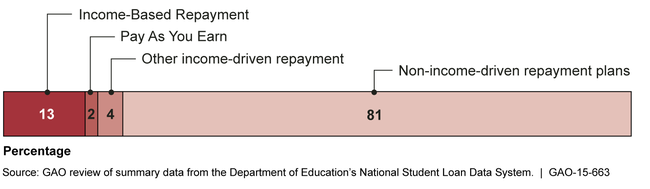

Many eligible borrowers do not participate in the Department of Education's (Education) Income-Based Repayment and Pay As You Earn repayment plans for Direct Loans, and Education has not provided information about the plans to all borrowers in repayment. These plans provide eligible borrowers with lower payments based on income and set timelines for forgiveness of any remaining loan balances. While the Department of the Treasury estimated that 51 percent of Direct Loan borrowers were eligible for Income-Based Repayment as of September 2012, the most recent available estimate, Education data show 13 percent were participating as of September 2014. An additional 2 percent were in Pay As You Earn. Moreover, Education has reported ongoing concerns regarding borrowers' awareness of these plans. Although Education has a strategic goal to provide superior information and service to borrowers, the agency has not consistently notified borrowers who have entered repayment about the plans. As a result, borrowers who could benefit from the plans may miss the chance to lower their payments and reduce the risk of defaulting on their loans.

Repayment Plan Participation of Direct Loan Borrowers in Active Repayment, September 2014

Few borrowers who may be employed in public service have had their employment and loans certified for the Public Service Loan Forgiveness program, and Education has not assessed its efforts to increase borrower awareness. Beginning in 2017, the program is to forgive remaining Direct Loan balances of eligible borrowers employed in public service for at least 10 years. As of September 2014, Education's loan servicer for the program had certified employment and loans for fewer than 150,000 borrowers; however, borrowers may wait until 2017 to request certification. While the number of borrowers eligible for the program is unknown, if borrowers are employed in public service at a rate comparable to the U.S. workforce, about 4 million may be employed in public service. It is unclear whether borrowers who may be eligible for the program are aware of it. Although Education has a strategic goal to provide superior information and service to borrowers and provides information about Public Service Loan Forgiveness through its website and other means, it has not notified all borrowers in repayment about the program. In addition, Education has not examined borrower awareness of the program to determine how well its efforts are working. Borrowers who have not been notified about Public Service Loan Forgiveness may not benefit from the program when it becomes available in 2017, potentially forgoing thousands of dollars in loan forgiveness.

Why GAO Did This Study

As of September 2014, outstanding federal student loan debt exceeded $1 trillion, and about 14 percent of borrowers had defaulted on their loans within 3 years of entering repayment, according to Education data. GAO was asked to review options intended to help borrowers repay their loans.

For Direct Loan borrowers GAO examined: (1) how participation in Income-Based Repayment and Pay As You Earn compares to eligibility, and to what extent Education has taken steps to increase awareness of these plans, and (2) what is known about Public Service Loan Forgiveness certification and eligibility, and to what extent Education has taken steps to increase awareness of this program. GAO reviewed relevant federal laws, regulations, and guidance; September 2014 data from Education and its loan servicer for Public Service Loan Forgiveness; Treasury's eligibility estimates; and 2012 employment data (most recent available) from the Bureau of Labor Statistics. GAO also interviewed officials from three loan servicers that service about half of Education's loan recipients.

Recommendations

GAO recommends Education consistently notify borrowers in repayment about income-driven repayment, and examine borrower awareness of Public Service Loan Forgiveness. Education generally agreed with GAO's recommendations, but it believed the report overstated the extent to which borrowers lack awareness of income-driven repayment. GAO modified the report to clarify this issue.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Department of Education | To help ensure that Income-Based Repayment, Pay As You Earn, and Public Service Loan Forgiveness serve their intended beneficiaries to the greatest extent possible, the Secretary of Education should take steps to consistently and regularly notify all borrowers who have entered repayment of income-driven repayment plan options, including Income-Based Repayment and Pay As You Earn. |

The Department of Education generally concurred with our recommendation, stating that it is committed to ensuring that federal student loan borrowers have the information they need to manage their debt, including details regarding income-driven repayment plans and loan forgiveness programs. Beginning in 2015, Education directed its loan servicers to start sending detailed income-driven repayment information, such as projected monthly payment amounts and total amounts paid over the life of the loan under each plan, on a quarterly basis to all borrowers who are in school or in the 6-month grace period after leaving school. Education reported that in 2016 its loan servicers also began sending an email to borrowers in the fifth month of their grace period with information about applying for income-driven repayment plans and Public Service Loan Forgiveness. From 2016 through 2019, Education also sent emails about income-driven repayment plans and Public Service Loan Forgiveness to certain groups of borrowers, including those who expressed interest in income-driven repayment plans during exit counseling, had Federal Family Education Loans, were in the Standard repayment plan and were 31 to 270 days delinquent, or were in a discretionary forbearance. In response to the COVID-19 global pandemic, Education began communicating with borrowers about student aid relief provided under the CARES Act and executive actions that, starting March 13, 2020, suspended student loan payments and interest accrual for Direct and Federal Family Education loans held by Education through at least September 30, 2021. In July 2020, as part of this effort, Education began sending monthly emails to all borrowers that outlined available repayment options, including income-driven repayment plans, when the payment suspension is over. According to Education, these emails have been sent to about 26 million borrowers and will continue through the payment suspension. We believe these emails demonstrate consistent and regular notification of all borrowers who have entered repayment about income-driven repayment options.

|

| Department of Education | To help ensure that Income-Based Repayment, Pay As You Earn, and Public Service Loan Forgiveness serve their intended beneficiaries to the greatest extent possible, the Secretary of Education should take steps to examine borrower awareness of Public Service Loan Forgiveness and increase outreach about the program as needed. |

The Department of Education (Education) generally concurred with our recommendation. Since September 2015, Education has examined borrower awareness of Public Service Loan Forgiveness through its monthly customer feedback process, and measured borrower awareness of repayment options through ongoing customer satisfaction surveys. Based on this feedback, Education's Office of Federal Student Aid has used a variety of approaches to increase outreach about the program. 1) In December 2015, Education added a question to the income-driven repayment plan application that asked borrowers whether they work for a government or not-for-profit organization. Borrowers who answer "yes" receive an email with additional information about the program. 2) As of June 2016, Education began sending emails about Public Service Loan Forgiveness to all borrowers in the 6-month grace period that typically occurs before they enter repayment. 3) From June through September 2016, the agency sent emails to 3.3 million borrowers who participated in income-driven repayment and had not indicated their interest in Public Service Loan Forgiveness. 4) In 2016, Education conducted webinars for borrowers and for financial aid educators about Public Service Loan Forgiveness. 5) Education continued to provide information about Public Service Loan Forgiveness through social media, loan servicers, repayment calculators, publications, and other approaches.

|